Sabitlenmiş Tweet

A New Year’s resolution! The #REconomy Podcast™: What Will it Take for the Housing Market to Rebalance? blog.firstam.com/economics/the-…

English

Mark Fleming

4.1K posts

@mflemingecon

Chief Economist @FirstAm. Father and dismal scientist. Runner, biker and beer maker. Views expressed here are personal and not the views of my employer.

The market has reacted jubilantly to Powell's comments at Jackson Hole today. Powell mentioned that the balance of risks between inflation and employment "appears to be shifting", suggesting that conditions "may warrant" interest rate cuts. He indicated that, though the economy remains resilient with a still-stable labor market, the downside risk to employment has grown. These seem to be words that the CRE industry has been waiting to hear for several years. Finally, does this mean more rate cuts are at hand? It certainly seems more likely - data from CME shows that the market expectations of a quarter point rate cut in September has jumped to over 90%. However, caution remains warranted. Remember - the Fed only directly sets short term interest rates. Variable rate commercial mortgages are typically priced based on a spread above SOFR, so Fed rate cuts would directly impact these mortgage rates. However, long term interest rates, like the 10-Year yield, are set by the market*, and it is the 10-Year Treasury yield that many fixed rate commercial mortgages are priced in relation to. Why am I throwing just a touch of cold water on an otherwise positive rate story? Because it's plausible that short term rates decline while long term rates stay where they are. This would not provide nearly as much relief to commercial borrowers as the market seems to be expecting. * The Fed can indirectly influence long-term interest rates by buying and selling bonds. #JacksonHole #Fed #InterestRate #CommercialMortgages

Powell cautiously tees up a cut: “The balance of risks appears to be shifting.” While labor markets remain in balance, “it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers.” “This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

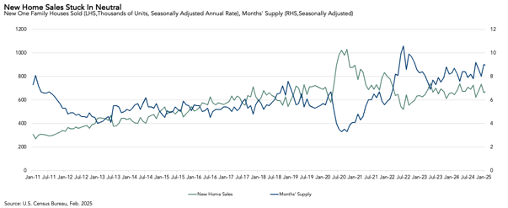

Housing affordability had a rough start to the year. However, affordability improved in February due to slower price growth, a decline in mortgage rates, and positive income growth. Inventory is expected to rise in 2025, which should continue to cool price growth and improve affordability. In this latest research, @mflemingecon lays out three scenarios for 2025 depending on how months' supply changes and impacts price growth: 1) If price appreciation stabilizes near where it currently is, affordability will improve by 3.5 percent by year's end 2) If months' supply increases to 6 months, which would indicate a more balanced market, price appreciation would slow and affordability would increase by 4 percent by year's end. 3) If sales outpace inventory growth, prices would re-accelerate. If months' supply falls to levels comparable to spring 2024, then affordability would end the year a little worse than compared to the end of 2024. #Housing #Economics #SpringHomeBuying #FirstAmEcon