narkheel.eth

1.6K posts

One of the greatest videos ever.👏👏

What a household.❤️

English

looking to hire a talented pixel artist for some character sprites, little side project 🙏

English

After 4 incredible years, today was my last day at Yuga Labs.

5 years ago I was a first-semester med school student who had just sold his car and put every last dollar into a Mutant Ape. Months later I got the call to join Yuga, and I never looked back.

I went from a community member to driving social comms for @BoredApeYC, @OthersideMeta, @yugalabs, @MeebitsNFTs, @FvckingMeta, @Toptrader_xyz, and more. I wrote copy, produced assets, resolved what felt like thousands of support tickets, built sentiment decks, ran QA and bug triage across numerous activations. I dove into product research and management, working on PRDs, GTM plans, murderboards, Figma designs, Jira taskboards, the whole nine. Dug through various dApps, L1s/L2s, AI use-cases, differentiating factors, narratives, functions, incentives, among many other metrics.

But what I'll carry with me most is the community. The Yuga community gave me a home in this industry, and I'm so grateful for every interaction, every event, every late night pushing to get things right for you all.

To the Yuga team, thank you for taking a chance on a degen who bet everything on a jpeg. That bet changed my life.

Web3 is my home and I'm not going far. If you're building something and need someone who lives and breathes social, community, product, and research — come say hi. My DMs are open. 🫡

English

Bit Paine ⚡️@BitPaine

Two interesting theories on the parabolic sell off yesterday: @TheOtherParker_ theorizes that HK-based hedge funds, likely non-crypto natives, blew up on massively leveraged $IBIT options trades. Key evidence: record $10.7B IBIT volume (2x prior high), $900M options premiums, and BTC/SOL lockstep drop with low CeFi liquidations. These funds held 100% in $IBIT for margin isolation, per 13F filings. Tied to JPY carry unwind raising funding costs, silver’s 20% crash (2nd largest ever), and a summer short-vol squeeze compressing BTC vol to record lows - until Oct 10’s spike blew holes in balances, spiraling into desperation trades and full liquidation. In-kind ETF creations since July ’25 enabled OG Bitcoiners to shift stacks tax-free for covered calls, amplifying vol suppression and eventual unwind. @TheShortBear attributes it to a leverage-driven unwind from the yen carry trade, hitting correlated risk assets like $BTC and software stocks ($IGV). No single blow-up, but systemic positioning stress: funding tightens, vol spikes, forcing sales across yield-seeking channels (crypto, software, private credit). Unwind started ~quarter ago, aligning with risk momentum loss; plays out in waves over quarters with grace periods. Binance’s heavy Asian-hour selling suggests regional funds/traders dumping during US liquidity. Long crypto positions now liquidated at 20:1+ skew, resetting extremes. Always remember: financialization of BTC via ETFs/options introduces systemic macro and derivatives risks -like carry trades, vol squeezes, and cross-asset contagion - wholly unrelated to BTC’s fundamentals. This dovetails with my theory that much “OG selling” was likely rotation into $IBIT for access to margin leverage and its ultra-liquid options market, fueling the powder keg.

QME

NEUES VIDEO:

Der Bitcoin Preis ist seit seinem Allzeithoch von über 126.000 US Dollar um mehr als 50 Prozent gefallen. In Medien und sozialen Netzwerken werden aktuell zahlreiche Gründe für den Bitcoin Crash genannt, doch nur sehr wenige davon halten einer sachlichen Analyse stand.

Von angeblichen Verbindungen zu Jeffrey Epstein und Spekulationen rund um Satoshi Nakamoto, über den bekannten Tether FUD, bis hin zum vermeintlichen Liquidationsrisiko von Michael Saylors Strategy ist nahezu jedes Narrativ vertreten, das den starken Preisrückgang erklären soll.

In diesem Video analysiere ich die fünf meistgenannten Gründe für den aktuellen Bitcoin Crash, Dip oder Bärenmarkt und erkläre detailliert, welche dieser Argumente wirklich relevant sind und welche schlicht keinen Sinn ergeben. Ziel ist es, Fakten von Emotionen zu trennen und eine nüchterne Einordnung der aktuellen Marktsituation zu liefern.

youtube.com/watch?v=1UotlT…

YouTube

Deutsch

Deutschland hat diesen talentierten Künstler geopfert für irgendwelche Internettrolle und Dauerstudenten wie Abk

Schämt euch

Deutsch

GM and HMM! 🧪🧪

Anyone buy any Mutants at these prices?

