One foot hurdle@one_foothurdle

(1/2) This is an update of an earlier post where I made some miscalculations.

——

Although I have not read the full write-up because I am not a subscriber, I have followed $WW for some time and own part of the restructured debt. I want to offer a different perspective on the company’s clinical pivot.

The key issue, in my view, is not whether the clinical business is growing. The key issue is whether that growth is economic.

WeightWatchers is spending heavily on marketing, but what is the return?

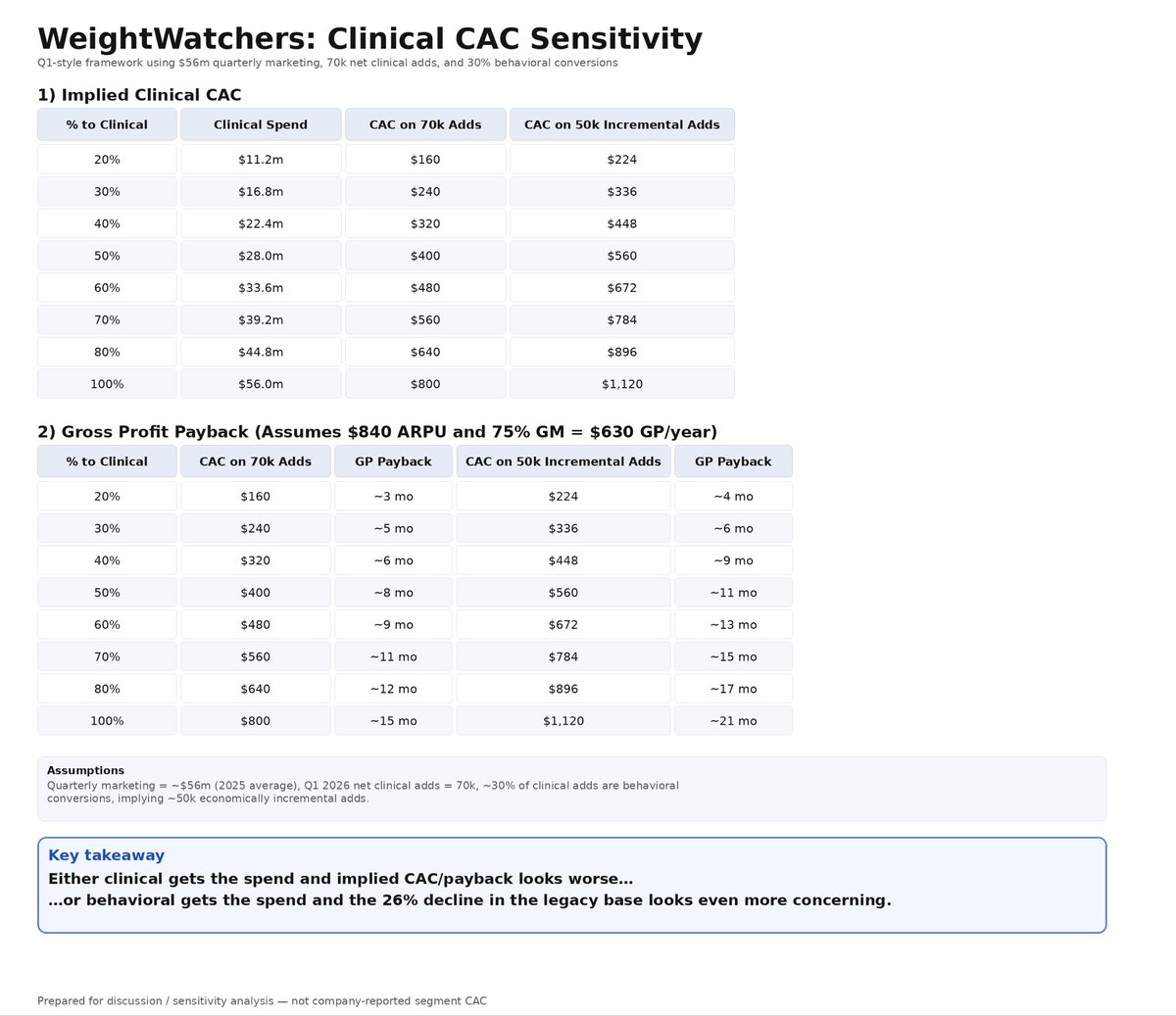

In 2025, WeightWatchers spent approximately $227 million on marketing, or roughly $56–57 million per quarter on average. While marketing is seasonally heavier in Q1, using the average quarterly figure is actually generous to management because Q1 spend is likely higher.

The question is simple:

What is WeightWatchers actually getting for this level of spend?

