Nero Scott retweetledi

Nero Scott

687 posts

Nero Scott

@scottnero56

Crypto, stocks, and whatever the news cycle throws at us. I make complex things simple. $BTC $ETH | Huge on $SLNH & $BMNR

Canada Katılım Kasım 2024

168 Takip Edilen89 Takipçiler

Nero Scott retweetledi

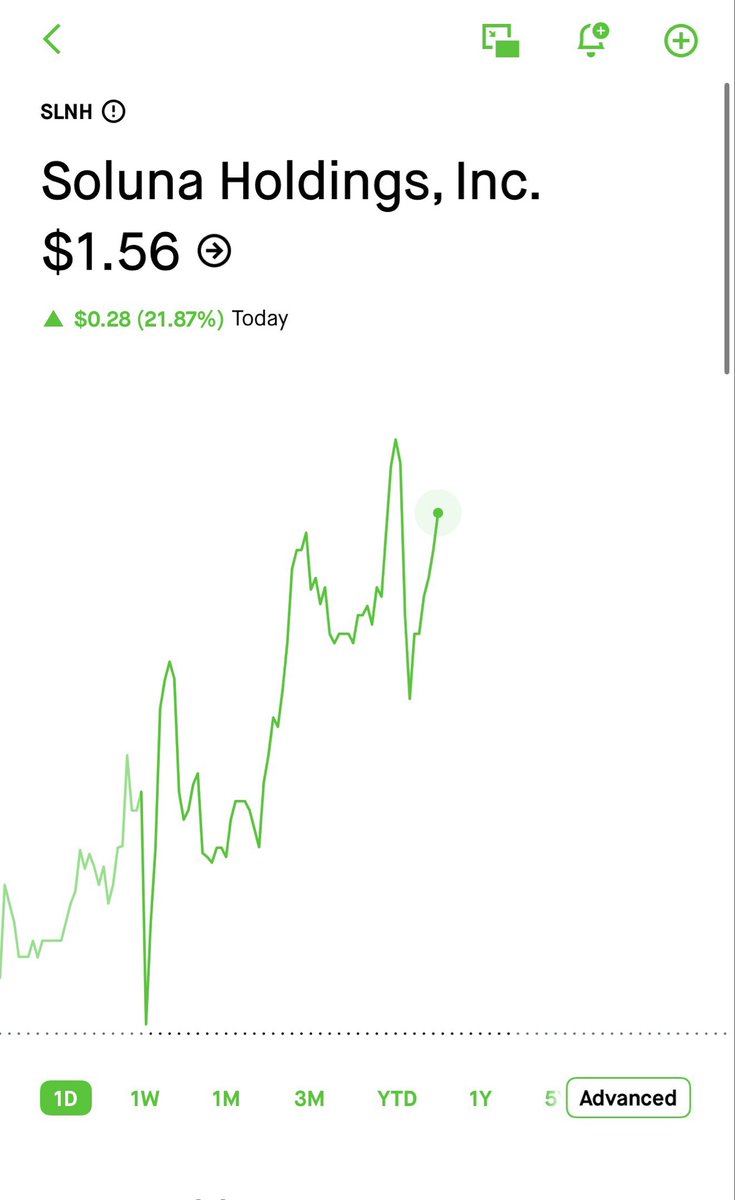

$SLNH I see a lot of attention towards this position right now with some big players taking a position

- Channel breakout on the 11th of April

- Wave 1 moved to the 200 Day MA

- Wave 2 pulled back to the 50 Day MA and held support between the 0.618 - 0.78 Fib range (standard)

- Bouncing now back above the 200 Day MA and moving to our Wave 3 target at $2.63

- +80% gain from here

- from a technical view, this looks good

-Wave 5 target is $3.68

Current price is $1.39

English

Nero Scott retweetledi

Chamath Palihapitiya just laid out the most important valuation question nobody on Wall Street wants to answer.

For 20 years, the Mag 7 won because they had the greatest business model ever invented, asset- ight software.

You write the code once, you sell it to a billion people, the marginal cost of the next customer is basically zero.

