Retaish uppal

205 posts

#shareholding" target="_blank" rel="nofollow noopener">screener.in/company/REMSON…

Public holding seems interesting.

It is very difficult to assess when the promoters are selling at all time high revenues and profits and at lowest valuations. Got some confidence to hold on to fairly large position.

Disc: No buy/sell recommendation.

#Remsons

GIF

Manojeet Das@Manojeet_Das

Looks like people are really frustrated with #Remsons How market is valuing this? idk. From valuations point of view the company is available at its historically lowest valuations: 15x PE | Median 32x 1.9x PB | Median 4.2x 0.6x PS | Median 0.8x Available at 4.6x Operating cash flows. 60 Cr OCF. Mcap 280 Cr. Only two pointers that maybe concerning and that may have impacted the short term market sentiments are: 1. Promoter selling by Mr. Krishna Radhakrishna Kejriwal and his wife Mrs. Chand Krishna Kejriwal (69 years old). Krishna ji - He is 73 years old (turning 74 on June 12, 2026). Together they sold shares worth ₹6.31 Cr (1.86%) in May and June 2026. Promoter buying is considered as a positive sign but selling may not be a negative sign. 2. Sudden drop in operating margins in Q4FY26 3. Irregular earnings call - I really hope that they improve this at least and become shareholder friendly. What are the positives? 1. Cash flow positive since inception. Generated 28 Cr free cash. 2. Improving ratios 3. Moving up the value chain in Auto anc. 4. Winning multi year deals from big guys. 5. Posted 25% sales growth and 24% PAT growth. 6. All this with 7 Cr equity capital. At this price and valuations, I see this more of an opportunity rather a risk. Maybe I will be wrong or maybe not. Who really knows? No one. Disc: I'm super biased and rooting for them. Sharing my thoughts. Please please don't take it as a buy/sell recommendation.

English

@DEBU_NEOGI @kushallodha548 Welcome to remsons sir... hopefully now stock will move right

English

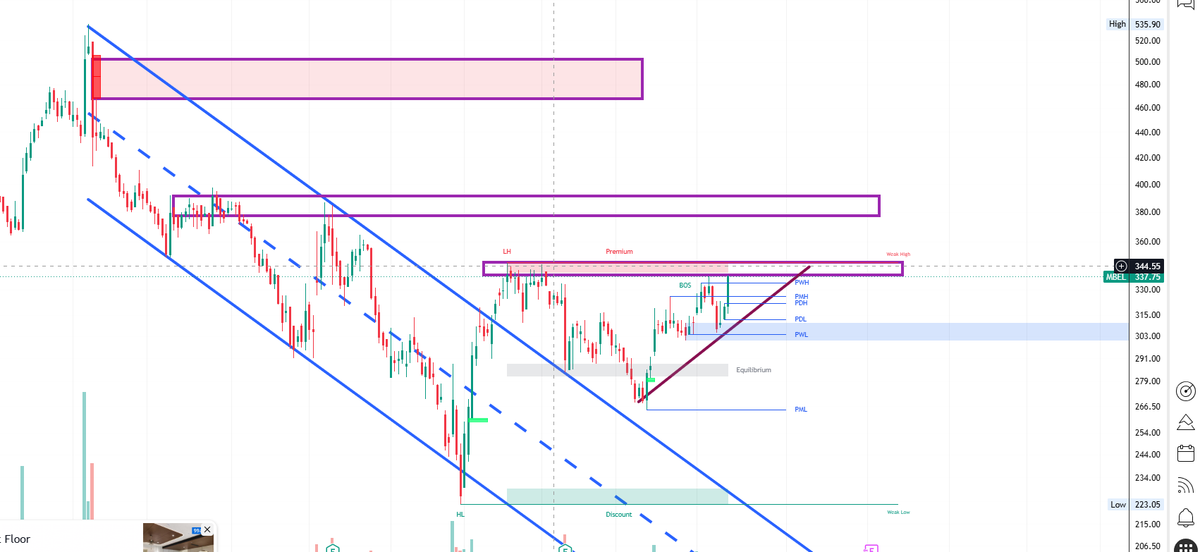

MBEL is looking strong on the charts. If it manages to decisively break the 345 resistance, the next zone to watch could be 380 - 400.

Now it's all about the Q1 results.

They should give a much clearer picture of whether the business is improving enough to support a sustained move higher.

