Masa’s Son

2.5K posts

Masa’s Son

@masayoshisson

non consensus tech investor. variant views only. unbridled optimist. truth seeker. xbuyside. xmckinsey. +248% since pf inception (jan ‘25)

New York, NY Katılım Ocak 2015

441 Takip Edilen554 Takipçiler

I mean this cannot possibly be good, can it?

The Kobeissi Letter@KobeissiLetter

BREAKING: Iranian officials say their President Pezeshkian will be releasing an "important letter" to the American people in "a few hours." This is set to be released just hours before President Trump's 9 PM ET address to the nation. We will be covering it real-time.

English

trump has zero idea how to get out (and Iran won't let him)

maybe we'll invade, maybe we won't

maybe we'll need to control the strait, maybe we won't

maybe we'll need NATO to step in, maybe we won't

maybe we'll need to make a deal, maybe we won't

deception has its limits

Al Jazeera Breaking News@AJENews

BREAKING: US President Donald Trump threatens to halt weapons supplies to Ukraine unless European countries agreed to join a coalition to secure the Strait of Hormuz, the Financial Times reported.

English

pulling out of the war now is about as dumb as a move as we could make for the future of peace and stability of the region and the world. yes, I know that probably means many more Americans would die as a result, but that is the price required at this point for the goals of our values.

withdrawing and leaving the ROW to figure it out and probably giving Iran some control of the SoH longer-term is economically, and in terms of stability, worse than really anything possible. even maybe having nuclear capabilities (maybe!)

know this will piss people off, don't care. never supported this to start, but now we must finish it or there will be far worse consequences. leaving now is because Trump can't stomach a recession instead of actually being America First, which right now is all I am thinking about. I love this country, I love our troops and I love you all

English

Imagine Trump’s announcement tomorrow night is just him saying he’s sending troops to occupy Iran lmfao that’d be unfortunate.

English

life or death for GCC and Israel

I expect this to keep the US engaged wsj.com/world/middle-e…

English

the winning formula is economic pain

since Iran will control the strait post war, it'll get what it wants (and is likely to make a lot of money from it)

it knows that is has leverage over the western AI supply chain through Taiwan and South Korea

erosion of the petrodollar means structurally higher borrowing costs for the US and inflation in the US whether trump likes it or not

will be interesting to see if we see more escalation on the back of that (potentially instigated by Israel)

clear win for Iran, China and Russia

clear loss for US and Israel

unimaginable loss for GCC and Europe

COMBATE |🇵🇷@upholdreality

Iran FM Araghchi: "No negotiation has taken place. We have not responded to the US proposal and we have not given a counter-proposal. Trust with the US is at zero. We are waiting for their ground troops."

English

See why we ripped today?

First Squawk@FirstSquawk

TRUMP SAYS U.S. DOES NOT REQUIRE A DEAL WITH IRAN IN ORDER TO WITHDRAW

English

I don’t buy this at all

2-3 weeks before US withdrawal means: either Iran tries to attain primacy in the Middle East now or never

blank check for Israel to go rogue

tail risk is that an abandoned strait means Europe and Asia (excl China) get cut off

First Squawk@FirstSquawk

TRUMP SAYS U.S. DOES NOT REQUIRE A DEAL WITH IRAN IN ORDER TO WITHDRAW

English

@ContrarianCurse you’re fully missing the social implications

quite literally the bear case given trump handed the dems the landslide

English

Thinking through AI backdrop. Sorry if I ramble along here.

Few things I think are absolutely true:

1) prob will never be enough tokens again

2) we are selling compute for way below cost

3) economics for the labs vs the semis that enable it, even though they are codependent are totally out of whack

Three things that are extremely important to the LT health of this trade:

1) there is capital willing to be burned

2) we keep developing harnesses/organization of agents in novel way to extract productivity and output

3) we need to absolutely continue to see leaps in performance per rack/w/etc

Its then a race against time, what comes first?

Do we run out of capital to burn? Most likely to would lose the highest cost token producers, and compute would get even more expensive (due to demand) - resulting in a windfall for those that have better cost curves. This would give headroom for the labs to raise prices

Does one of the labs gain enough confidence that they can raise prices? I would argue Anthropic could do it today, but will probably choose to burn another 50b+ to keep the momentum. I'm not sure they are wrong, but IPO window needs to stay healthy (and is somewhat tied to what SpaceX can get done)

Or can NVDA achieve cost does fast enough + price increases that you get a narrowing in the growth in demand and the growth in compute supply to a better ecosystem level.

We will see. But the market currently is not optimistic that we are on the right path.. depends on the month though

I am long infra/equipment/and supply chain that I think have already won, and the advancements needed to enable the compute scaling which is essential to keeping this whole thing going

English

Risk/reward seems attractive:

Token consumption accelerating, GPU per hour rental prices going vertical and Tech valuations are broadly below their Covid and Deepseek lows.

Some high quality secular growth names are at mid single digit multiples on real 27/28 numbers.

English

Remember when people were talking about just selling everything and staying in cash for the rest of the year in January because the month was so good?

lol I was one of those people.