There is essentially no factories, no raw materials, no union workers, no physical infrastructure, just pure leverage, scale the revenue, barely scale the costs.

That's how you get 30x, 50x, 60x earnings multiples and the market was paying for compounding economics that had no natural ceiling.

But AI just blew that model up.

The hyperscalers, Amazon, Microsoft, Google, Meta are now projected to spend between $600 and $725 billion on capex in 2026 alone, up from $250 billion just two years ago.

That number is climbing, not plateauing and it's not just the chips and the data centers, it's the energy contracts underneath all of it.

When Microsoft re signed Three Mile Island, they locked in a 20 year forward purchase agreement at more than $100 per megawatt hour nearly double the prevailing spot rate of $60 for wind and solar in the same region.

That's a long term liability commitment baked into operating cash flows for two decades.

Here's where Chamath's math gets uncomfortable.

These five or six companies are now collectively spending so much that their capex has exceeded their free cash flow meaning they can no longer self fund growth from operations alone.

In 2025 alone, hyperscalers raised $108 billion in new debt and projections put the total debt issuance over the next few years at $1.5 trillion.

These are companies that, for two decades, were net cash accumulators and now they're going to the debt markets like everyone else with term loans, revolvers, and structured credit facilities.

That's Chamath's core point and it's a devastating one for anyone still modeling these companies the old way.

When a company is asset light, investors pay a premium for that lightness and the multiple reflects the belief that returns on capital will stay high indefinitely, because there's no heavy physical plant dragging them down.

But when Google starts looking like a utility locked into 20-year energy contracts, carrying hundreds of billions in debt, spending half its revenue on physical infrastructure, the rational multiple compresses.

You don't price a utility at 30x earnings, you price it at 12x.

His conclusion is that stop trying to value the hyperscalers themselves and follow the money instead.

A trillion dollars a year is flowing out of these companies into power companies, data center operators, chip manufacturers, cooling systems, fiber networks, rare earth metals.

The companies on the receiving end of that spending are already underpriced because the market is still staring at the senders while ignoring who's cashing the checks.

The asset-light era minted the most valuable companies in human history and the asset heavy era that's replacing it might be the best argument yet for owning everything around them instead.

English

Nero Scott retweetledi

Soluna has regained compliance with Nasdaq’s minimum bid price requirement.

Our shares maintained a closing bid price of $1.00+ from April 14 to April 29, 2026, and Nasdaq has closed the matter.

We appreciate our shareholders’ support as we remain focused on disciplined execution, scaling our Renewable Computing platform, and building durable long-term value.

We keep pushin’.

$SLNH @SolunaHoldings

Learn more here >>

solunacomputing.com/news/nasdaq-co…

English

Nero Scott retweetledi

$SLNH an Asymmetric Bet⁉️

A $160M market cap company sitting on 4.3 GW of renewable power, a wind farm they fully own, and an AI data center strategy about to flip the switch.

Most people have never heard of Soluna Holdings - $SLNH.

Here's why Soluna Holdings could be one of the most asymmetric plays in AI infrastructure right now. 🧵

Bookmark this post for further references!

