Sabitlenmiş Tweet

youtube.com/watch?v=3kIClX…

This was a lot of fun, privilege's to be on Bill's curated forum. Pleased to have found his site and devouring his other material. @MiningStockEdu

YouTube

English

Nugt

1.6K posts

@nugget_effect

Rocks and stocks. Also fishing/fatherhood/books/travel

The @Apple link to episode 231 with Tom Benson podcasts.apple.com/us/podcast/the…

$700 million coming for #Gold equities by one of best in the boutique funds management business, L1 Capital The two founders tipping in $100m of own money is good indicator of their #gold sentiment Interesting to see which stocks they allocate to Src afr.com/street-talk/l1…

Metals: The projected demand growth of copper, steel, lithium, and aluminum over the next 10 years is shown in the chart below, according to Australian mining giant Rio Tinto. ⛏️👇 As expected, lithium is far ahead, but it's currently a much smaller market, of course. $RIO

🔋 Lithium is back in focus. Prices are up more than 125% over the past year as demand expands beyond EVs and governments increasingly treat the metal as a strategic resource. With supply disruptions, evolving policy tools and rapid growth in grid‑scale energy storage, lithium is being repriced, not just as a commodity, but as critical infrastructure. ⚡️🏗️Read more from Jacob White, Director, ETF Product Management at Sprott. sprott.com/insights/lithi…

