Nemesis

98 posts

Nemesis retweetledi

Nemesis retweetledi

Nemesis retweetledi

It's official – the first neutral-atom quantum company is publicly trading under $INFQ.

We couldn't be more thankful for everyone who shared this moment with us, and especially the partners, customers, and team members who made it possible.

NYSE 🏛@NYSE

From world‑class quantum computers to cutting‑edge sensors, @infleqtion aims to transform neutral‑atom science into solutions that elevate human potential. ⚛️ $INFQ

English

Nemesis retweetledi

I spent 100 hours over the past week researching, writing and editing the piece we just put out.

It’s a scenario, not a prediction like most of our work. But it was rigorously constructed, dismissing it outright requires the kind of intellectual laziness that tends to get expensive.

And we’ve released it for free. Hopefully you enjoy it.

citriniresearch.com/p/2028gic

English

Its wild to me as to how certain people choose to be negative.

It makes no sense. It costs nothing to kind, it costs nothing to be negative.

So lets go and be miserable instead of happy or thankful.

Just wild.

This is aimed at one person in particular.

English

Nemesis retweetledi

Nemesis retweetledi

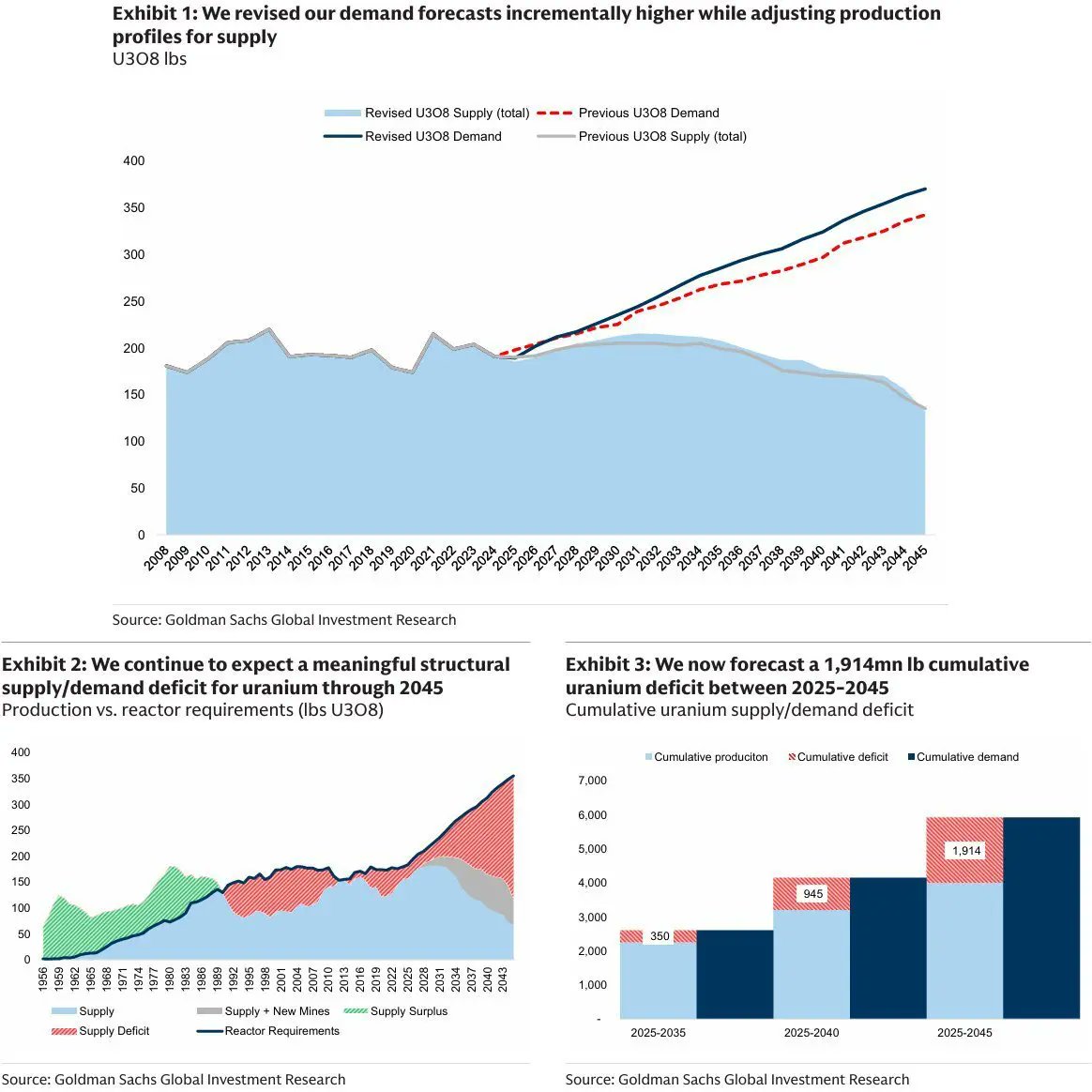

Goldman Sachs Initiates $UUUU with Buy Rating, PT $30

Analyst comments: "UUUU owns and operates the highest-grade uranium deposit in the United States, as well as the White Mesa Mill, which is a key competitive advantage as it is the only processing facility in the United States able to process both uranium and rare earth elements. Additionally, the company maintains a portfolio of three heavy mineral sands assets expected to come online over the next five years, which will supply the key feedstock, monazite, to support expansion into production of key light and heavy rare earths (NdPr, Dy, Tb). We believe this positions UUUU uniquely versus peers given strong demand and pricing trends for heavy rare earths and the likelihood of increasing policy support for securing domestic supply and production capabilities for these critical minerals."

