M J JELIL

737 posts

M J JELIL

@m_jelil

I am Muslim

Daarul Ijra crescent Alasaa Co Katılım Kasım 2020

1.2K Takip Edilen216 Takipçiler

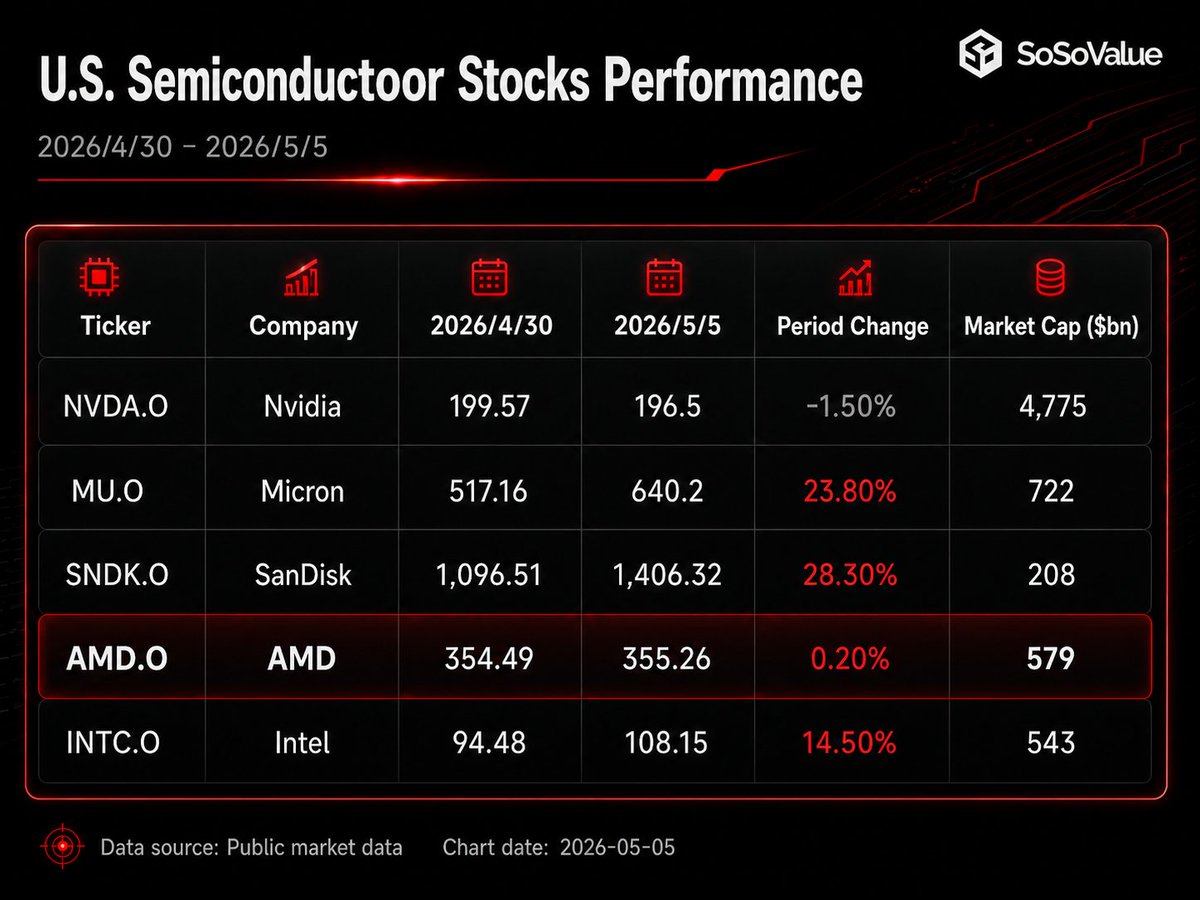

🚨SoSoValue Flash: Hormuz Skirmishes Ignite Noise, AI Shifts into "Seesaw" Mode

💥 Core Catalyst: Truce Extensions & Tehran ShadowsA direct military flare-up occurred as Iran accused the U.S. of striking a tanker, triggering IRGC retaliation against warships followed by U.S. counterstrikes. However, Trump maintains that the ceasefire holds, and Washington’s "self-defense" framing signals a lack of appetite for full-scale escalation, containing the macro fallout.