English

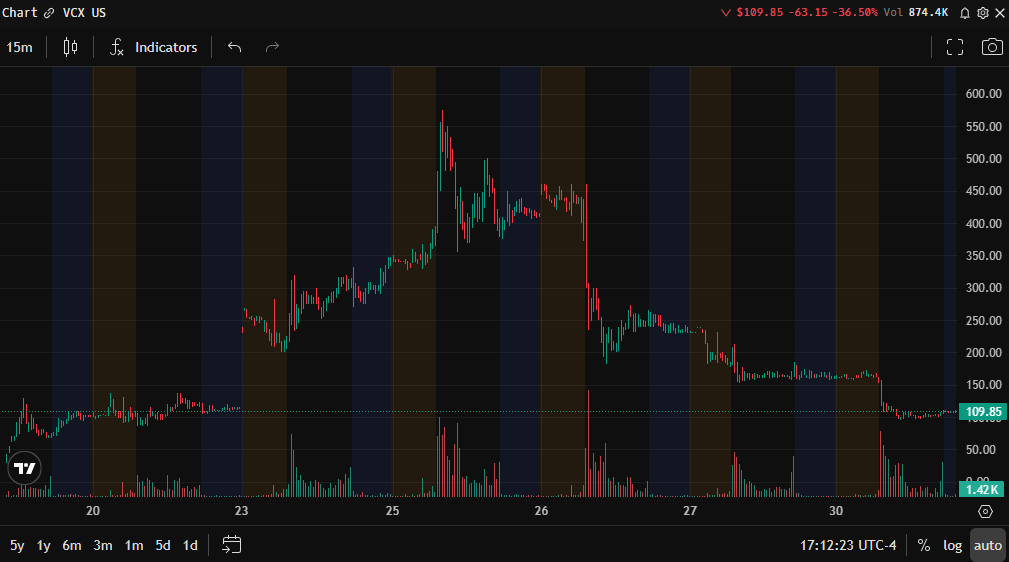

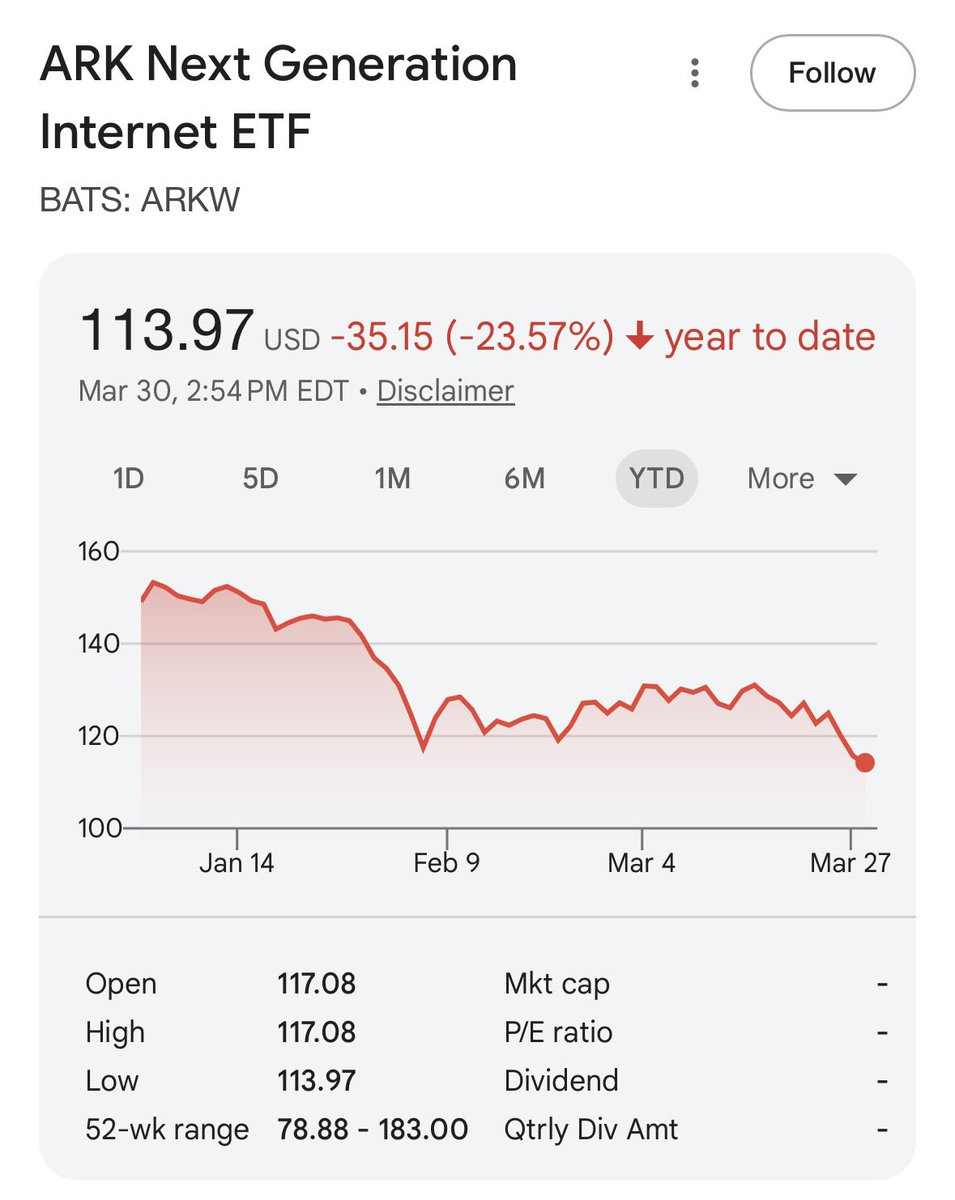

zero humility and learning from 2022

just keeps lighting capital on fire

how do you justify this @CathieDWood?

I wonder what tgm/ coleman and laffont/ coatue are up to

English

“never admit defeat” - trump, c. 1970s/ @rabois 2026

Keith Rabois@rabois

@boreas_eth opening tomorrow per Trump.

English

@jukan05 totally in alignment there

but, the voices get louder

that said, fully appreciative of all your great work!

English

@masayoshisson I don’t cherry-pick information. I try to read and consider everyone’s perspective.

English