mathdhdh

253 posts

mathdhdh retweetledi

There are so many paths a strategy/portfolio of stratgies can take.

You backtest and you get all these stats about your portfolio and you think thats it but no thats a perfect path.

Bakctest is path DEPENDED.

Its a perfect path but the future is not a straight path what if the trades come in different order? what if you miss some trades ?

what if a strategy you made decayed and its losing money?

Never trust the backtest and always size up for atleast a 2.5x DD more than what you see so if your target DD is 10% max your backtest ideally should show 4.5% historical DD and thats your risk.

Monte carlo proves that.

It is a computerized mathematical technique that predicts the probability of various outcomes by running thousands of random trials, accounting for risk and uncertainty in unpredictable systems. It is used to model scenarios in finance, engineering, and project management where variables are uncertain, providing a range of possible results rather than a single "best guess"

These are the tools i use to deploy my systems correctly on prop firms.

English

mathdhdh retweetledi

Systematic trading is the ONLY way to long term profitability in this game.

I have been trading for the past 6 years now and i tried and tested every single system you can think of.

99.9% of gurus dont even have an edge they just cycle accounts.

I am not saying thats bad if that makes them money but it doesnt make sense to learn from someone that simply has no edge and gambles right?

If you want to get profitable and actually make money long term study systematic trading-rule based trading.

