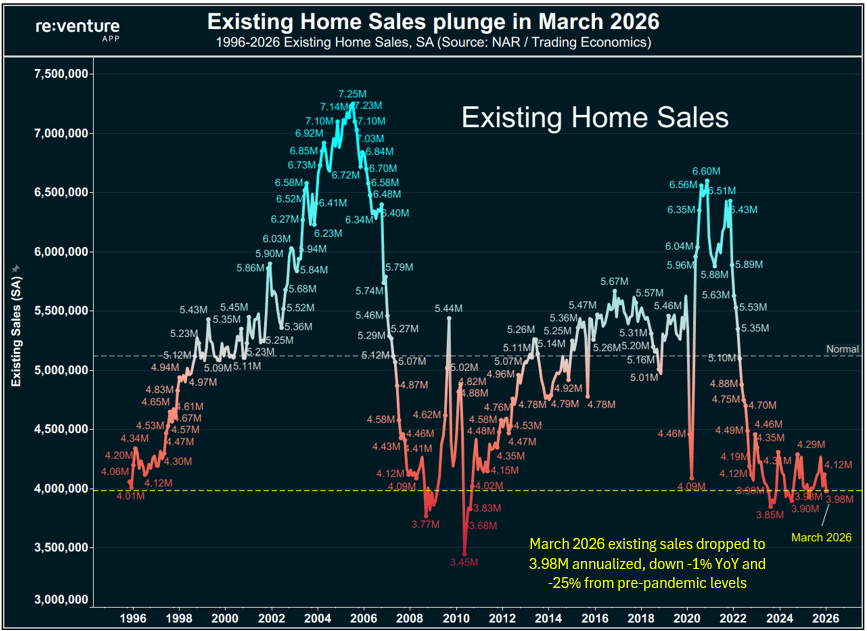

@Please_NoLabels @DaveHcontrarian @glendenningj @KK19334850 @KevinKummerow @coding_thoughts Different kind of seller though. 2008 sellers were forced out by bad loans. Today's sellers are owners choosing not to sell because moving means doubling their mortgage payment. Are those really comparable? One is distress. One is rational calculation.

English