Nitin Verma@itsnitinverma

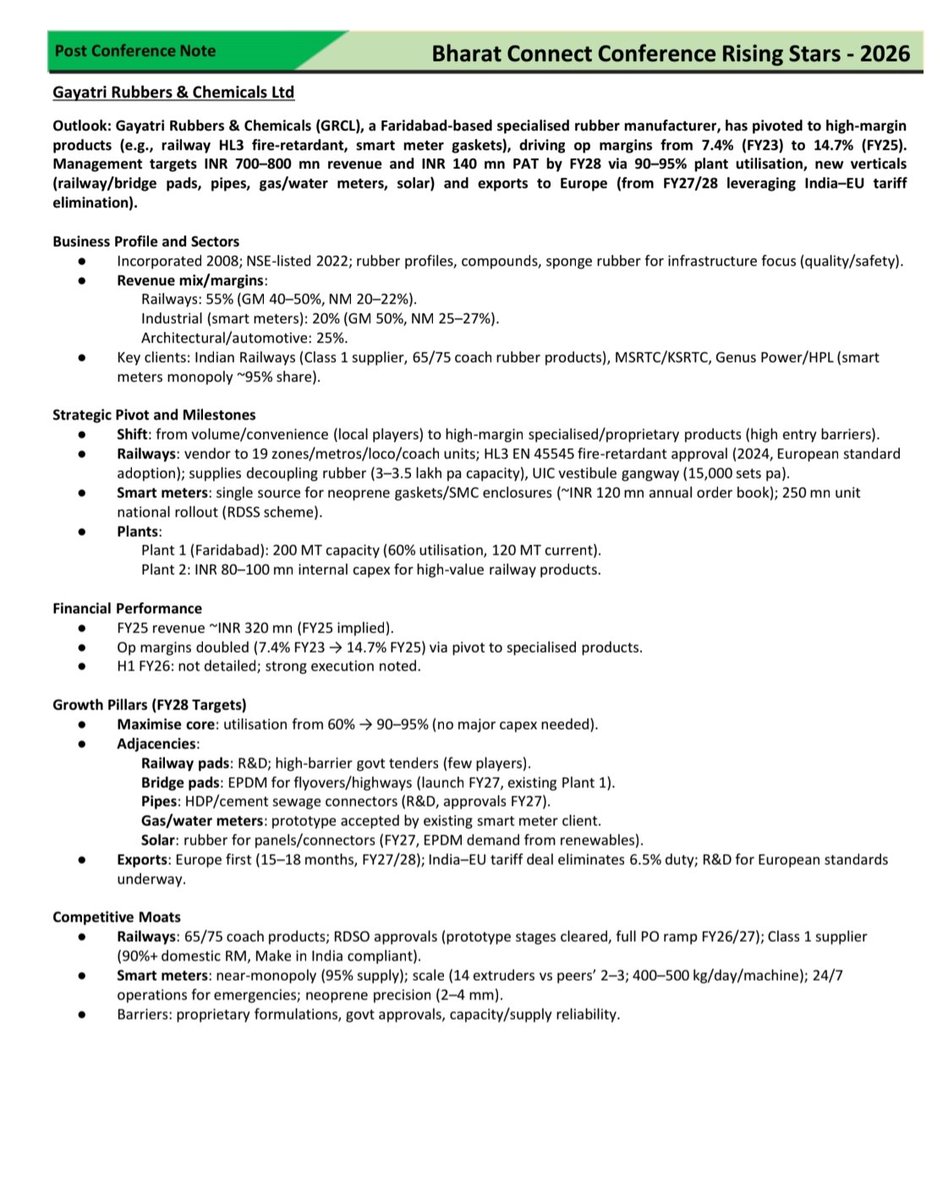

Gayatri Rubbers and Chemicals (#GRCL)

My largest holding & highest conviction company 🤩 Relatively unknown company with great future. ✅🙏

Disc : I hold 2.33% of company and have increased stake 4 months back 💪🙏

My reasons for investment in #GRCL : Honest, hardworking promoters who underpromise and over-deliver every time 🙏

I have done factory visits and attended physical AGM.

