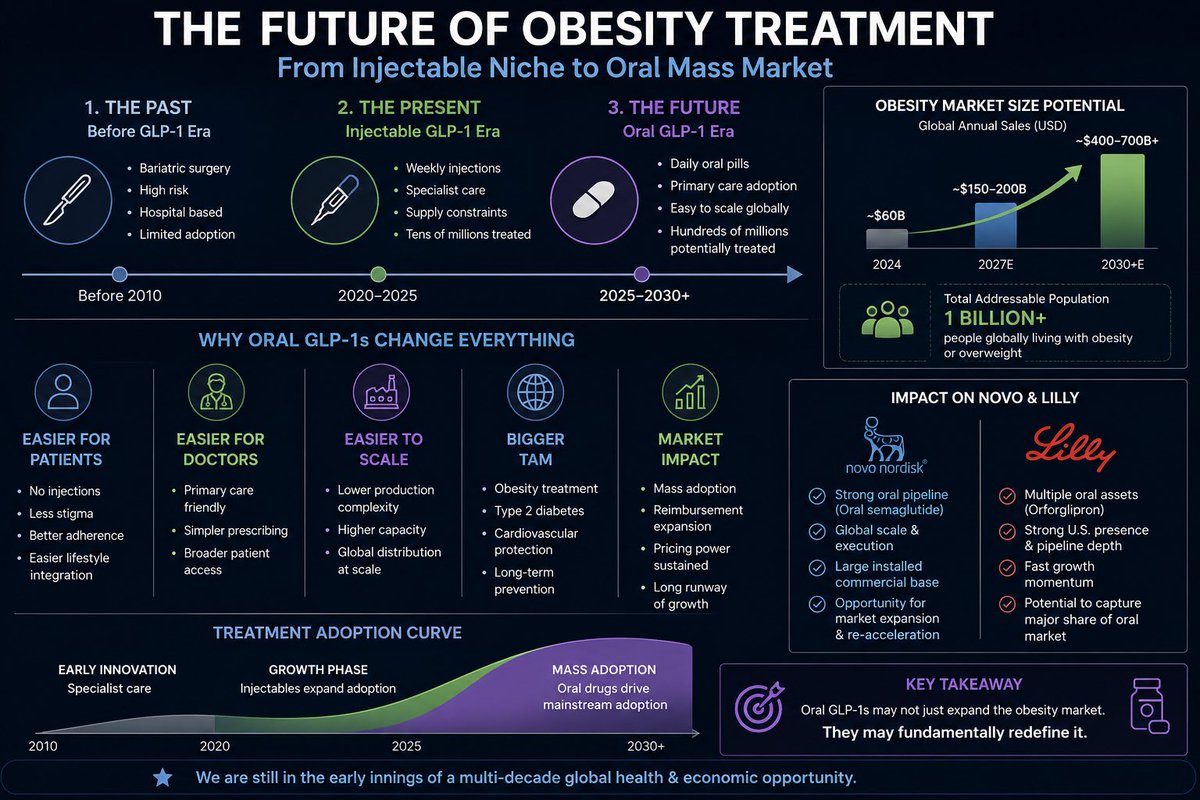

Many still underestimate how transformative oral obesity drugs could become.

Easier for patients, easier to scale, easier for primary care. Over the next few years, oral GLP-1s may reshape the entire obesity market for both $NVO and $LLY.

English

Peter Törngren

1.4K posts

@peter_torngren

Gillar börs, index, analyser. Tweets är inte råd utan endast jag som ventilerar mina privata tankar. Fil kand i Systemvetenskap och Ek kand i Företagsekonomi.