🔍 Key Logic Shifts:

1️⃣ Geopolitics: Local skirmishes pushed Brent back above $100, injecting fresh anxiety into the 14-point deal narrative. Yet, as long as both sides signal restraint, the damage to global risk appetite remains localized rather than systemic.

2️⃣ Macro Policy: Japan is suspected of a third FX intervention raid near ¥4.68T. Repeated yen-defense measures are steepening the odds for a June BOJ rate hike, adding pressure to global carry trade dynamics.

3️⃣ AI & Earnings: AI remains the undisputed engine, but internal rotations have begun. After an explosive rally, Memory and CPU players are seeing profit-taking, while NVIDIA and software laggards are catching a bid. Consolidation looms as the market gauges the "post-earnings" narrative.

📊 Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI Hardware: $SNDK | $MU | $AMD | $INTC

English

M J JELIL retweetledi

🚨AMD's Second Act: From GPU Challenger to AI Infrastructure Duopoly

AMD reported Q1 2026 results with revenue of $10.25B (+38% YoY), ahead of the $9.84B consensus; Non-GAAP EPS of $1.37 (+43% YoY), also beating expectations. GAAP net income came in at $1.38B (+95% YoY); Non-GAAP net income reached $2.27B (+45% YoY), with Non-GAAP gross margin at 55%. Free cash flow hit a record $2.6B for the quarter, more than tripling year-over-year.

On the surface, the financials were a modest beat across the board — but AMD stock surged more than 18% in after-hours trading, briefly topping $410. The numbers alone don't explain the move. What does: CEO Lisa Su's forward guidance. Su stated that the server CPU TAM will double to $120B by 2030, that annual data center AI revenue is on track to reach "tens of billions of dollars," and reaffirmed a long-term Non-GAAP EPS target of over $20.

⚡️Core Theme: Data Center Takes the Wheel

Data Center revenue reached $5.78B, up 57% YoY, crossing the halfway mark of total company revenue and becoming the primary driver of both top-line and earnings growth — powered by the dual engine of EPYC server CPUs and Instinct GPUs.

The market's historical read on AMD's AI thesis was straightforward: can MI300/MI350/MI450 take share from NVIDIA? What this quarter's management commentary reframes is that agentic AI and inference workloads are driving a significant uplift in CPU demand as well. AI clusters don't just need GPUs for training and inference — they require substantial CPU capacity for orchestration, data preprocessing, head node management, and parallel task scheduling. AMD's advantage is now expanding from a single-point GPU play into a compound architecture: EPYC + Instinct + Helios, together.

Critically, CEO Lisa Su raised AMD's server CPU TAM outlook significantly: the addressable market is now expected to grow at over 35% annually, reaching more than $120B by 2030 — effectively doubling the prior forecast of ~18% CAGR and a ~$60B TAM.

🌞Product Pipeline: MI450 / Helios Enter the Visible Order Cycle

On the AI accelerator front, AMD confirmed that MI450 series GPUs have begun sampling with lead customers, and Helios rack-scale AI systems remain on track for production shipments in H2 2026. Su noted that customer demand forecasts for MI450 and Helios have already exceeded AMD's original 2027 plans, with new customers now in discussions for large-scale deployments — including additional multi-gigawatt opportunities.

More significantly, AMD raised its confidence in 2027 data center AI revenue: management expressed conviction in achieving tens of billions of dollars in annual data center AI revenue in 2027, ahead of the prior long-term target of greater than 80% CAGR.

On the hyperscaler side, the order book is becoming concrete: OpenAI and Meta have each committed to deploying 6GW of Instinct compute; Oracle plans to launch the world's first publicly available AI supercluster powered by 50,000 MI450 GPUs in Q3. Taken together, these three commitments are moving AMD's status as "AI compute's second source" from narrative to reality.

Q2 Outlook: Above Expectations, Data Center Continues to Accelerate

AMD guided Q2 revenue to approximately $11.2B (±$300M), meaningfully above the $10.5B consensus, representing roughly 46% growth YoY and 9% sequentially. Non-GAAP gross margin is guided at approximately 56%. Server CPU is expected to grow more than 70% for the full year, with both data center AI and server businesses projected to deliver double-digit sequential growth.

📈Bottom Line

This quarter isn't just another beat. The on-track delivery of MI450 and Helios has moved AMD from "potential NVIDIA alternative" to "confirmed co-anchor of AI infrastructure."