English

mathdhdh retweetledi

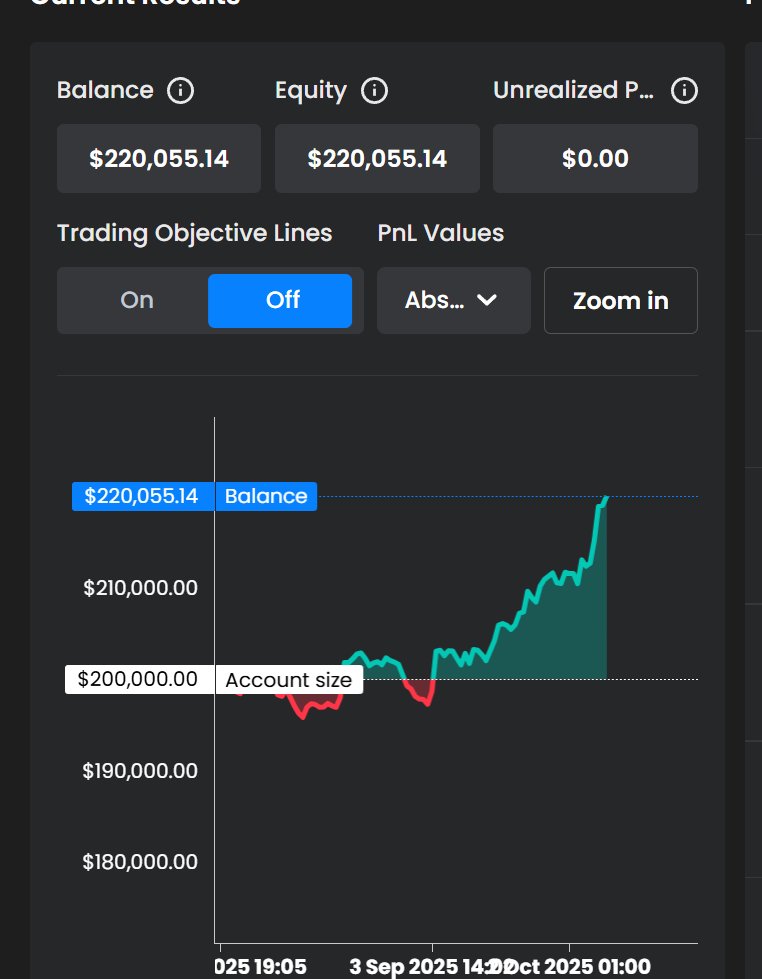

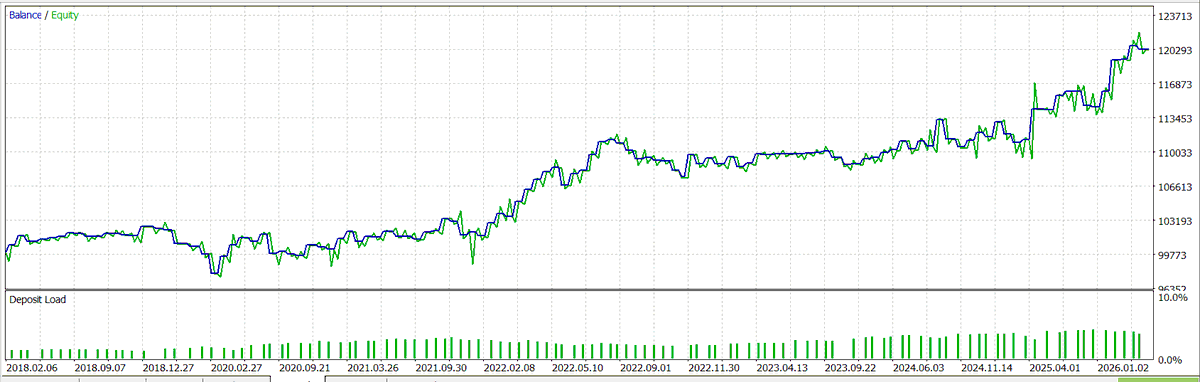

Another portfolio done today for my FTMO accounts.

This one is specifically made for the standard account type.

News close included.

EOD close included!

No over the weekend filters.

Performance drops but we still adapt and make money and thats what matters!

4 strategies so far and we will scale to 6 strategies on this account next week!

Either you ADAPT or you stay behind.

Its up to you to make it happen!

English

A lot of traders are obsessed with high win rate strategies.

Not because they’re better…

but because they’re easier to deal with psychologically.

Winning often feels good.

It builds confidence.

It reduces emotional stress.

But high win rate ≠ profitable.

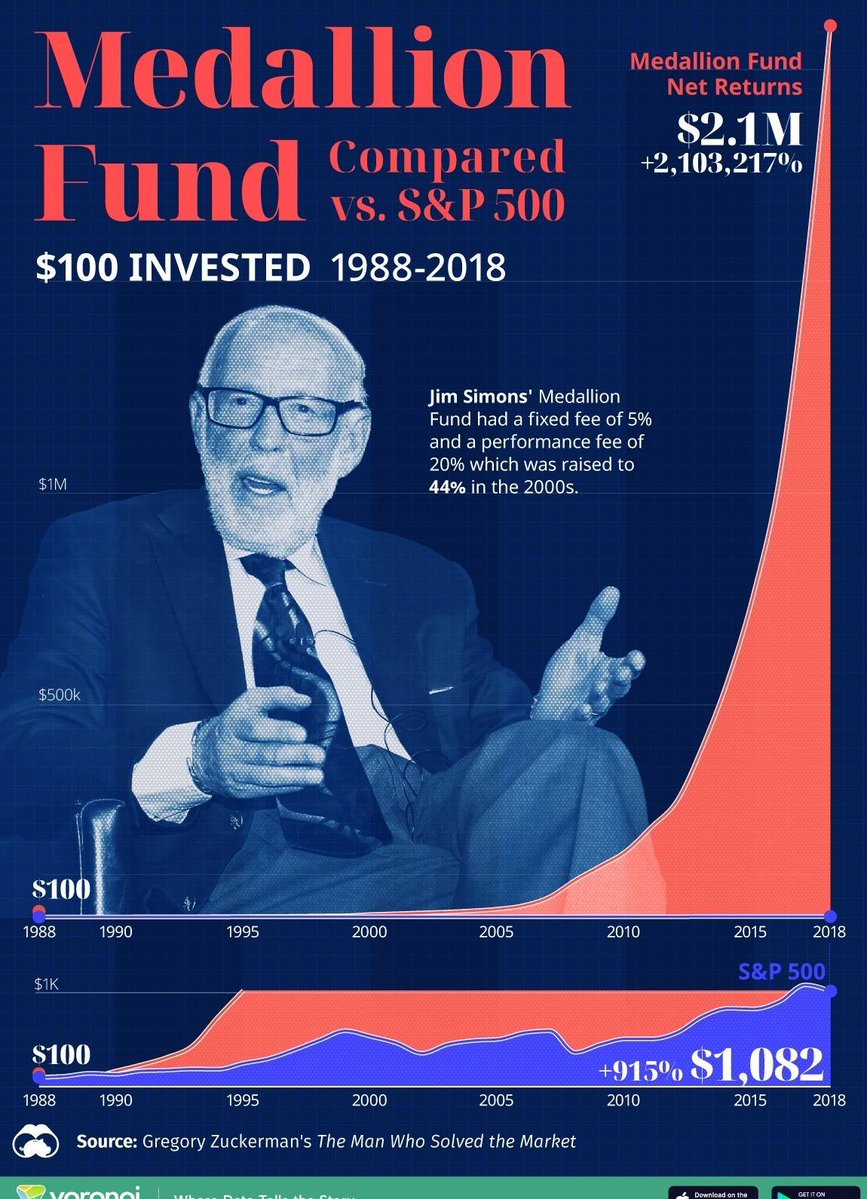

The goat of trading Jim Simons was trading mostly mean reversion/short-term statistical patterns/inefficiencies/micro-patterns

Below is a mean reversion portfolio I run, focused on indices.

