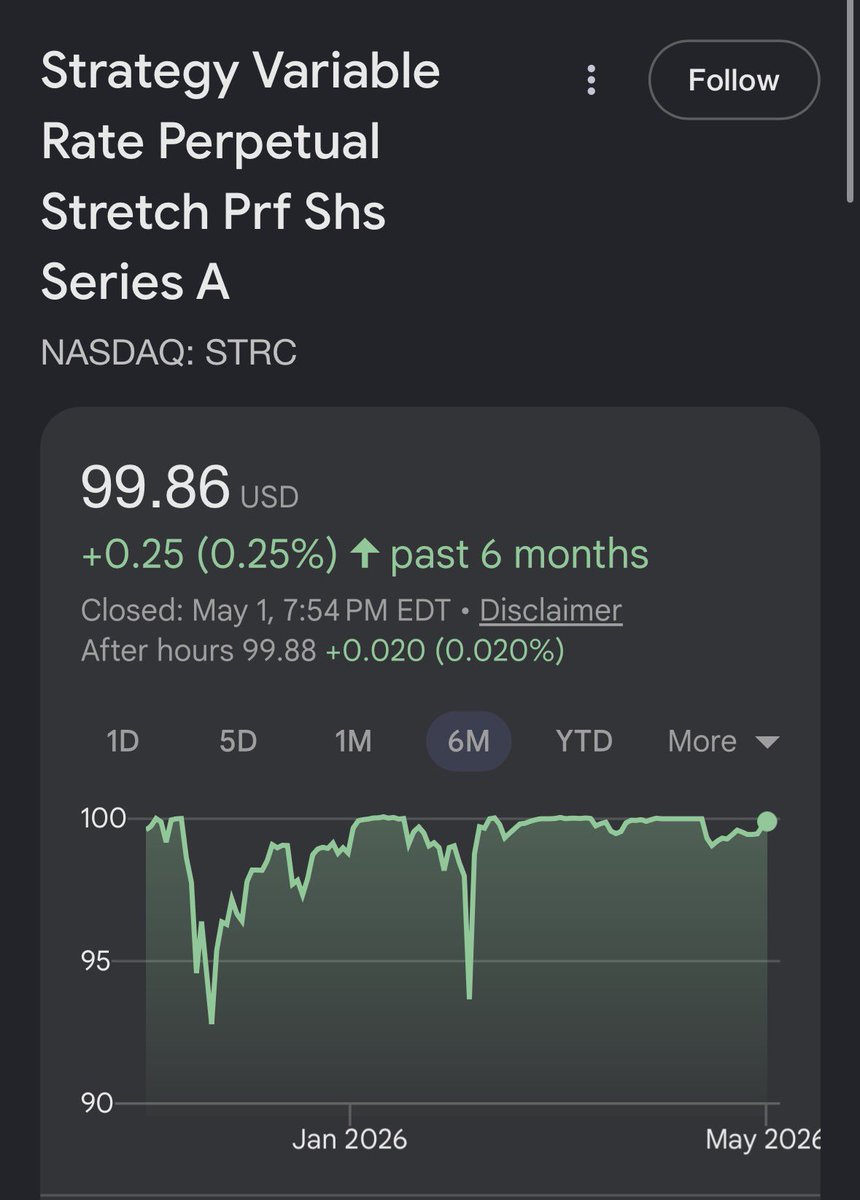

The God Particle@_Sgr_A_Star

$IREN

My expectations heading into IREN earnings week.

1) I expect IREN to miss the headline numbers, revenue and EPS consensus estimates.

Current (Bloomberg) consensus estimates are:

Revenue: Total $216.6M ($83.1M Cloud)

EPS: -0.24

In Q1, IREN's Bitcoin wallet generated sales (revenue) of $110.9M, short of consensus by more than 20M.

This miss is primarily due to the weakness in the price per bitcoin in Q1, as well as the reduction in hash-rate as the company accelerates disconnecting bitcoin miners in preparation for conversion to GPUs.

Fact is, the quicker they can do away with bitcoin mining, the better. At this point, it's frankly inconsequential.

My current estimate for AI Cloud revenue is $81.3M but this assumes that the company completed the retrofit of Prince George and the installation of the 23K+ GPUs at that site.

Based on the most recent comments from Kent Draper on the Jefferies fireside chat, he confirmed that all capacity (50MW) at PG is currently operating GPUs.

Kent's Quote:

So our Prince George site- the entire capacity of that site is being used for our existing fleet of GPUs.

Taking Kent's words at face value leads me to believe that it's probable the company met their ARR guidance for PG of ">500M in ARR by the end of Q1".

When you take into consideration the ARR they exited 2025 with, the number of GPUs in their possession, and the fact that all 50MW were operating GPUs as of late March (per Kent's interview), it allows me to back into the $81.3M AI Cloud revenue estimate.

I'd consider this a major win in their AI Cloud execution, but it won't make up for revenue shortfall from consensus.

How the market trades these (miss) results will depend on....

2) I expect IREN to to announce a deal between now and the earnings call.

Not because I have any inside information, nor because I think they *have* to announce one, but because I think it's the perfect time for "The Three Cs" to realign. The Microsoft deal is fully capitalized. It's past the commercial and capitalization phase, and now deep in the build-out phase. It's the perfect time for the next one:

Capacity: there is 110MW of available capacity at Mackenzie and Canal Flats and another 450MW available at Childress along with everything that just energized at Sweetwater 1 (will be in phases). Their capacity is diverse! They can do liquid and air cooled!

Customers: there is no shortage of demand for compute right now. Every industry metric validates it. They've told us for over a year now that there is appetite from customers for well more than 200MW. In Feb they told us that they have *multiple advanced* negotiations with hyperscale and enterprise customers. That customers aren't a constraint - choosing the right long term partnerships is their focus.

Capital: the balance sheet is strong and supports growth. Capital is lined up wanting to fund DC builds. The company has access to proven multiple sources of capital. Billions of cash on hand, GPUs you can borrow against, data centers you can borrow against, and now even an ATM you can withdraw equity from.

The Three Cs are as aligned now as you could possibly hope for, and I believe there are signs:

- Massive hiring spree all over the world, including now in Australia - 147 active openings. Coupled with the massive marketing campaign down under.

- Disconnecting of 100MW+ of miners at Childress. You don't disconnect that many miners unless you have plans for that capacity.

- Order of 50K air cooled GPUs with 1/3 slated for Childress

- Disclosure of the "multi-billion $ deal with software" at the last earnings call. (This wasn't an accident)

- Sweetwater energization.

-Dan was stateside recently per his tweets at Childress

-At every turn a new story about how compute constrained the world is.

CCCs aligning.

3) I expect/hope for information on:

- Current status of Horizon 1-4. Has Horizon 1 been delivered? If not, why not?

- Outlook for VR200 availability and prospects of MSFT taking the VR200 option.

- Update on the "multi-billion dollar deal with software"

- If they're not going to share what ARR they exited the quarter with, I'd expect an updated contracted ARR number. Last quarter it was 2.3B - I'd expect it to be significantly higher, as I'd expect the last 100M+ at PG to be contracted, and I'd hope they've contracted chunks of the 50K B300 associated with 1.3B of ARR.

- Outlook for Sweetwater - when may we see the first operational MW there?

- We all see the smoke, but are there actual fires in Australia?

- Status of the "other projects in our portfolio that are potentially also included in Batch Zero"