Analyst: Brian Lee

English

Nemesis retweetledi

"Satan has three steps to steal our peace:-

Regrets about the past;

Fear for the future;

Ingratitude for the present."

- St Anthony the Great

English

Nemesis retweetledi

Finally took a deeper look at $MRVL.

My first reaction: What are the markets and analysts/news smoking?

Revenue derived from Maia ramp is literally double $MRVL's FY 2025 revenue.

If we look at the numbers, it's staggering:

Marvell is modeled to take in $10-$12B in revenue (Fubon) in Microsoft Maia ramp in 2027. Alone.

To put that in perspective, Marvell's FY 2025 revenue was $5.77B.

No matter how I look at it, Marvell looks like a strong Broadcom competitor (after Celestial acqusition) and a terrific long.

But... The Information / Benchmark released news that:

- Microsoft is negotiating with Broadcom to displace Marvell in future generations.

- Amazon Trainium 3 and 4 designs went to Taiwanese competitor Alchip Technologies.

causing a massive selloff.

After looking into it more, how is this even possible?

"Marvell Technology declines after Benchmark Equity Research downgrades the stock, citing a loss of Amazon’s AI chip business."

"Benchmark believes Marvell lost Amazon’s Trainium 3 and 4 designs to Alchip, despite Marvell’s recent forecast of strong data-center growth."

- Trainium 3 production are locked to Marvell's design. You can't "swap" to Alchip without designing an entirely new chip from scratch. If you want to share scope, sure but the wording is absolutely atrocious.

$MRVL already secured Trainium 3 orders from $AMZN throughout 2026, why in the world would Amazon cancel them all and then go with a new vendor?

There can be different scope, additional design services, etc. but the framing from all the news sounds like $MRVL is being displaced.

Benchmark itself later walked it back materially after causing damage (via more "industry discussions") and said Marvell did not lose Trainium 3/4 outright, but that Amazon added Alchip for additional design support while Marvell retains a position.

But the damage has already been done to stock price.

As for The Information report on $MSFT Maia loss to Broadcom this is sensational journalism.

JP Morgan later literally came out and basically said it's all false, "there has been no ASIC program share loss".

On the Microsoft deal, markets completely missed the nuance between "immediate displacement" and "future generation" discussions.

The physics of this make an immediate swap impossible from Maia to Broadcom without incredible multiple-year delays.

To replace Marvell with Broadcom for the Maia 300 now would require scrapping the entire 2nm mask set, redesigning the I/O ring, and restarting a 3-year validation cycle. Marvell’s specific SerDes Is is also embedded in the chip’s I/O ring (retimers and switches comms). If Microsoft targets a 2027 ramp for Maia 300, the chip must be in validation phase by mid-to-late 2026. This implies the physical design is already frozen or nearing freeze today.

A new ASIC design with $AVGO today (Dec 2025) would face this minimum timeline:

- Architecture & RTL (12 months): Logic definition and IP selection.

- Physical Design to tape ot (9-12 months)

- Mask prod & Fab (3-5 months): TSMC 2nm cycle.

- Post-Silicon validation (6-9 months)

Total Time: ~30–38 months.

Even if this is sped up by many months, these "Discussions with $AVGO " not be ready for volume deployment until 2028 at the very earliest. To hit the 2027 ramp timelines, Microsoft must ship the Marvell design.

Then there's Microsoft’s rack infrastructure uses Marvell’s "Alaska" retimers and DSPs in the cables.

Microsoft would have to:

- Re-qualify the signal integrity of every cable and backplane in the rack.

- Rip out Marvell retimers from the motherboard and replace them with Broadcom versions

As well as change their custom liquid-cooling rack "sidekick", which was specified toward specific distribution of the $MRVL Maia chip’s floorplan. A $AVGO chip would have a completely different physical floorplan and thermal density and they'd need to regineer the rack.

So market are completely trolling if when they price in immediate displacement risk and trade on TMZ-style discussion gossip rumors that Microsoft wanted to explore options.

$MRVL CEO even went out and said they have "purchase orders in hand" for the entirety of the next year's forecast. 2026 forecasts are probably light because $AMZN and $MSFT both faced delays on their ramp.

But if you look at longer term Q4 2026 into 2027, we just from their orders and Maia 300 alone: even just estimating $7.72 EPS from ~$20.0B revenue, 30x P/E (they've traded 35-40 before), would be $231.60/share from $85 if you want to wait 2 years.

So TLDR: The whole “replacement” theory is extremely completely misinterpreted and is just noise. Normally, I wouldn't write a whole post on it, but seeing The Information and other news pop up again, and again, spreading misinformation through sensational wording is just crazy.

There's a physical impossibility of a mid-cycle swap and market misunderstanding of displacement. So the recent sell-off looks like a solid buying opportunity.

As for future discussions, of course any company would want vendor diversification. $MRVL can go do the same with $META MTAI future generations too if Meta wants to multi-source away from Broadcom.

If you model just by single project Maia 300 alone and ignore media noise, $MRVL looks incredibly promising.

English

Nemesis retweetledi

🚨@Energy_Fuels to acquire Australian Strategic Materials to create new "mine-to-metal & alloy" rare earth champion 🚨

Read the full details in our most recent press release: investors.energyfuels.com/2026-01-20-Ene…

$UUUU $EFR #EnergyFuels #rareearths

English

Nemesis retweetledi

Amazon is a company that is set up well for 2026. Their revenue mix is improving from retail sales to services. AWS is reaccelerating, the ads business is set up well to continue growing, and if Amazon captures more grocery market share it makes them structurally stronger.

I hold a lot of Amazon going into 2026.

Joseph Carlson@joecarlsonshow

What's your single biggest bet for 2026?

English