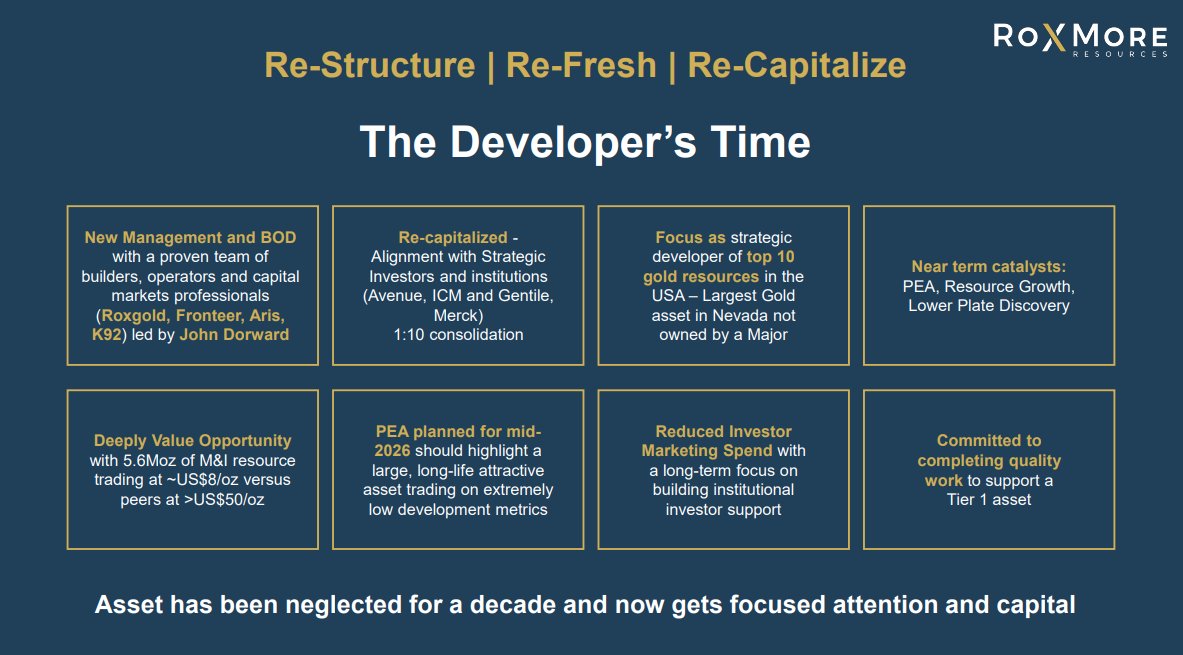

THE NEVADA MEGA-MERGER: SSR MINING just got 1,5 Billion in cash to possible buy x i-80 GOLD x ROXMORE Is $SSRM about to create a Nevada Titan by swallowing $IAUX and Roxmore? Let’s dive into the "Hub-and-Spoke" play of the century. 🧵👇 1️⃣ The War Chest 💰 SSR Mining just signed a binding $1.5 Billion all-cash deal to exit Çöpler (Turkey). While the close is set for Q3 2026, the market knows SSRM is now "Americas-focused." They don't need to wait for the final wire; with that contract, their credit lines are wide open for accretive growth NOW. 2️⃣ The Strategic Jewel: Lone Tree 💎 Why buy $IAUX (i-80 Gold)? One word: Infrastructure. i-80 owns the Lone Tree Autoclave. In a world of rising costs, you don't build new autoclaves; you buy them. It’s the only way to unlock high-grade sulfide ores. For SSRM’s Marigold mine, this is the missing puzzle piece to process their own deep sulfides. 3️⃣ The Volume: Roxmore’s Converse 🏗️ Roxmore $RM.ca sits on the Converse Project—5.5M+ oz of gold. At $5,190 gold, it’s a cash-printing machine. It’s located right next to SSRM’s Marigold. The Problem: Roxmore has no mill. The Solution: SSRM buys Roxmore + i-80. Roxmore ore feeds the i-80 autoclave. Synergy level: 100%. 4️⃣ Financials📊 SSR Mining: ~$6.76B MCap i-80 Gold: ~$1.59B MCap Roxmore: ~$160M USD MCap 5️⃣ EXCLUSIVE: EBITDA Forecast for "NewCo" (i-80 + RM Only) 📈 What happens to the combined i-80/Roxmore assets under SSRM's wing? (Excludes existing SSRM assets): 2026: -$45M | Heavy Capex for Lone Tree refurb. 2027: +$110M | First oxide production ramp-up. 2028: +$680M | INFLECTION POINT. Lone Tree Autoclave goes online. 🚀 2029: +$1.15B | Full scale. Converse $RM.ca ore hits the hub. 2030: +$1.32B | Optimization. Tier-1 production status achieved. 6️⃣ Why wait? ⏳ SSR Mining shouldn't wait for the Turkey cash to hit the bank. The longer they wait, the more expensive $IAUX becomes as it derisks Lone Tree. By mid-2026, the "Nevada Discount" might be gone. The Bottom Line: By combining Marigold (SSRM) + Lone Tree (i-80) + Converse (Roxmore), SSR Mining becomes the undisputed #3 producer in the USA, holding the keys to the most important processing hub in Nevada. Are we looking at the birth of the "Nevada Gold Hub"? 🏔️⛏️ Disclaimer: Not financial advice. Mining is high risk. Always do your own DD. #Gold #Mining #Stocks #SSRM #IAUX #Roxmore #Nevada #Investing #GoldPrice

THE NEVADA MEGA-MERGER: SSR MINING just got 1,5 Billion in cash to possible buy x i-80 GOLD x ROXMORE Is $SSRM about to create a Nevada Titan by swallowing $IAUX and Roxmore? Let’s dive into the "Hub-and-Spoke" play of the century. 🧵👇 1️⃣ The War Chest 💰 SSR Mining just signed a binding $1.5 Billion all-cash deal to exit Çöpler (Turkey). While the close is set for Q3 2026, the market knows SSRM is now "Americas-focused." They don't need to wait for the final wire; with that contract, their credit lines are wide open for accretive growth NOW. 2️⃣ The Strategic Jewel: Lone Tree 💎 Why buy $IAUX (i-80 Gold)? One word: Infrastructure. i-80 owns the Lone Tree Autoclave. In a world of rising costs, you don't build new autoclaves; you buy them. It’s the only way to unlock high-grade sulfide ores. For SSRM’s Marigold mine, this is the missing puzzle piece to process their own deep sulfides. 3️⃣ The Volume: Roxmore’s Converse 🏗️ Roxmore $RM.ca sits on the Converse Project—5.5M+ oz of gold. At $5,190 gold, it’s a cash-printing machine. It’s located right next to SSRM’s Marigold. The Problem: Roxmore has no mill. The Solution: SSRM buys Roxmore + i-80. Roxmore ore feeds the i-80 autoclave. Synergy level: 100%. 4️⃣ Financials📊 SSR Mining: ~$6.76B MCap i-80 Gold: ~$1.59B MCap Roxmore: ~$160M USD MCap 5️⃣ EXCLUSIVE: EBITDA Forecast for "NewCo" (i-80 + RM Only) 📈 What happens to the combined i-80/Roxmore assets under SSRM's wing? (Excludes existing SSRM assets): 2026: -$45M | Heavy Capex for Lone Tree refurb. 2027: +$110M | First oxide production ramp-up. 2028: +$680M | INFLECTION POINT. Lone Tree Autoclave goes online. 🚀 2029: +$1.15B | Full scale. Converse $RM.ca ore hits the hub. 2030: +$1.32B | Optimization. Tier-1 production status achieved. 6️⃣ Why wait? ⏳ SSR Mining shouldn't wait for the Turkey cash to hit the bank. The longer they wait, the more expensive $IAUX becomes as it derisks Lone Tree. By mid-2026, the "Nevada Discount" might be gone. The Bottom Line: By combining Marigold (SSRM) + Lone Tree (i-80) + Converse (Roxmore), SSR Mining becomes the undisputed #3 producer in the USA, holding the keys to the most important processing hub in Nevada. Are we looking at the birth of the "Nevada Gold Hub"? 🏔️⛏️ Disclaimer: Not financial advice. Mining is high risk. Always do your own DD. #Gold #Mining #Stocks #SSRM #IAUX #Roxmore #Nevada #Investing #GoldPrice