Mavix

8 posts

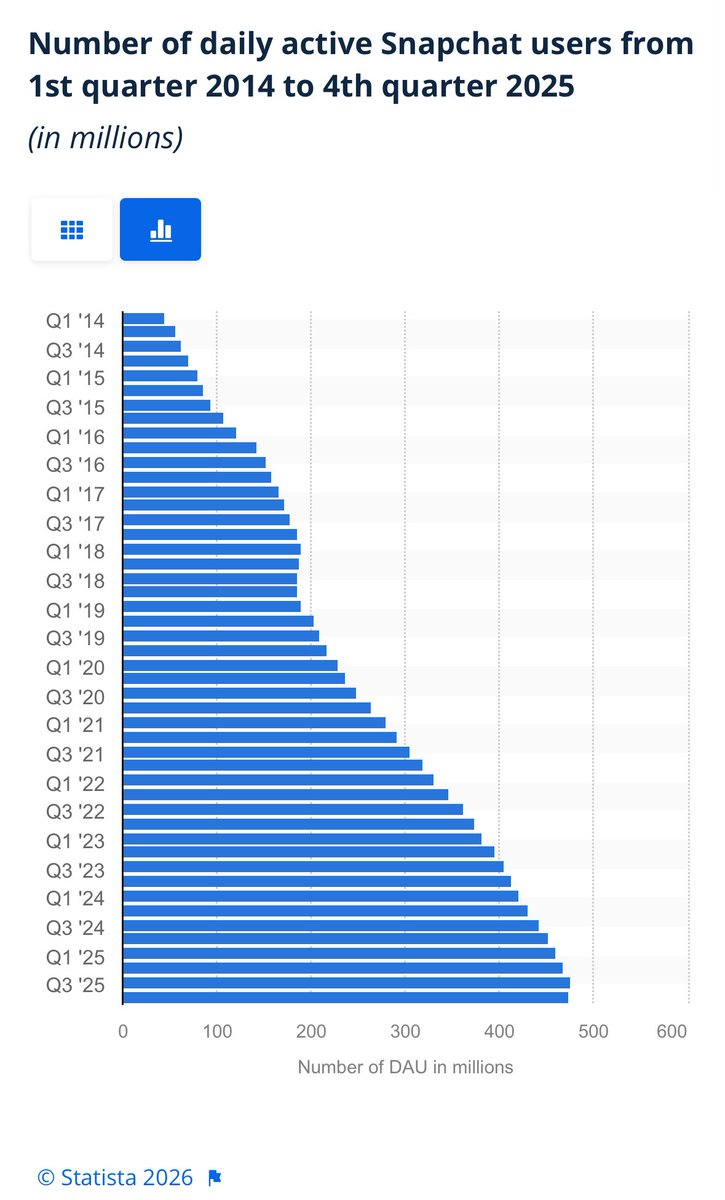

Bought some $SNAP here at 5,17 USD/share. My reasoning⤵️ • Profitability Pivot 💰: The company reached a major milestone last quarter, turning profitable for the first time. • Monetization Upside✅: With a massive user base of 1 billion Monthly Active Users (MAU), even a modest 1% conversion to their new $1.99/month memory storage tier would generate an additional $240M in annual high-margin revenue. • Operating Leverage 💸: Based on recent quarterly performance, incremental revenue is now largely flowing directly to the bottom line. • Conservative Valuation 3️⃣0️⃣: Even with a minimal 1% conversion rate on this single new product, the stock would trade at a 30x earnings multiple. This excludes growth from their other three subscription tiers, including Snapchat+. • Growth Momentum 📈: Total subscriptions have surged 71% over the last 12 months, amounting to 24 million, a large portion of these are Snapchat+ subscribers. • Shareholder Yield %: Management has accelerated share buybacks with the explicit goal of achieving "net-zero dilution," effectively neutralizing stock-based compensation. At these levels, the risk/reward profile looks highly asymmetric.