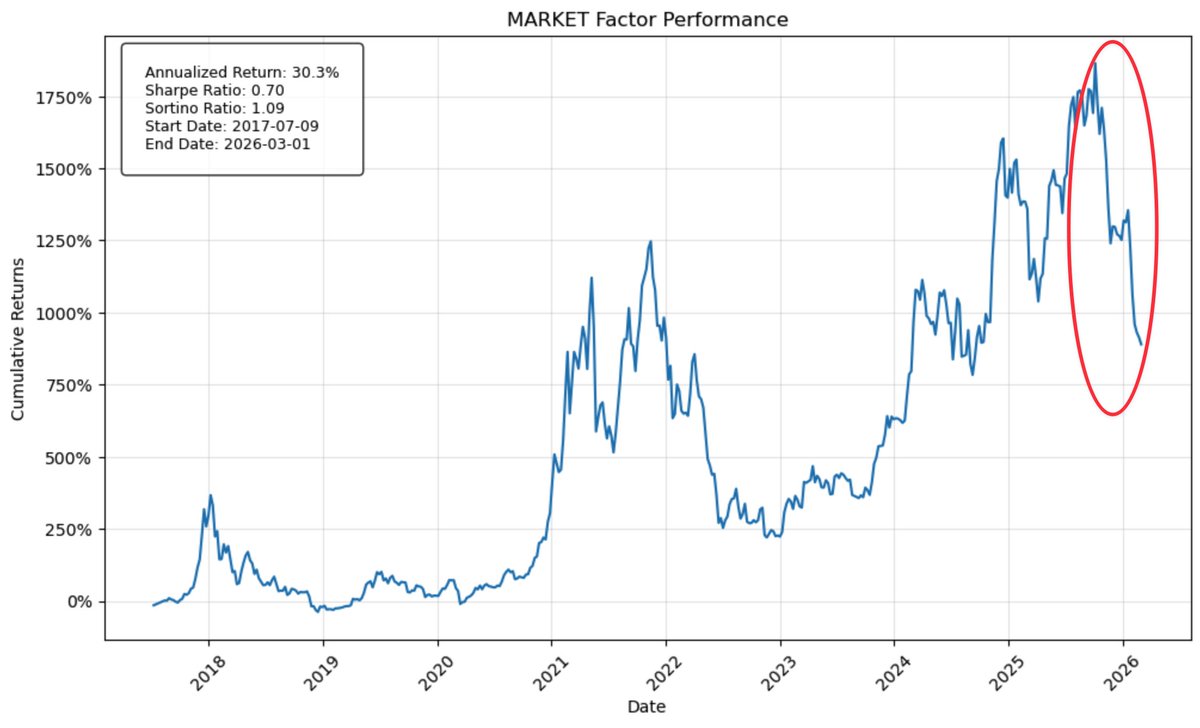

How much was the Google Quantum AI mention worth to ALGO?

Roughly $302M, after backing out the broader crypto market move.

Algorand already had the technology. The paper got the market to price it.

English

Matt Brigida

25 posts

@mattbrigida2

Chief Economist @ Algorand Foundation and Professor and Finance/Accounting Chair @ SUNY Polytechnic Institute. Views are my own.