Green Energy Investor@GreenOriginInv

🔋🔋LITHIUM BULL 🐂

Well on a down day I decided to add European Metal Holdings $EMH - Looks like it has a much better chance in this cycle.

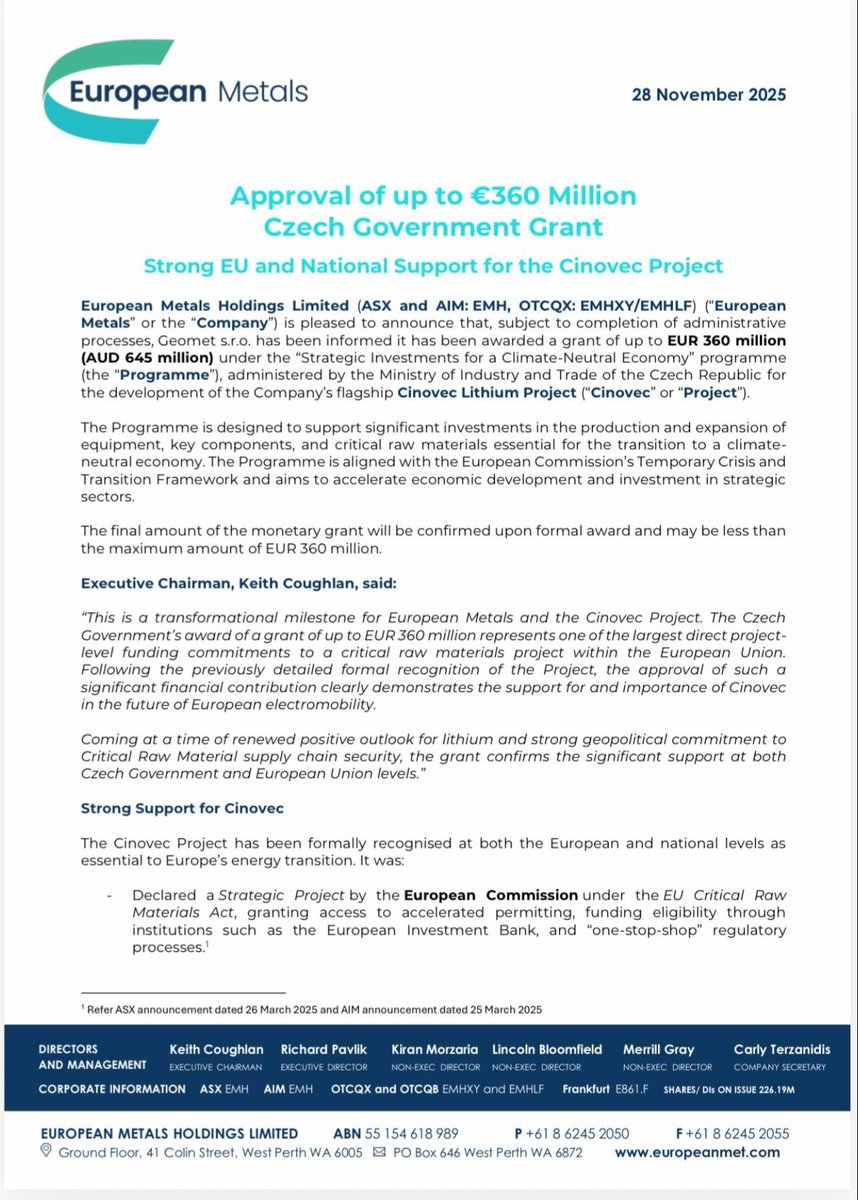

EMH holds a 49% stake through its subsidiary Geomet s.r.o., with Czech utility CEZ a.s. owning the remaining 51%. The project targets battery-grade lithium hydroxide (LiOH) production, aligning with EU critical minerals goals under the Critical Raw Materials Act.

The Definitive Feasibility Study (DFS) is due in December 2025, marking a key catalyst. Until then, economics are based on the 2022 Pre-Feasibility Study (PFS) update, which remains the most detailed public benchmark. Lithium market dynamics have improved since (prices up ~23% month-over-month as of Nov 20, 2025), but I'll flag sensitivities.

