@petsbysimon@TheWyteRabbit1 The Cl you're referring to in your example is Chloride not Chlorine. The difference is gargantuan, even though the spelling is off by one letter...

@Sheep_Of_Trades Looking at the Casino deposit so far, measured indicated and inferred metals which include gold, copper, molybdenum and silver, at spot prices it's approx. 215 billion dollars worth of metals in situ now. 47 yr. mine after phase 2 with more life after that.

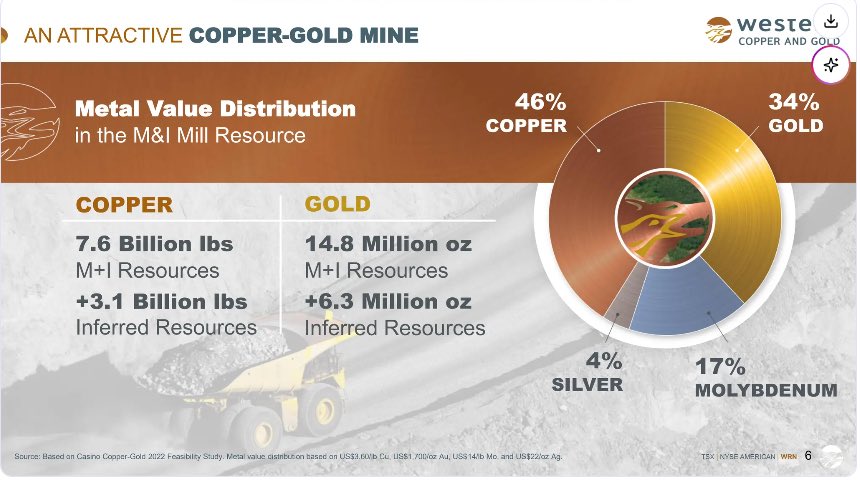

According to the latest $WRN January slides on their website, they are sitting on about $4B in copper and $97B in gold.

Of course there are more things to consider, but if you oversimplify, for this company to be valued at 680M with over 100B in metals, seems like a no-brainer play if you can hold longer term.

#COPPER#SILVER#GOLD

$wrn HC Wainwright raises Western's #WRN target to $5.75 from $4.25 maintaining their buy rating, citing increased optimism for the Casino Project. Spot prices for gold, copper, moly & silver put Casino's NAV over $7.2 bil U.S., a 40% IRR and a blistering 1.5 yr. Capex payback.

@westernCuandAu Very proud of the company for stepping up when the government stepped back... Helping to feed children is no small matter... Well done!

$WRN | Western Copper and Gold is proud to partner with Little Salmon Carmacks First Nation to support school and daycare meal programs in Carmacks.

“We’re grateful to work alongside Little Salmon Carmacks First Nation in supporting these programs for the children and families of Carmacks. We see this as part of what it means to operate responsibly in the Yukon,” said Sandeep Singh, President & CEO.

➡️ Read the full release: bit.ly/48AsBUX#Yukon#Community#Mining

TSX: $WRN.TO | NYSE American: $WRN

@westernCuandAu One overlooked fact about Casino is based on spot prices for copper, gold, molybdenum and silver, you're looking at close to 180 billion dollars worth of metals in situ right now. Hard to imagine what that figure might be in Western's entire land package looking decades ahead.

