@kieranwgoodwin “ It can’t be valued” is just a ludicrous statement - half the loans in the avg book in April 23 have already paid off.

English

James Morrow

76 posts

Ares: 11.6% redemption requests. Honored 5%. Called it “aligned with the best interests of all stakeholders.” The stakeholders who wanted their money back might define “best interests” differently.

Per Bloomberg, Ares is the latest private credit fund in developed markets to fulfill only a portion (43.1%) of requested investor withdrawals. These requests totaled 11.6% of the fund, exceeding the typical 5% cap. As these headlines multiply, the risk of a "contagion of concern" grows—fueling fears of further redemptions and forced liquidity sales by funds. #economy #markets #privatecredit

At an annual meeting with top financial advisors, $BX's Jon Gray explains why the math doesn’t add up on some of the predictions around private credit. Watch:

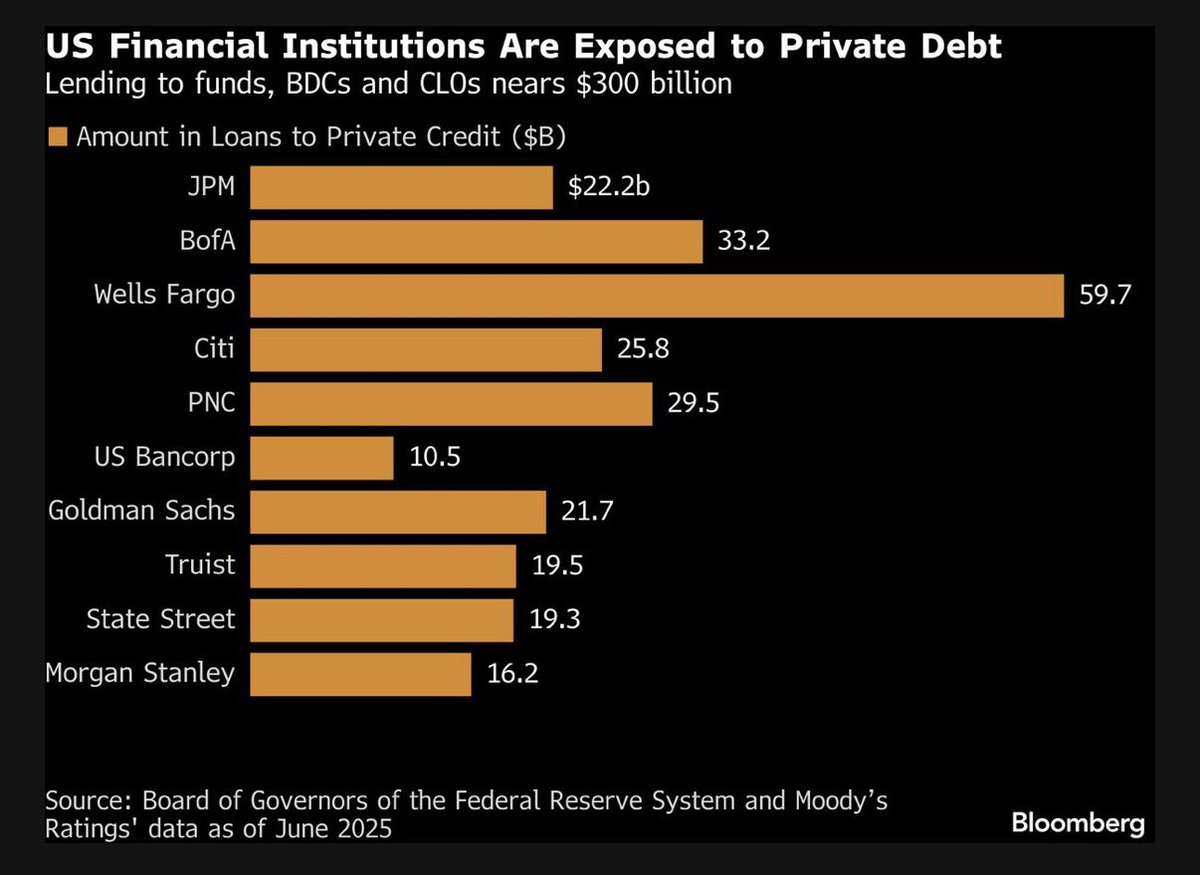

Following JPMorgan’s announcement earlier this week (please see earlier post), here’s Bloomberg on “back leverage:” “Private credit funds, already on the defensive amid an unprecedented investor exodus and a number of defaulting borrowers, are now bracing for a battle with their go-to lenders: major banks.” #economy #markets #privatecredit #banks