Not a recommendation. I am invested from much lower levels and will decide whether to add or trim the position based on the upcoming results.

English

@MithunSarkari Pl continue ur genuine sharing ...only few post genuine insights

English

Friends, it takes more than double the time and effort to read and decode and present a Annual Report than a concall.

Concall 20-30 pages ( 1 hr)

Annual report ( 250+ pages, but only 70-80 pages to concentrate finding those and reading those)

I posted 3 Annual reports so far

TMPV

Aerofkex

Poonawalla

Atleast read once 😃

Seems it's a waste of time for me.

What do u suggest, shall I stop posting Annual reports?

English

Froths are cleared - People are suddenly bullish 😁

Water stocks are back with a bang!

#EMS up 42% in 3 months

#Wabag up 68% in 3 months 🔥

#DENTA up 33% in 3 months

#EIEL up 48% in 3 months 👏

Watch out for proxies - they will also do well in these times 😌

Arka Bhattacharjee@niveyshak

Govt slashes Jal Jeevan Budget by 46% 👎 This news will clear lot of froth tomorrow from the water stocks! If the stocks weren't performing, this is the reason. 👏 Expecting good returns after this because weak hands will be out 🔥 #EMS #WABAG #DENTA #EIEL #WPIL #ENVIROINFRA #IONEXCHANGE

English

@Manojeet_Das Please throw some light on remsons promoter selling shares again

English

I’m not doing anything.

Pls don’t take actions on my conviction 🙏

Sarath@Sarath12255718

@Manojeet_Das @EquityValueIn Bro what to do with the Infobeans? Literally bleeding everyday. One side conviction says, from the perspective of IT some of the companies may do well and strongly feel Infobeans can do well but as a sector wise, this was the worst thing that can happen to IT. What will you do?

English

@Manojeet_Das I think he might have resigned due to no concall...no clarity on promotor selling ...might be integrity man.something he may felt wrong .

English

Remsons CEO was a part of my investment thesis.

The resignation came out of nowhere. However the reason mentioned is pursuing new professional opportunities.

He grew Remsons from 120 Cr in 2018 to 470 Cr in 2026. Spent reasonable time here. Reasons seems rational.

Let’s see who they bring on.

Disc: No buy/sell reco. Holding strong.

Manojeet Das@Manojeet_Das

Looks like people are really frustrated with #Remsons How market is valuing this? idk. From valuations point of view the company is available at its historically lowest valuations: 15x PE | Median 32x 1.9x PB | Median 4.2x 0.6x PS | Median 0.8x Available at 4.6x Operating cash flows. 60 Cr OCF. Mcap 280 Cr. Only two pointers that maybe concerning and that may have impacted the short term market sentiments are: 1. Promoter selling by Mr. Krishna Radhakrishna Kejriwal and his wife Mrs. Chand Krishna Kejriwal (69 years old). Krishna ji - He is 73 years old (turning 74 on June 12, 2026). Together they sold shares worth ₹6.31 Cr (1.86%) in May and June 2026. Promoter buying is considered as a positive sign but selling may not be a negative sign. 2. Sudden drop in operating margins in Q4FY26 3. Irregular earnings call - I really hope that they improve this at least and become shareholder friendly. What are the positives? 1. Cash flow positive since inception. Generated 28 Cr free cash. 2. Improving ratios 3. Moving up the value chain in Auto anc. 4. Winning multi year deals from big guys. 5. Posted 25% sales growth and 24% PAT growth. 6. All this with 7 Cr equity capital. At this price and valuations, I see this more of an opportunity rather a risk. Maybe I will be wrong or maybe not. Who really knows? No one. Disc: I'm super biased and rooting for them. Sharing my thoughts. Please please don't take it as a buy/sell recommendation.

English

Rupesh ji got a good entry and he seized the opportunity good!

Put money more than his annual income at sub 1000 per share. 🫡

Disc: No buy/sell recommendation.

#Macpower see you at 5k Cr Mcap

Manojeet Das@Manojeet_Das

Perception outweighs rationalism in the short term. Decent Q4FY26 numbers: Sales growth: 25% YoY PAT growth: 18% YoY OPM: 16.1% vs 17.8% OCF: 14.02 Cr vs 6.97 Cr Receivables: 46 Cr Vs 34 Cr Recommended dividend of ₹1.5 per share. Waiting for the management commentary. Disc: Invested. No buy/sell reco. #Macpower

English

@niveyshak Maithan alloys is always in news for share buying not for their core buisness ..

