@LeoMargolis_ importantly citsec pays to be retails counterparty though? i'm sure kalshi would be thinking about something similar, targeting people who bet through coinbase, etc.

English

ziggy

9 posts

The math that made Wall Street billions pricing options just got ported to prediction markets This paper builds the first Black-Scholes equivalent for platforms like Polymarket Treating belief volatility as a quotable risk factor, with proper tools for hedging jump risk around elections and macro events. The paper is dense but worth it:

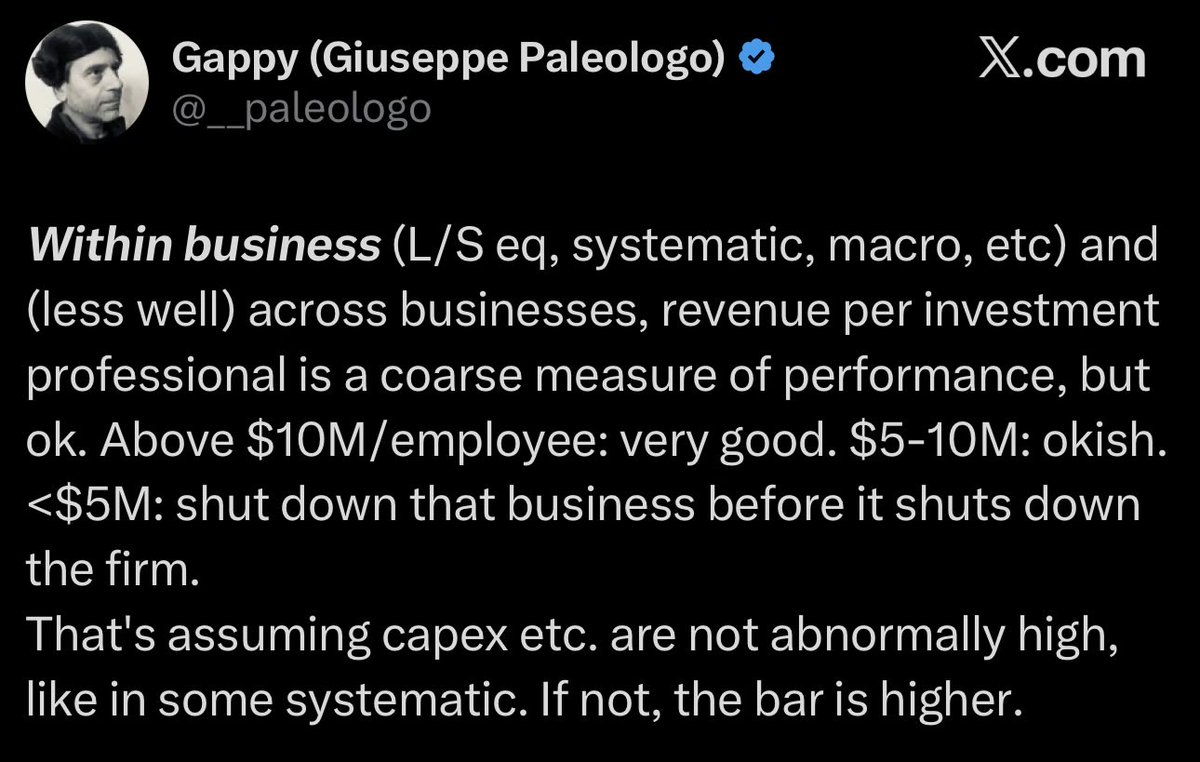

Coming from a GP at YC, I would have expected somewhat less laughable ignorance about what make the top quant firms profitable. Particularly Jane Street.