Mean reversion is one of the most consistent edges in the market especially in range-bound conditions, where price oscillates between extremes.

The concept behind mean reversion is simple:

When price deviates too far from its average value,

it tends to revert back.

Why?

Because markets are driven by:

overreaction

short-term imbalance

emotional positioning

And those extremes don’t sustain.

This is where most traders get it wrong.

They chase moves after the expansion.

They buy when price is already extended.

They sell when the move is exhausted.

That’s not edge.

That’s participation in the crowd.

Mean reversion does the opposite.

It looks for:

exhaustion

overextension

liquidity events

And positions for the snap back.

But here’s the part most people miss:

Mean reversion does NOT work in all conditions.

When the market is trending strongly,

what looks “overextended” can keep going much further.

That’s why combining strategies is critical.

Mean reversion → performs in ranges

Breakout / trend systems → perform in directional markets

Together, they allow you to:

adapt to different regimes

smooth your equity curve

reduce dependency on one condition

This is how professionals think.

Not:

“What’s the best strategy?”

But:

“How do I cover all market environments?”

The edge isn’t just the setup.

It’s:

understanding when it works

understanding when it doesn’t

and combining systems accordingly

At its core, the logic remains simple:

When price overextends…

it tends to revert.

The key is knowing when that actually applies.

Below is a very simple portfolio using this concept mean reversion combined with breakouts!

English

@TheWolf534 i find it very hard to find mean reversion on the lower timeframes

English

mathdhdh retweetledi

Richard Dennis one of the best traders of all time built his edge on breakouts.

He accepted small losses for big trends.

He always believed that even if he publishes his rules on the newspaper nobody would follow them.

Discipline and consistent execution is key for any system to play out.

I applied that same methodology and discipline

and DOMINATED prop firms.

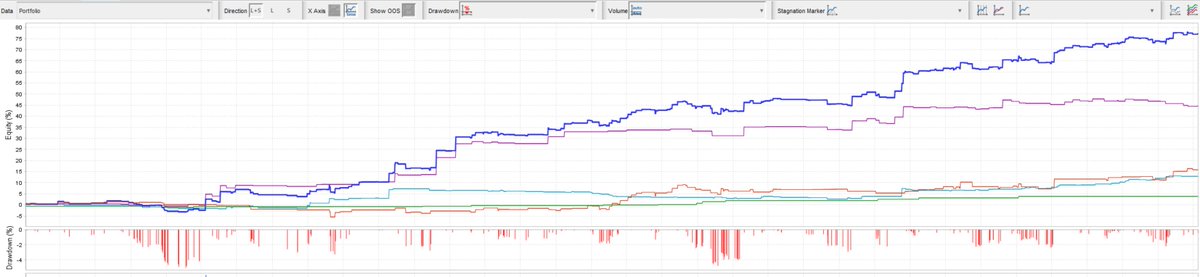

Below is a simple portfolio of 2 Breakout Systems Tested from 2011-2026 and used on my FTMO accounts.

English

@TheWolf534 since i started using this i avoided a lot of bad strategies that is so true

English

mathdhdh retweetledi

When i create a strategy one of the most important things i focus on is if my strategy generalizes across assets.

What i mean by that is that for example if i have a mean reversion system on NAS100 it has to work on SP500 too and US30....etc

If it only works on NAS100 thats a bad sign.

Example Below i have a mean reversion strategy.

It works on all INDICES.

70% win rate across 15 years sample size.

Just 2 criteria as robust as it can get.

These are the stuff i trade on my live accounts.

STOP HANDPICKING INDICATORS AND CREATING A FAKE BACKTEST.

Its a complete lie and it wont work in live trading.

English

I have built the most COMPLETE Prop Firm portfolio in the industry.

Breakout on gold(Long Only)

Breakout on BTC (Long Only)

Mean reversion on BTC

Mean Reversion Indices

Deep Mean Reversion on Indices

Short Mean reversion on Indices

Breakout On Indices

Every strategy was build with a HYPOTHESIS first always.