The after-hours surge to above $410 implies roughly 30x that $20 long-term EPS target — the market is pricing it in today. Notably, AMD had gone virtually nowhere over the prior three sessions, with tonight's after-hours move catching it up to Intel's recent gains. The capital rotation story isn't complicated: last Friday, Western Digital's blowout earnings ignited a fresh AI hardware rally, with funds rotating out of NVIDIA into memory and CPU names — Western Digital and Micron gained 28% and 24% respectively over three sessions, Intel added 15%, and AMD's earnings tonight became the final piece of that rotation trade.

Looking further out, the key variables are whether MI450 and Helios ship on schedule, whether the Meta and OpenAI deployments convert into durable multi-year order flow, and whether EPYC can continue capturing share as AI-driven CPU demand structurally expands.

English

SoSoValue@SoSoValueCrypto

BTC holds the line. Everything else fades. ✅Five straight weeks of BTC ETF inflows — $153.87M last week. Consistent institutional buying in the $75K–$80K range is starting to look less like opportunistic dip-buying and more like deliberate position-building. BTC has since broken above $80K. ❌ETH tells the opposite story. After three weeks of inflows, last week saw $82.47M exit. ETH holding above $2,300. Short-term profit-taking is the obvious read — but ETH's persistent underperformance relative to BTC is becoming a pattern, not a blip. ⚠️XRP and SOL are effectively invisible right now. XRP ETF net outflows: $35.21K — essentially zero. SOL: seven of eight ETFs recorded no flows whatsoever, with only GSOL moving. SOL at $85.47. Altcoin ETF momentum has quietly evaporated. 💡Institutions are buying BTC at $78K while pulling back from ETH and ignoring the rest. Is this the early setup for a BTC-led move — or just consolidation before the altcoins catch up? Drop your take 👇 #Bitcoin #Ethereum #XRP #Solana #CryptoETF #BTC #ETH #BitcoinETF #SoSoValue

QME

Hey. I am sending you 23,000 ATOS worth about 23 USDT. Come claim it!

ATOS is a mobile mining cryptocurrency with nearly 13.7

Click the invitation link to register an Atoshi account, we BOTH get 23,000 ATOS FOR FREE.

My invitation code:X6C8JK

invite.atoshi.org

English

Bee Network is the world’s largest Web3 ecosystem platform. The all-in-one Web3 super App,integrating Bee mining, wallet & DEX, social and games. Register today and enter my invite code mjeleel2013 to claim 88 $Bee for free. Download at j.bee.com/s?a=mjeleel2013

English

M J JELIL retweetledi

V5.1 will introduce the following major updates:

• Launch of the InterLink Private Mainnet Chain

This is a major milestone as InterLink moves closer to real infrastructure. The Private Mainnet will serve as the foundation for everything ahead, from global payments to real-world asset integration.

• vITLG Migration from Off-chain to On-chain

Users will be able to migrate their vITLG onto the InterLink chain. This is a critical step, transforming balances from internal records into real on-chain assets within the ecosystem.

• 2FA Integration for Migration Security

The migration process will include 2FA to ensure maximum security. This protects users from risks and reinforces InterLink’s commitment to a safe and trustworthy network.

• Staking vITLG to Earn ITL

vITLG will become productive. Users can stake and earn ITL, unlocking real utility and moving toward a sustainable token economy.

• Wallet UI/UX Refactor for InterLink Chain

The wallet will be redesigned and optimized for the InterLink chain, delivering a smoother, faster, and more intuitive on-chain experience.

• KYC Process Optimization

The KYC process will be optimized to improve speed, accuracy, and scalability, ensuring it meets global compliance standards while supporting a rapidly growing user base.

English

M J JELIL retweetledi

On a scale of 10, what would you rate @scott_itl ? Do you think he meets the requirements for the role right now?

English

M J JELIL retweetledi

English

M J JELIL retweetledi

I think this update should be handled by @scott_itl. However, I do feel that not sharing updates with the community for a long time makes me miss this work, something I’ve been doing consistently for the past year

English

M J JELIL retweetledi

Hi Ambassadors, have a nice day💜

Take a moment to check your Bubble Map in your profile.

Each bubble represents your strong contribution through the amount of ACS you have achieved.🎁

English