English

HFCL Limited | Acquisition

Maithan Alloys acquires 27.53L shares (0.18%) of HFCL shares for ₹50.04 cr

English

@Manojeet_Das Sir ..asset is undervalued...but if promoter is selling.. something bad may be comin..thwy are cheating..they said no promoter selling but they are selling nonstop and no concall this quarter...till now..big shame on REMSONSIND

English

Yet another promoter selling. This is not a good sign.

But, I am holding strong as the underlying asset feels very very undervalued.

Would take this opportunity to highlight the data issue: Quantity and Avg. Price values are interchanged @screener_in 🙏

Disc: No buy/sell recommendation.

#Remsons

Manojeet Das@Manojeet_Das

Promoters sold for a philanthropic activity as per Rahul Kejriwal ji. youtu.be/otbOqLzBD8g?t=… #Remsons Disc: Invested and biased. No buy/sell reco.

English

@ArindamPramnk Ek mera bhi share hai Bade bhaiya Remsons ind down hai 35 percent kya uska bhi analysis kar sakte hai aap ?

हिन्दी

🚨 A Setup Worth Tracking Closely? OM INFRA TECHNICAL ANALYSIS

This stock has given me pain still holding in loss in my portfolio but I am sure when time will come this will recover just like walchandnagar and olectra did wonders in my portfolio which was at once more than 35% loss same like OM Infra now

After spending a long time in correction mode, OMINFRAL is once again approaching a critical zone.

✅ Price is attempting to break above a long-term falling trendline.

✅ The ₹100 level remains the key hurdle. A decisive breakout above this zone could attract fresh momentum.

✅ Interestingly, the current ₹80–85 zone was a major resistance in the past and is now acting as support — a classic example of resistance turning into support.

✅ Risk-reward starts becoming interesting when stocks move from long periods of consolidation into potential trend reversals.

Note:Keep a close watch not any recommendations to anyone once trendline breaks picture will be clear but I would say good levels to add for long term if someone is bullish on this space

English

@Manojeet_Das Promoter sold again....rahul kejriwal told earlier that they will do promoter selling in it..very strange..

English

#Remsons Mcap 320 Cr | PE 17.7x

Margins dipped in Q4FY26

Sales growth: 22.8% YoY

PAT growth: -52.8% YoY

OPM: 8.41% vs 10.32% → I hope that management clarifies.

Depreciation and Amortisation and interests expenses ate up the profits.

EPS jumped from ₹1.3 per share to ₹1.5 per share due to one time sale of shares of Astro Motors.

Borrowings: 98.4 Cr vs 86.1 Cr

OCF: 59.93 Cr vs 22.17 Cr

Disc: Invested. Holding strong. No buy/sell reco.

Manojeet Das@Manojeet_Das

#Remsons Mcap 430 Cr Yet another consistent set. Q3FY26 numbers: Revenue growth: 20% YoY PAT growth: 34% YoY EPS growth: 29% YoY OPM: 12% Vs 12.08% Disc: Invested. Biased. No buy/sell reco

English

it's like a guess work to be speaking on a thing which may happen in future i mean in terms if how the distress may affect.

That said, remsons atleast in terms of fundamentals and CMP is ok it was even at 120 odd levels. the current quarter shows margin stress.

the micro cap status ain't helping as well

English

@kishorekc506 @Sahilpahwa09 Sahil ...any view on remsons ... I think kishore has asked number of times...though small company but has sector tailwinds..ur views on remsons

English

@Sahilpahwa09 Sir ek bar Remsons ind ka bhi chart analysis kro na bhaiya

हिन्दी

RSI breakdown failed!!!

Price making LL!!

Breakout required for the change in trend!

#POONAWALLA

bhajan kevadiya@bhajanpatel8

@Sahilpahwa09 Poonawala dont sale sir next week se chalega

English

@manish21688 @Manojeet_Das Hi ..how u track today's movement of remsons ...so much volume with some where good delivery ..? But no price appreciation at the close ....anything to share

English

@Manojeet_Das I have also added some. But invested since 110 levels. This could be hammered for these results if valuation were expensive. Would love to hear more from management.

Only positive indicator is, sales growth.

English