No data mined stuff just simple stuff that have a 30 year track record from famous funds that still work with some small changes.

Creating a portfolio is not about stacking random edges.

It's about stacking the right ones.

Negative Correlation as always!

Will use this on FTMO and many other firms that meet the criteria.

English

@TheWolf534 true i only found consistency when i started using rule based trading

English

mathdhdh retweetledi

SYSTEMATIC TRADING-RULE BASED TRADING

Wins every single time againist DISCRETIONARY TRADING

Discretionary traders most of them have no edge no positive expectancy

Even if they have an edge their execution is so shit that makes it impossible to make money long term

Discretionary traders trade based on their mood or intuition..etc

They keep changing risk or rules

And that is why they fail long term

Systematic trading wins in every way possible

Also systematic trading executes better than 99% of discretionary traders every single time

That is why i trade fully automated with prop firms.

Less room for error

Less screen time

English

mathdhdh retweetledi

Breakout trading isn’t new.

It’s one of the oldest edges in the market.

Long before indicators, YouTube strategies, or retail hype…

Traders were already exploiting one simple idea:

When price breaks out of a range,

it tends to keep moving.

In the 1980s, the Turtle Traders proved it.

Decades later, nothing changed.

Here I have a very SIMPLE system on the USDJPY.

Its not a classic breakout system.

This one trades with NEGATIVE RR.

TIMEFRAME: Daily

Win Rate 74% on shorts and 69% on Longs

DD under 7% on an 8 year sample

I don't usually trade stuff like this but since negative RR is very popular amongst the trading industry especially for futures prop firms i decided to post something related.

English

@TheWolf534 we actually have a chance to escape all this

You share some good stuff man

English

In school you were taught to play it safe.

Get a stable job.

Follow the path.

Don’t question the system.

But the people winning in life?

They did the opposite.

For decades, systems were built to suppress individual power.

The era of independent thinkers and dominant individuals faded, replaced by structures designed to reward compliance over capability.

Being well-rounded lost value specialization took over.

Proof of work became less important than credentials.

Stability replaced freedom.

You were molded to operate within limits:

a single position, a single authority, a fixed set of duties.

Stay in your lane, follow instructions, and rely on others to complete the bigger picture.

That was the trade-off: exchange your full potential for a sense of security. Let systems choose your direction. Let a title determine your value.

Everything around you was built on that model.

BUT we are in a NEW ERA.

In todays world you have the opportunity to build stuff that 20 years ago it would take a whole team of 200 people to make.

5 years ago i went into trading trying to escape the norm and make money doing what i love most.

Trading has been a wild ride with many ups and downs these past 5 years but each day getting closer to that freedom of owning your time and being able to make a living full time with trading has been a blessing.

Go againist the norm.

Choose uncertainty and risk it all trust me its worth it in the end.

English

@TheWolf534 working to get there soon!

that kind of money is life changing indeed

and from there is just scaling and scaling

English

mathdhdh retweetledi

THE PROP FIRM BUSINESS

If you can find and build 5-6 uncorrelated edges you can literally scale to multiple figures with prop firms.

This is a new low frequency portfolio that i am working on and its currently at 4 strategies.

Lets talk numbers.

$1.000.000 in funding

If you can average 10-15% returns yearly with moderate risk thats 120k$ profit after split.

Which comes to about 10k per month.

These returns are very doable with a well rounded portfolio and it will be life changing for 99% of people.

Leveraging beta with prop firms is the easiest way to earn money in trading.

English

@TheWolf534 Breakout systems are one of the most stable systems i have in my portfolio at the moment

English

mathdhdh retweetledi

INDICES tend to have a mean reversion effect.

Which means that after going down they usually snap back to the mean.

This strategy here on NASDAQ takes advantage of this effect.

Very simple and robust and tested from 2013-2026.

I will be adding this to my FTMO portfolio soon.

Stop using random criteria and too much parameters when creating a strategy.

The more criteria you have the higher the probabilities are of not working in the future.

56.30% WIN RATE

MAXIMUM DD OF 5%

COMPLETELY UNCORRELATED USING THE CORRELATION COEFFICIENT SHOWING NEGATIVE CORRELATION WITH THE OTHER SYSTEMS IN THE PORTFOLIO

SIMPLE WINS AND SIMPLE IS SCALABLE REMEMBER THAT.

English