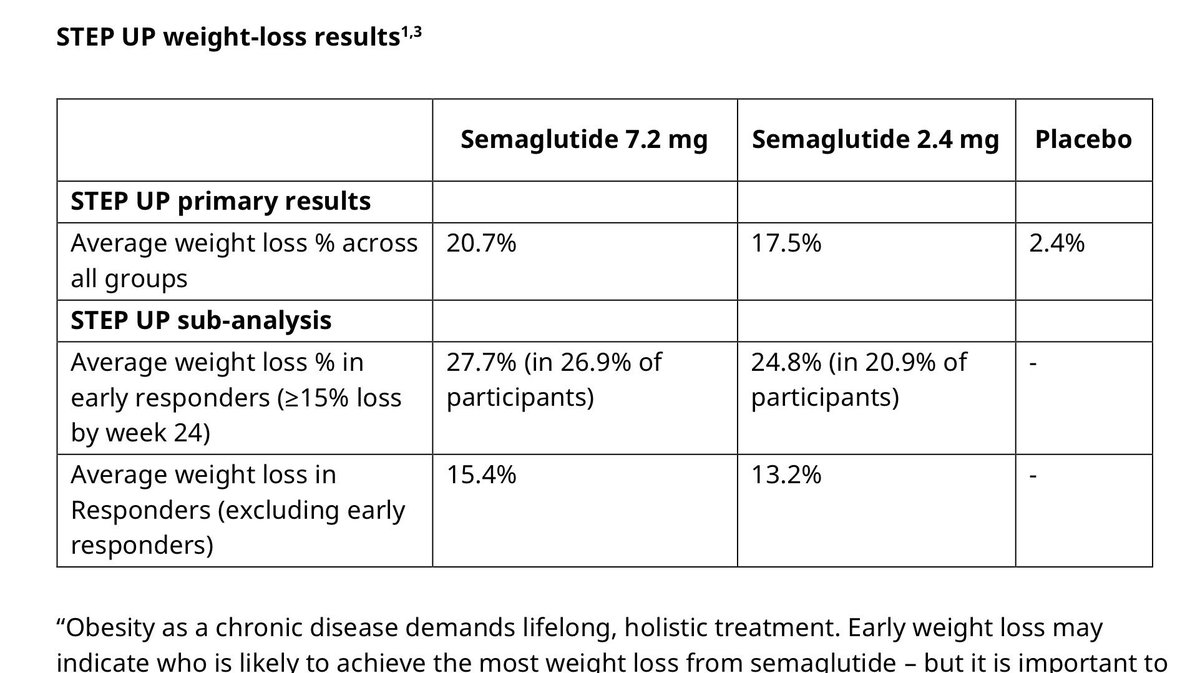

Lots of new $NVO wegovy data. In a new post-hoc analysis presented by Novo Nordisk at the European Congress on Obesity (ECO) 2026 in Istanbul, premenopausal women with obesity lost an average of 22.6% of their body weight using a weekly high dose of Wegovy (semaglutide 7.2 mg) compared to placebo. Key Findings from the Study The analysis is based on data from the STEP UP clinical weight management trial and highlights several critical points: Higher dose drives greater loss: The average 22.6% weight loss was achieved using the new, higher investigational dose of semaglutide at 7.2 mg once weekly. Consistent across life stages: The data demonstrates that Wegovy provides significant weight loss in women with obesity regardless of whether they are premenopausal, perimenopausal, or postmenopausal. Lower risk of depression: Women in the study taking Wegovy alone had a 25% lower risk of developing depression compared to women receiving menopausal hormone therapy alone. $LLY $VKTX

$NVO $NOVO Nordea attended Novo Nordisk's Meet-the-Management on Thursday in London and noted several interesting points during the day. Firstly, Novo Nordisk is sharpening its commercial focus on building a brand around Wegovy rather than being a GLP-1 producer. An important difference in Nordea's opinion. In this context, it is interesting that Wegovy is becoming the leading household brand in obesity treatment in the US according to Google Trends, with the shift in trend visible around the turn of the year. This is in line with the development in prescriptions, where Novo Nordisk continues to show solid demand for Wegovy (pill), while Eli Lilly's launch of Foundayo remains subdued, Nordea notes. Nordea also understands from the sessions that the volume increase from the Medicare Part D bridge program in H2 2026 is only an insignificant part of Novo Nordisk's own expectations - at least at the low end of the range.