Picked up some Apecoin on Solana this morning, but might have to scoop a Mutant 👀. lfg

English

GIF

English

gm.

still here. still doing art. just heads down working behind the scenes. putting in the work! gotta make sure i can do what i said i was gonna do. i’ll update more when i get closer. until then.

one of my latest. bet ya didn’t even notice the little shadows under the apes

English

narkheel.eth retweetledi

@CryptoGarga @BoredApeYC smash the gas greg LFG EVERYBODY GET INNNNNNN @Lucky1seth @Codeiaks @narkheel @gifr_eth @OGWL @GBsTVee @Elektro4242

GIF

English

we're back baby

it's a great time to build crypto in the USA

Yuga Labs@yugalabs

After 3+ years, the SEC has officially closed its investigation into Yuga Labs. This is a huge win for NFTs and all creators pushing our ecosystem forward. NFTs are not securities.

English

@Ashcryptoreal @mittser_mayc good try. Probably hedged position.

English

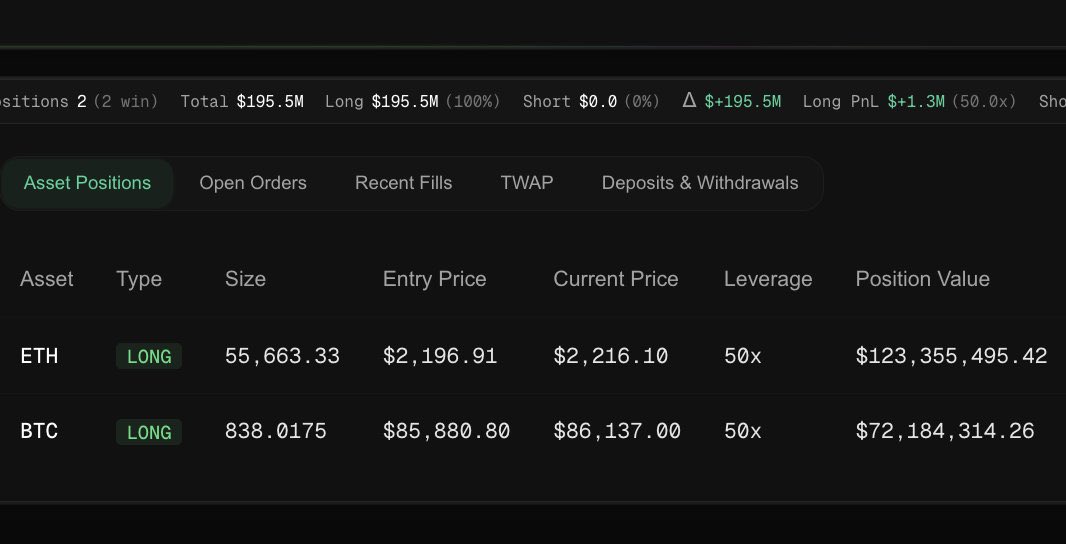

TODAY: SOMEONE OPENED A $123M

LONG ON $ETH AND $72M LONG ON

$BTC WITH 50X LEVERAGE.

HE KNOWS SOMETHING….

English

narkheel.eth retweetledi

BREAKING 🚨: A rare planetary alignment is happening tonight (Feb 28)

Saturn, Mercury, Neptune, Venus, Uranus, Jupiter, and Mars will line up after sunset

Visible anywhere with clear skies ✨

English

PYTHON is difficult to learn, but not anymore!

Introducing "The Ultimate Python ebook "PDF.

You will get:

• 74+ pages cheatsheet

• Save 100+ hours on research

And for 48 hrs, it's 100% FREE!

To get it, just:

1. Like & RT

2. Reply "DM"

3. Follow @CjRandhawaX [MUST]

English

gm and hmm 🦍’s and anon’s,

are you into art?

are you into pokemon?

are you into collecting?

98/151 minted

unrevealed. will reveal shortly after mint out.

we’re so close yet so far! almost!! thank you everyone so far!!! 🙏🏼🧡

more info here: 👇🏼

artlicky-on-apechain-series-2.nfts2.me

English

@100trillionUSD would we be there if they money tied up in memecoins would actually be in btc?

English