Mike Dobbins

1.5K posts

Today, I will give a special shoutout to all XRP HODL around the world.. 🌎

Please comment below "XRP" so my followers & I can follow you..

This way you can get on a fast track to get monetize & paid for posting in X..

To all my followers please follow all who commented! 🙏

English

Mike Dobbins retweetledi

The @Razor5Hole found himself in the middle of a comparative idiom intersection. Nowhere to turn. The pause is his Rolodex of options. Brain speeding through choices like cars running red lights. Sirens sounding. And he chose....perfection.

Sauce Hockey@saucehockey

"That's dirtier than a urinal cake." — 🤢

English

Mike Dobbins retweetledi

WYATT JOHNSTON STANDS ALONE. THE GREATEST POWER PLAY GOAL SCORING SEASON IN FRANCHISE HISTORY 🗣️

- @JoshBogorad

#TexasHockey

English

Mike Dobbins retweetledi

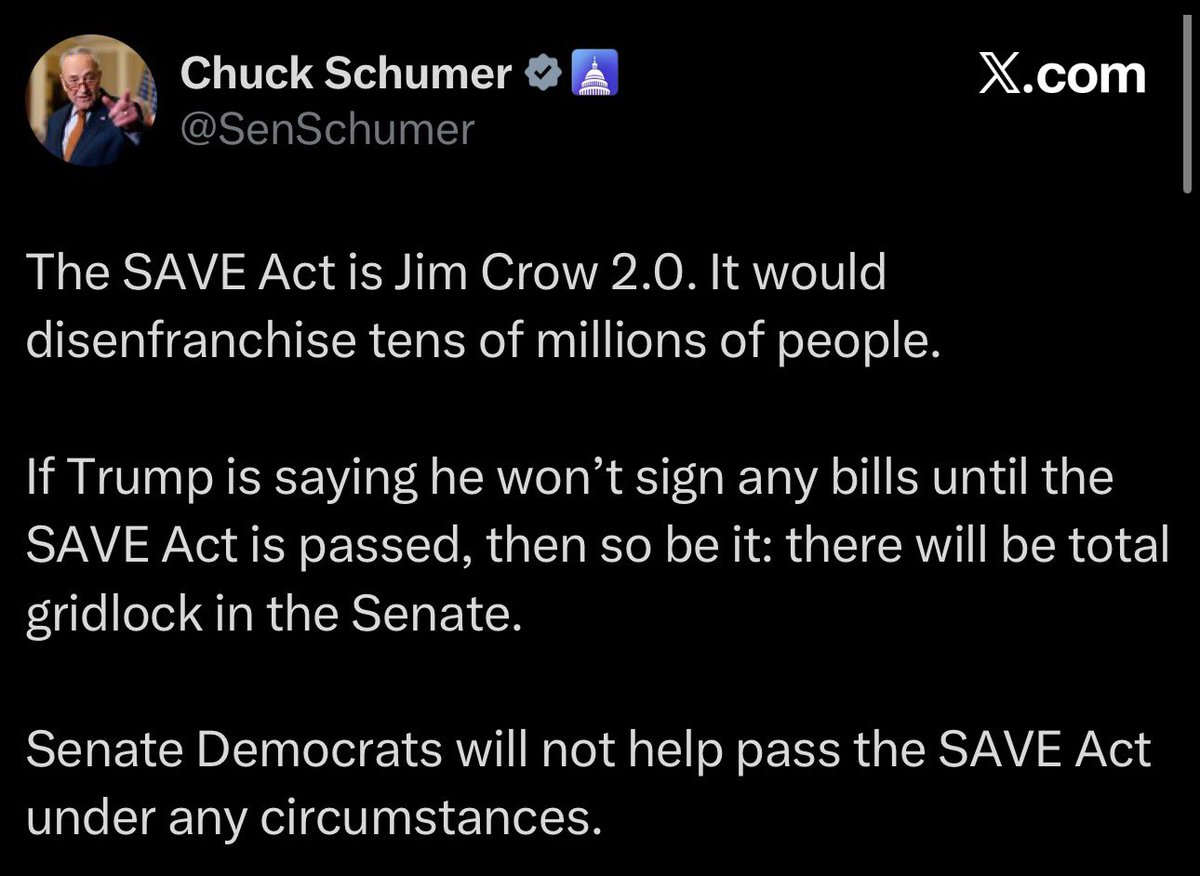

Dear Chuck Schumer,

Hi. Black dude here. I can trace my family ancestry to slavery. I even know where they were slaves. My mom experienced Jim Crow. I think I’ve watched every episode of “Eyes On the Prize” when I was younger.

With that said…

Can you directly explain to me how the SAVE Act is “Jim Crow 2.0?” Literally every black person I know has ID. Literally every black person I know has a car or at least a ride. Literally every black person I know knows how to vote (well… except the ones with felonies… but they don’t count).