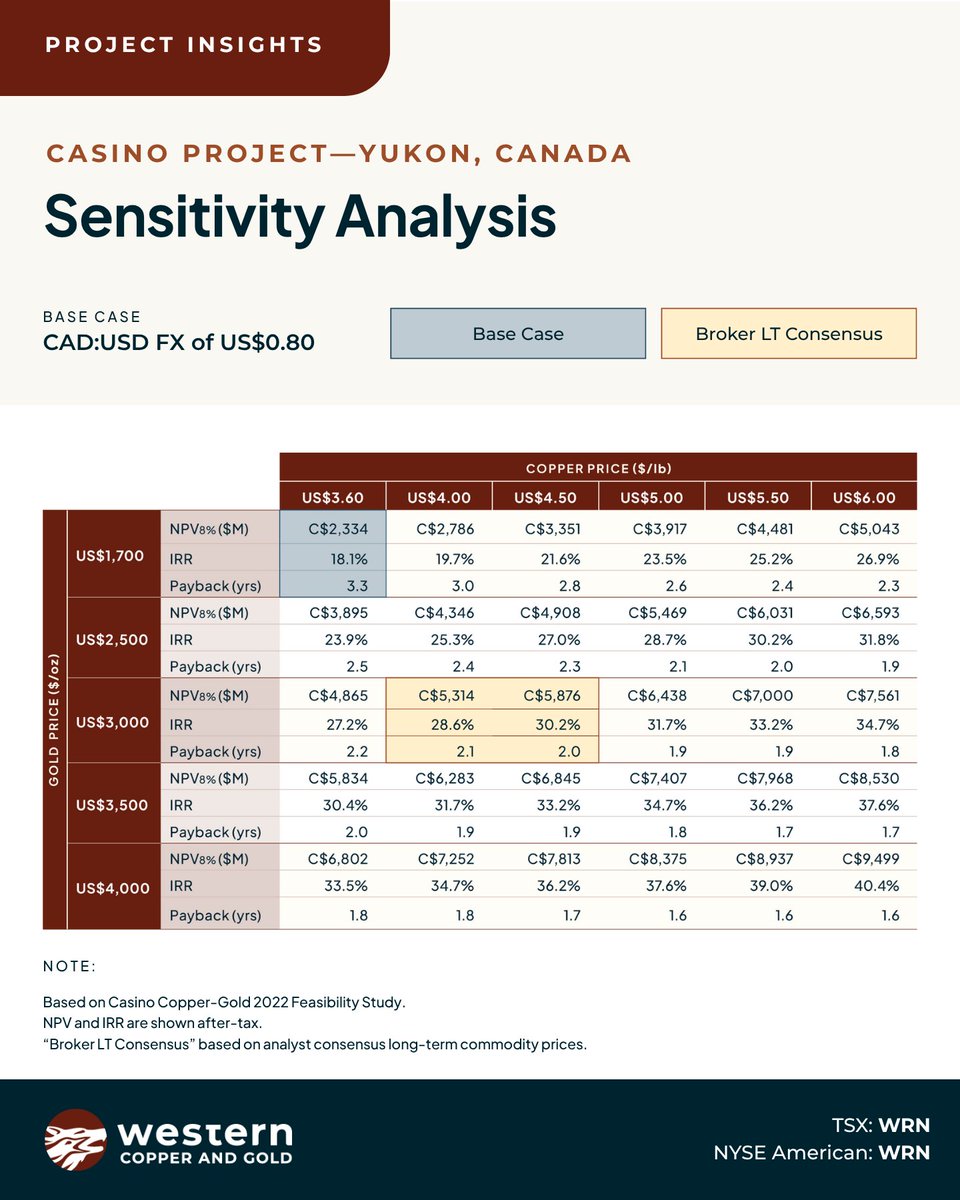

Long-term commodity price assumptions have shifted meaningfully in recent years.

What long-term copper and gold prices do you view as reasonable when evaluating projects – and why?

Share your perspective below. 👇

#Copper#Gold#Mining

TSX: $WRN.TO | NYSE American: $WRN

$WRN | The Casino Project offers substantial leverage to copper and gold prices – with meaningful option value tied to its 27-year mine life.

As Casino advances and de-risks, this leverage provides strong potential for further re-rating.

View the sensitivity matrix below.

#Yukon#Canada#Mining#Copper#Gold#CriticalMinerals

TSX: $WRN.TO | NYSE American: $WRN

$WRN | The Casino Project's high-grade Core Zone is a key value driver – delivering strong early cash flow and rapid payback.

In Years 1-4, higher milled grades (0.66% CuEq) and an ultra-low strip ratio (0.26:1) drive exceptional early economics.

With a 27-year mine life based on roughly one-third of its current resource endowment, Casino offers a best-in-class mine life-to-payback ratio – and significant long-term optionality.

#Yukon#Mining#Copper#Gold#CriticalMinerals

TSX: $WRN.TO | NYSE American $WRN

$WRN | The Casino Project ranks as Canada's top critical minerals project by GDP impact.

Over its 27-year mine life, Casino is expected to contribute C$44 billion to Canada's GDP – including C$37 billion in the Yukon – along with C$12 billion in wages and hundreds of direct jobs.

Casino is positioned to strengthen the North's economy and Canada's global presence for decades to come.

📊Read the report: casinomining.com/wp-content/upl…#Canada#Yukon#Mining#Copper#Gold#CriticalMinerals

TSX: $WRN.TO | NYSE American: $WRN