Sabitlenmiş Tweet

Ramadan Mubarak! Inshallah, this will be the first #Ramadan where you can actually buy Iftar and make Zakat using crypto to pay local rails (i.e M-Pesa)

GIF

English

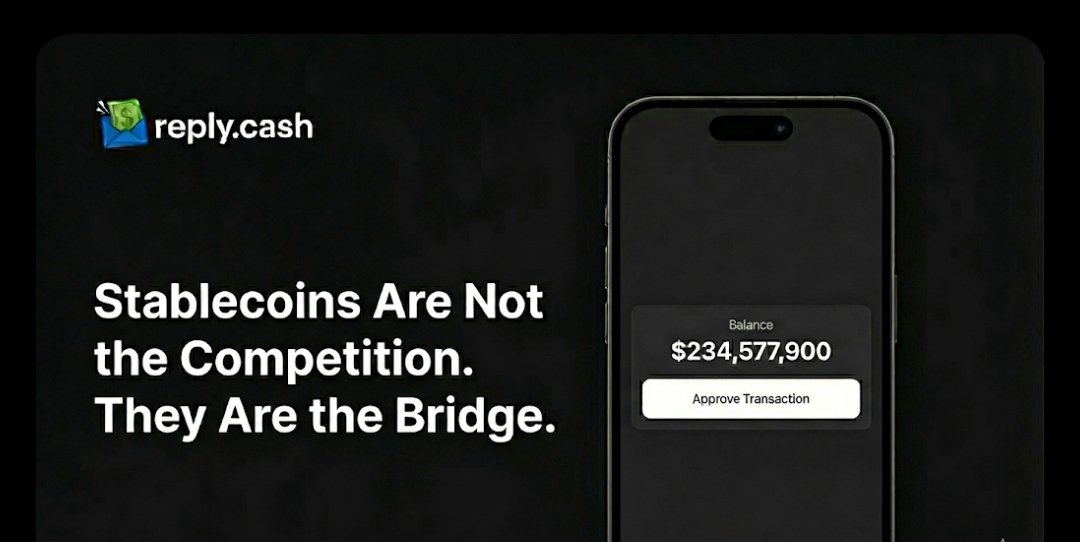

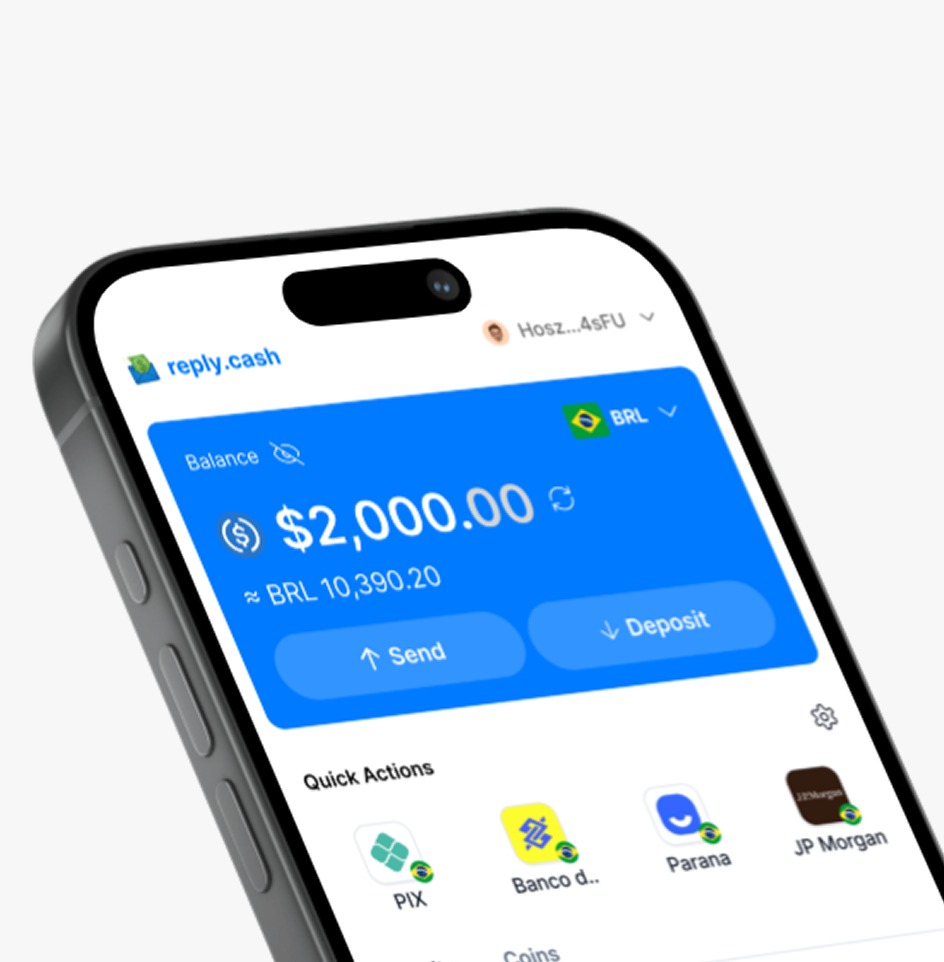

reply.cash

209 posts

@replydotcash

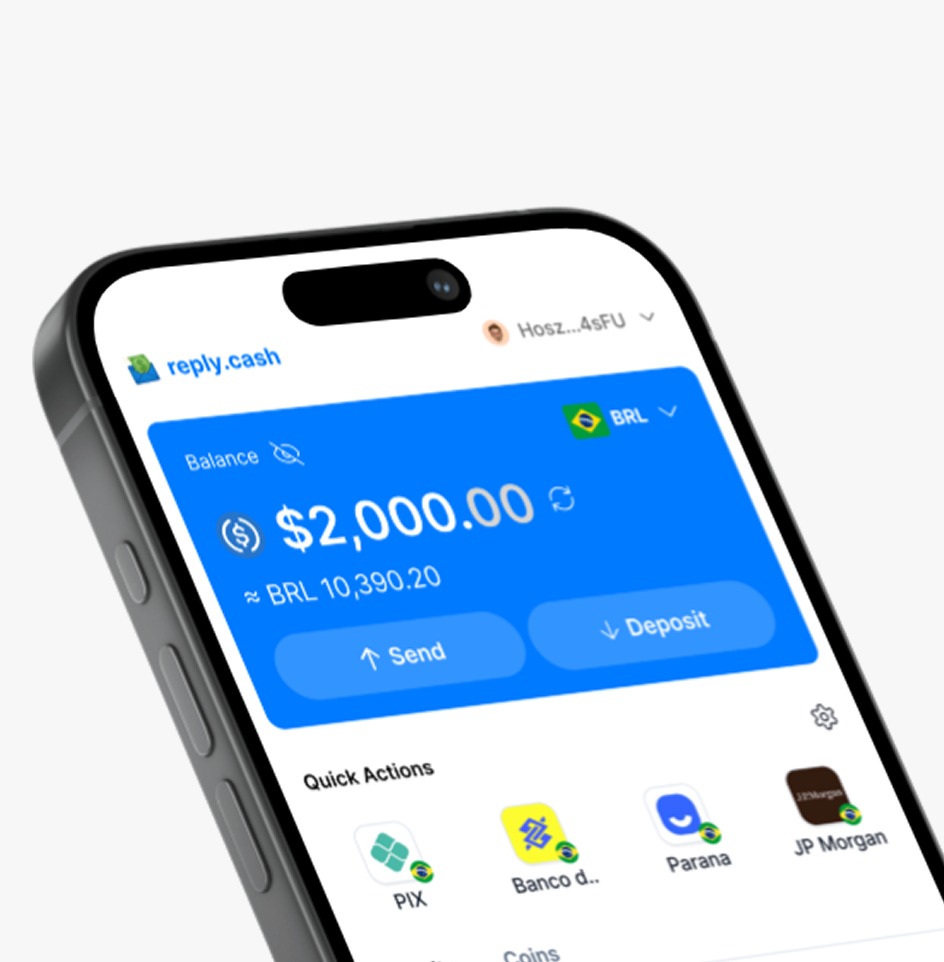

Use stablecoins to pay people & merchants through local rails privately Now live in 🇰🇪 Kenya & 🇳🇬 Nigeria soon 🇬🇭🇨🇩🇷🇼🇲🇼🇧🇷🇨🇴🇺🇬

Same-day payments for international contractors are now live in Gusto. Wise Account or USDC stablecoin - contractors pick what works for them. Employers pay the same way they always have.

We built this model from @NEARProtocol fee data and real volume trajectories, not top-down market size projections. Recent inflation reduction and fee switch activation are the two structural events around which the analysis is built. This article from @sal_ternullo lays out the mechanics in full.

Today we made a major upgrade to Brave Wallet. We've added support for NEAR Intents, which allows you to easily swap crypto assets across blockchains (Bitcoin, Solana, Zcash, Cardano, and EVM) within our browser.

BREAKING: @WesternUnion is launching USDPT, a new stablecoin on @solana. @Crossmint will power wallets and payment APIs connected to Western Union's Digital Asset Network. Stablecoins will be redeemable through 360,000 cash locations in 200+ countries. x.com/crossmint/stat…

" Stablecoins are the next evolution of money... and just like cards, will enable a whole new set of capabilities. And we're starting to see that today." @zcabrams of @Stablecoin and @stripe on how cards changed commerce, and why the next wave of fintechs will be built on stablecoins.