With your advanced white liberal thinking, you must know more than me. Apparently, as I experience daily on this app, white liberals are experts on being black; even more so than actual black folks. Perhaps you could explain it like I’m five. I’d look it up on the internet, but Kathy Hochul has already told me I don’t know what a computer is and Joe Biden said I can’t navigate it, anyway.

Looking forward to your answer.

No hugs.

Zeek

English

Mike Dobbins retweetledi

Kept 11 tons of cocaine off American streets.

It’s unacceptable these brave members are not getting paid.

Shutting DHS down only punishes those who keep our nation safer.

English

Mike Dobbins retweetledi

Ok this is literally the most insane, raw, brutal rap song every made

If Drake, Kendrick Lamar, Eminem, Kanye West, Travis Scott, Future, J. Cole, NBA YoungBoy, Playboi Carti, Lil Baby were asked to sing this rap, they would piss their pants

Big G Chris Webby

subs burnt by me

English

@jw1035 @victoryplustv My app crashed at the 3rd period penalty kill and when I reloaded it the game wasn’t listed as available. Missed the hawks tie and the ot goal 😒

English

Mike Dobbins retweetledi

Will not stop until the objectives are met.

Unrelenting. Unapologetic. 🔁

English

Mike Dobbins retweetledi

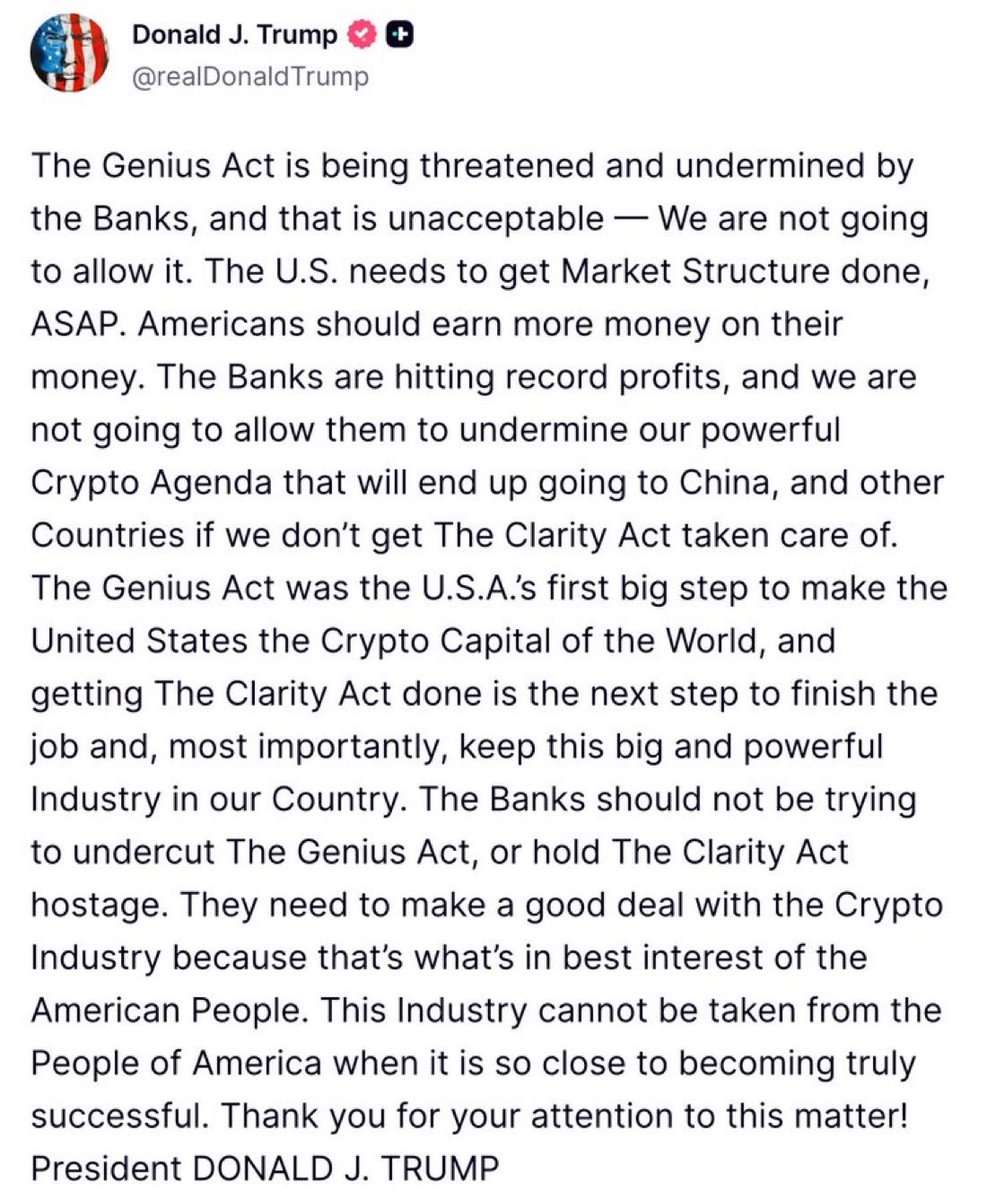

Let me make this very clear: Big Banks (think JPMorgan Chase, Bank of America, Wells Fargo, etc.) are lobbying overtime to block Americans from getting higher yields on their savings—while trying to block any rewards or perks from being given to customers.

These banks, and others, pay rock-bottom rates on standard savings (often 0.01%–0.05% APY), even as the Fed pays them 4% or more. This massive spread fuels record profits, with almost none passed back to their customers / everyday depositors.

Today, the banks are desperately targeting crypto/stablecoins, where platforms plan to offer 4–5%+ yields or rewards. The ABA and other lobbyists are spending millions trying to ban or restrict those yields via bills like the Clarity Act, crying “fairness” and using words like "stability"—when it's really about protecting their low-rate monopoly and preventing deposit flight. This is anti-retail, anti-consumer, and straight-up anti-American.

Next time you see a big bank dropping billions on a shiny new Midtown Manhattan HQ, you know exactly where that money comes from: the non-existent interest rate they “pay” you!

Fortunately, the big banks are losing this fight as customers wake up to the games…

@worldlibertyfi

English

Mike Dobbins retweetledi

For the record.

Jamie Dimon says he wants a “level playing field” for stablecoins. What he really wants is to make sure nobody can offer you a better deal on your own money than tradtional banks can. The president is right to call the banks out on this.

We’ve seen this before. In the 1970s, money market funds started paying real yields while banks were locked under deposit caps. Banks cried “unfair” and “unsafe,” lobbied furiously, and lost. Policymakers chose competition over protection; savers got paid, and banks had to adapt instead of suffocating the threat.