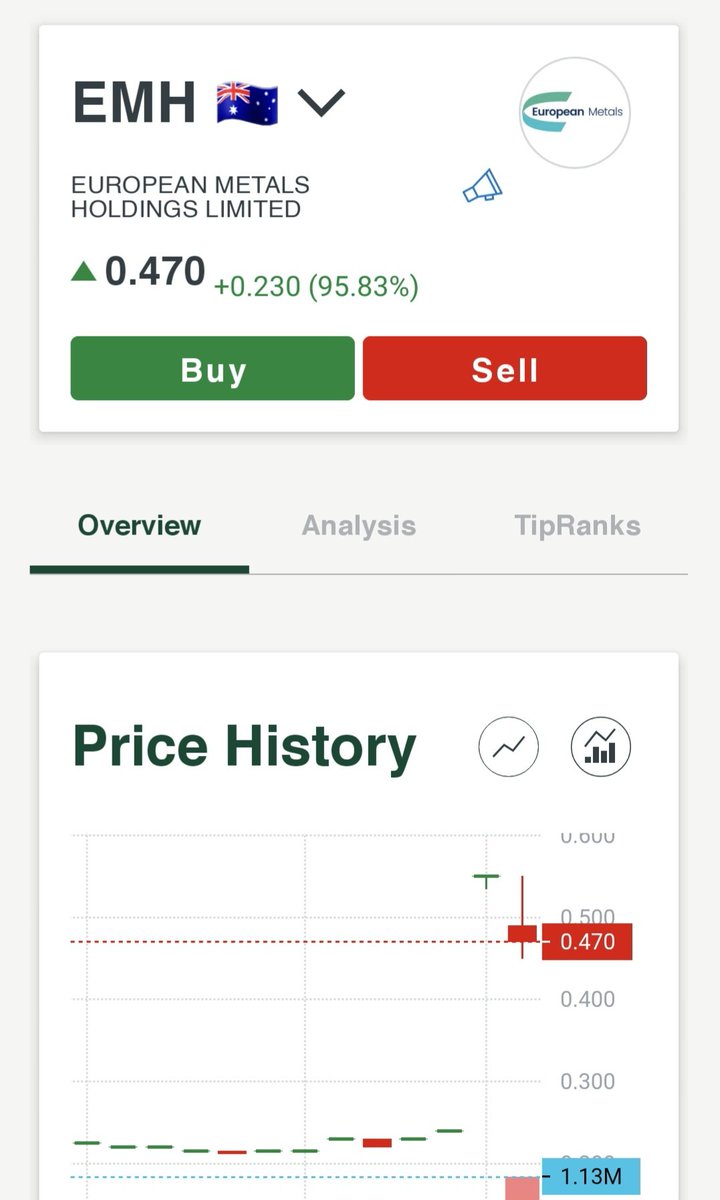

- Current Valuation Metrics: As of Nov 19, 2025, EMH trades at A$0.21/share on ASX (market cap: A$46.2M) and 11p/share on AIM (market cap: ~£24.9M / A$50M equivalent). Shares outstanding: ~226.6M. Price-to-Book ratio: 1.5x (vs. Australian metals/mining industry avg. 2.3x), suggesting relative cheapness.

- Analyst Targets: Consensus is "Hold" with an A$0.50 target (~138% upside from current). Longer-term forecasts (e.g., 2025 avg. price A$0.21, high A$0.39) imply modest near-term growth but explosive potential post-DFS.

- NPV-Implied Value: The PFS attributes a post-tax NPV₈ of US$1.94B to the full project (36.3% IRR). EMH's 49% share: ~US$950M (A$1.43B at current FX). At current market cap (A$46M), this implies a ~31x multiple to attributable NPV – a classic "junior miner discount" for pre-production assets. Even applying a conservative 50% "risk haircut" (as in Liberum's 2024 note) yields ~A$715M fair value, or A$3.15/share (15x current price).

Risks include lithium price volatility (current spot: ~US$10,200/t LiOH CIF, vs. PFS assumption of US$17,000/t – a ~40% haircut that could reduce NPV to ~US$1.1B). However, Cinovec's low-cost profile and EU strategic status provide a floor. With DFS imminent and funding secured, this is a high-conviction "buy" for lithium bulls targeting European supply chain localization.