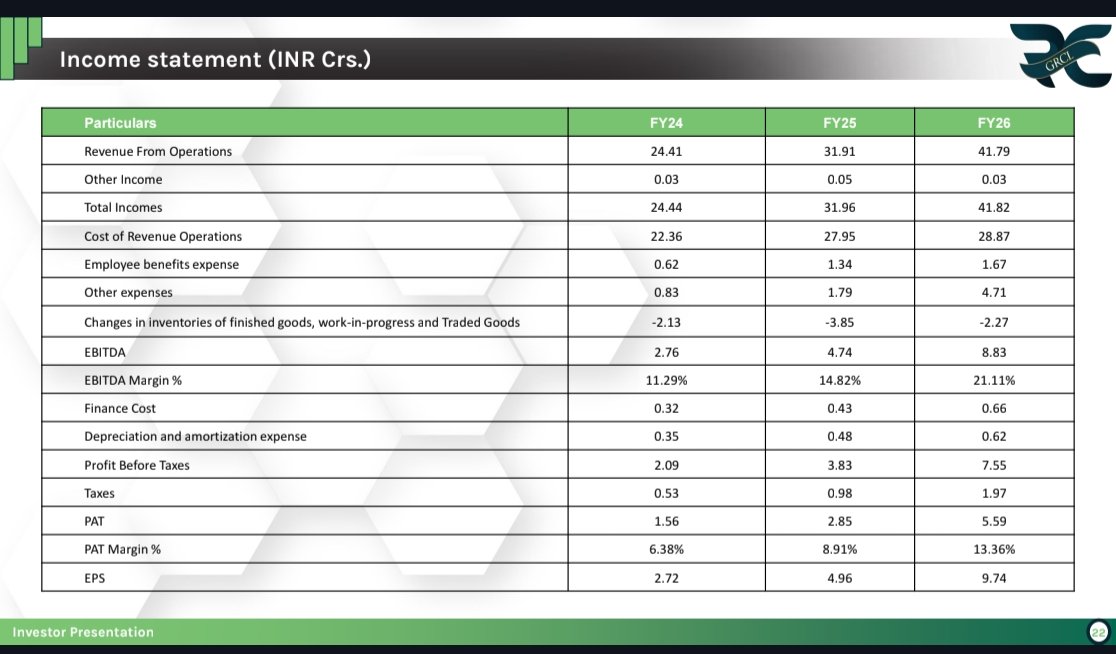

GRCL's PAT has almost doubled this year and it is growing at 83% CAGR since listing(last 3 years). 🥳

Company's PAT margins are close to 13.4%. A company growing at this pace every year with good margins & excellent promoters should trade at comparatively high valuations.

GRCL: The Non - Tyre rubber company.

A company to ride Railway , Smart Meters , Water/Gas meters , Infrastructure , Automobile etc themes simultaneously.

GRCL makes speciality rubber products which are used in Indian Railways, Smart Meters , Automotive and Architectural sectors. It is not a commodity or cyclical business. It makes speciality rubber products. 😊

Their 2 speciality high value products - 'Intercar Gangway' and 'Absorption Strips' are used in Vande Bharat and other trains. They have recently entered into silicon mobile holders to be used in trains.

There are 75 different kind of rubbers used in trains. GRCL makes 65 out of those 🤩

They are planning to venture into 5 new verticals-

1- Rubber pads

2- Bridge pads

3- Solar T shaped Rubbers

4- Gas /Water meter rubbers

5- Pipes

Company is constantly shifting to high margin products which is visible from its profitablility growth.

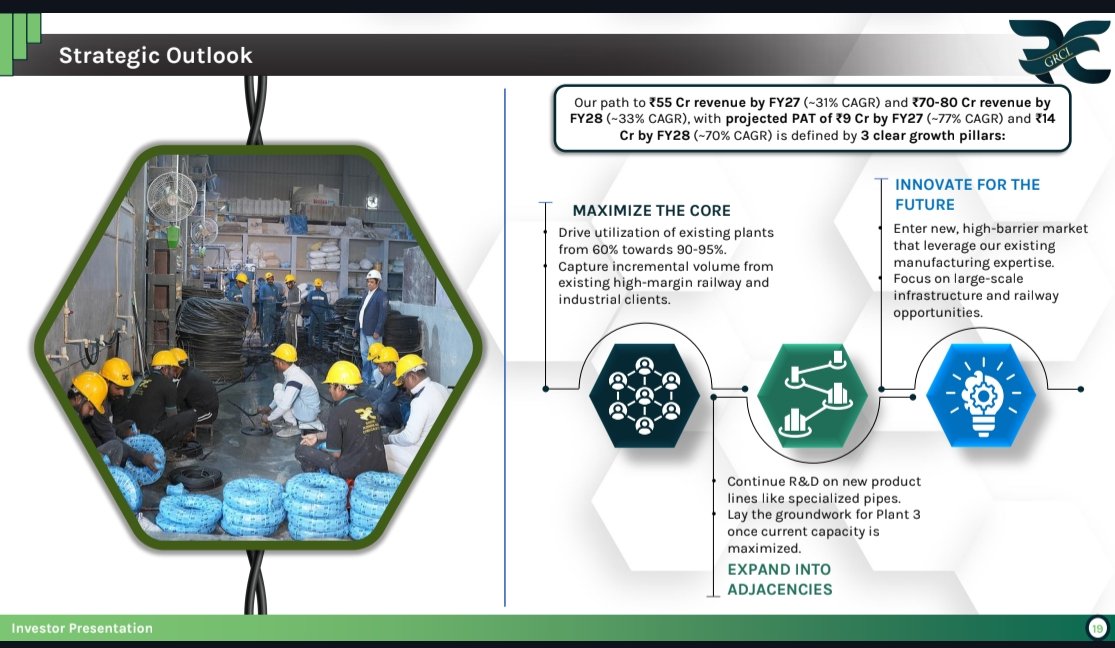

For FY27 , management has guided for 55cr+ topline and 9cr+ PAT (more than 60% growth)

For FY28 the guidance is 70-80cr revenue with 14cr+ PAT(150% growth 🫡)

I am sure they will beat this too like they have been doing till now .

After listing they gave PAT of 91L(FY23) and in just 3 years they have reached 5.6cr PAT(FY26) . Growth 🤯

Key fundamental features of company -

ROCE -40%

ROE -33%

Almost debt free.

Promoters have recently increased stake to 74.06% .

Technical perspective - Stock is looking to breakout after long consolidation and making inverse H&S .

This is a boring evergreen business which is constantly growing under the guidance of best management I have seen till date.

The management is doing concall tomorrow at 4pm. They recently did concall organized by Arihant capital.

Note : Illiquid stock. Not a buy/sell reco.

Just for educational purposes.

#GRCL

#GayatriRubbers

#Investing