Investor Feed@_Investor_Feed_

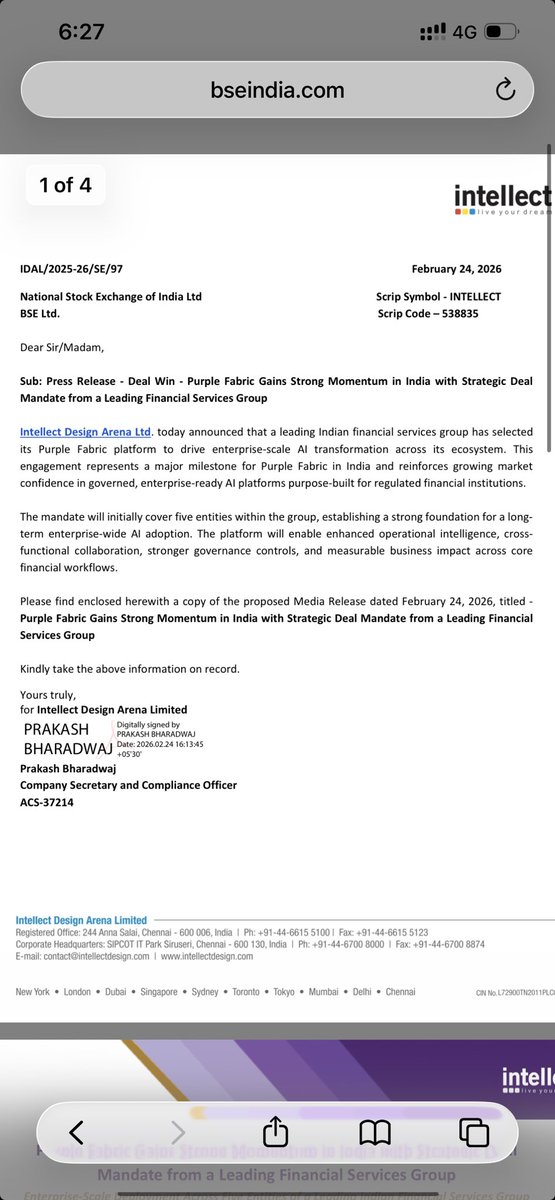

Intellect Design Arena Launches HR TeamSpace at ₹99,500/Month 🤖 | MCap 10,586.58 Cr

• HR TeamSpace is a secure AI environment for HR teams

• Priced at ₹99,500 per month for up to 50 users

• Built on Intellect's Purple Fabric platform

• Replaces manual HR tasks and isolated AI experiments

• Enables deployment of pre-built AI agents with enterprise security

• Key use cases: recruitment automation, personalized coaching, policy queries

• Supports IndiaAI's mission for responsible AI adoption

Find Source & similar updates -> investorfeed.in/posts/87446

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.