Behavioral business: marketing is not stopping the decline

For the legacy behavioral segment, the answer appears to be: very little.

Behavioral subscribers declined approximately 26% year-over-year. Management may argue that marketing prevented an even steeper decline, but that is speculative. What is observable is that WeightWatchers is spending enormous amounts on marketing while the legacy business continues to contract sharply.

That matters because the behavioral business remains the larger installed base and historically the higher-quality source of cash flow.

Clinical growth is real, but the economics look questionable

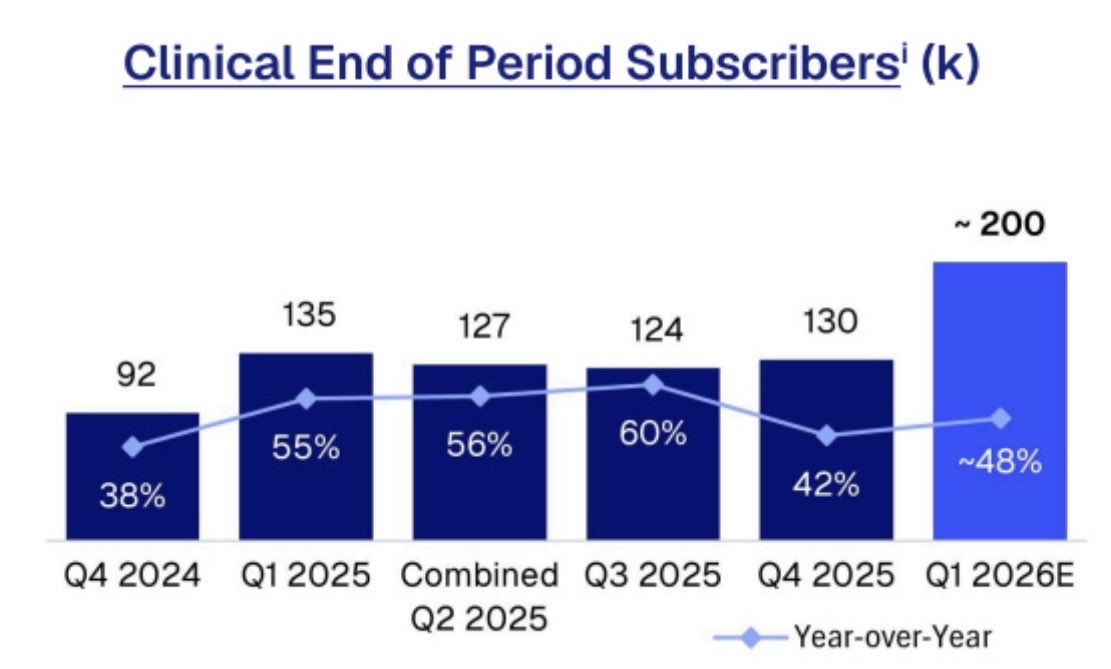

In Q1 2026, WeightWatchers added approximately 70,000 net clinical subscribers.

If we compare that to the company’s average quarterly marketing spend of roughly $56 million, WeightWatchers is effectively spending about:

~$800 of quarterly marketing dollars for each net clinical subscriber added

Again, this likely understates the true burden, because Q1 marketing spend is typically above the quarterly average.

Now consider that management has also disclosed that roughly 30% of clinical subscribers are conversions from behavioral members.

That distinction matters. A behavioral-to-clinical conversion is not the same as a truly incremental new customer. It may increase revenue per user, but it does not represent a fully new member added to the ecosystem.

Adjusting for that, the truly incremental clinical adds are closer to 50,000, which implies:

~$1,100 of quarterly marketing spend for each economically incremental clinical subscriber

To be clear, I am not claiming this is WeightWatchers’ reported “clinical CAC” in the narrow performance-marketing sense. It is something more important:

It is the effective economic marketing burden required to generate net clinical growth while the rest of the business is shrinking.

And for investors, that may be the more relevant number.

The payback period appears unattractive

Clinical ARPU is roughly $840 annually.

Using management’s approximate 75% gross margin, that translates to around:

~$630 of annual gross profit per clinical member

If WeightWatchers is effectively spending ~$1,100 to generate one economically incremental clinical subscriber, then the gross-profit payback period is:

~21 months ($1,100 / $630)

And that is a best-case framing, because this uses gross profit, not true contribution profit.

In reality, the clinical business likely carries additional costs such as:

•physician and care delivery infrastructure

•support and service costs

•retention marketing

•payment and processing costs

•other variable operating expenses tied to the clinical platform

That means the true contribution payback period is likely longer than 21 months.

So the real issue is not whether clinical is growing. It is whether WeightWatchers is spending uneconomic amounts of capital to acquire growth that may take far too long to pay back.