Today’s script is the same, just with better technology. Stablecoin issuers now operate under licensing, 1:1 high‑quality reserves, liquidity and risk rules, audits and strict AML standards. This is not the Wild West. Yet Dimon still talks as if they exist with “no reserves, no compliance, no oversight.” He’s not describing reality; he’s describing a story that justifies shutting down a rival funding system.

The Clarity Act is the real battlefield. On paper, it’s about integrating crypto into U.S. market structure. In practice, the big banks are fighting to ensure that anything that looks like a deposit with yield must either become a bank product or be regulated into irrelevance. “Level playing field” in their vocabulary means: everyone wears the bank straitjacket, or no one plays.

Why? Because yield‑bearing stablecoins blow up the quiet cartel behind record profits. Banks live on deposits that pay close to nothing even when risk‑free rates are high. They earn a clean spread and interest on balances parked at the Fed, while passing little of it through. Savers get crumbs; banks get the margin; inertia does the rest. A credible, regulated stablecoin that passes through money‑market yields detonates that racket: with a few clicks, your cash can leave the cartel.

The president’s critique goes straight at this arrangement: Americans should “earn more money on their money,” and banks should not be allowed to undermine laws designed to make that possible or to stall a market‑structure bill so the whole “powerful Crypto Agenda” decamps overseas. He’s not attacking banking; he’s attacking a model that treats low‑yield deposits as an entitlement and regulation as a weapon.

Crypto‑native firms, for all their flaws, behave like they live in a real market: they build new instruments, disclose, and pay up to attract capital. The banks build talking points and hire lobbyists. Stablecoins don’t just threaten their funding; they threaten their chokehold on payment rails and transaction data.

Call this debate what it is: not a fight over “safety,” but a fight over whether a protected deposit cartel gets veto power over technologies that finally let savers earn something closer to the risk‑free rate. In the 1970s, policymakers chose competition.

In the 1970s, banks were forced to stop hiding behind regulation and compete. If Jamie Dimon wants a level playing field, he should stop complaining and start doing the same.

Rapid Response 47@RapidResponse47

English

Mike Dobbins retweetledi

The “Big Banks”—the very institutions that have held a monopoly and screwed their customers for years, offering near-zero yields on retail Money Market Accounts while crushing low-balance accounts with exorbitant fees—are now doing everything they can to block the Crypto industry from offering real benefits, perks, and rewards on their platforms.

They are the greatest hypocrites and are in mass panic given they know they are losing the digital finance race! @worldlibertyfi

English

Mike Dobbins retweetledi

Mike Dobbins retweetledi

What would happen if you got directly hit by an RPG? This would be the result.

🎥 @BHS_Official_

English