Read further below! 👇

English

Nero Scott retweetledi

$SLNH

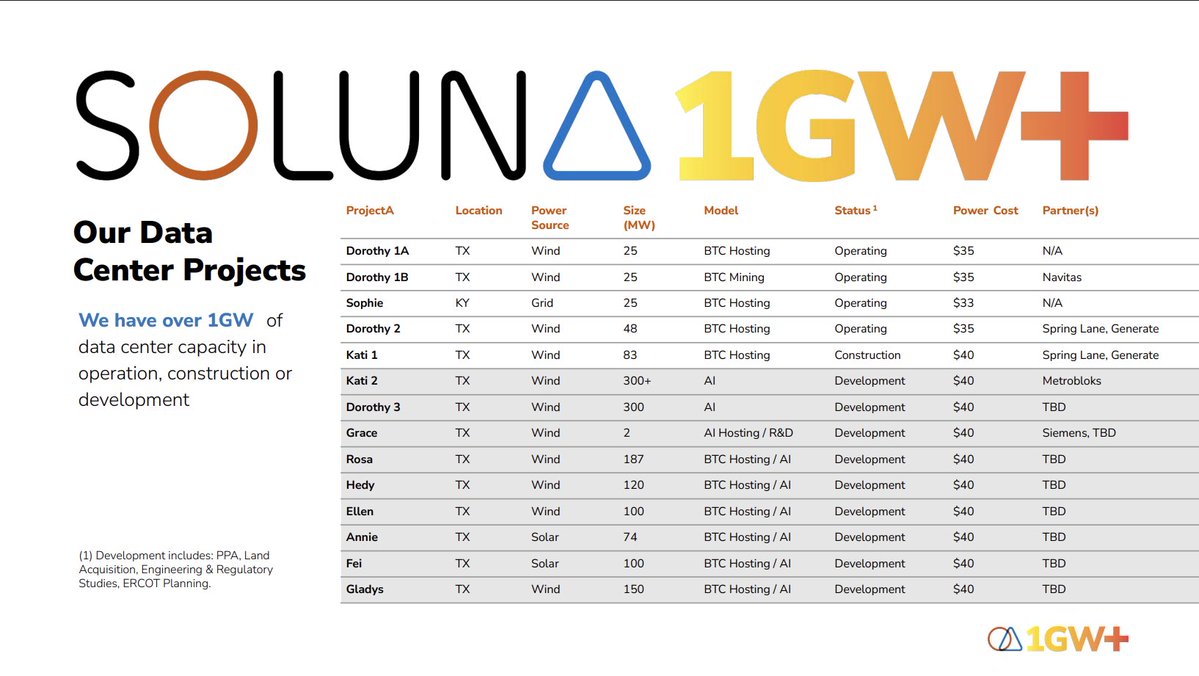

Kati 2 was originally an 83 MW project that got upsized to 100 MW and then to 350 MW in partnership with Metrobloks.

It’s likely that potential tenants require a larger capacity to move the needle for them.

Then they have 300 MW under development at Project Dorothy 3.

So, you are looking at roughly 650 MW capacity under development.

At the current industry rates ($1.5 million/year per MW) it can generate $975 million revenue.

Kati 2 is a JV, so assuming 50/50 revenue share, $SLNH can generate $712.5 million from these sites alone.

Even if it can achieve 1/3 of this, we are looking at $237.5 million revenue add.

Market cap is $240 million today.

Definition of an asymmetric bet.

English

Nero Scott retweetledi

Seeing a lot of talk recently about $SLNH and after a good amount of research Just opened a long position in $SLNH this morning at $1.40.

Small. Speculative. But the setup is genuinely interesting.

Soluna Holdings is not what most people think it is.

Yes it started as a Bitcoin miner. But what it is actually building is something completely different.

The core thesis is simple.

Renewable energy generates massive amounts of surplus power that the grid cannot absorb. Wind farms and solar fields produce electricity at odd hours when nobody needs it. That power gets curtailed and wasted.

Soluna builds modular data centers co-located directly with those renewable sources and converts that stranded energy into computing resources. Behind the meter. Cheaper than anything on the grid.

Here is what they have actually built.

They just closed a $53 million acquisition of the 150MW Briscoe Wind Farm in West Texas.

That deal makes them fully vertically integrated at Project Dorothy. They now own both the electrons and the racks.

Management guided $20 to $24 million in annualized revenue and $6 to $11 million in first year EBITDA from Briscoe alone.

For a company that did $29.7 million in revenue last year that is a meaningful step change in a single transaction.

Kati 1 at 83MW reached substantial completion ahead of schedule.

Kati 2 at 100MW is advancing through technical validation as a dedicated AI and HPC facility.

Project Dorothy 3 is a planned 300 plus MW renewable powered AI compute campus on 300 adjacent acres at the same West Texas site.

$88.8 million in cash. $100 million project finance line with Generate Capital. 4.3 gigawatt development pipeline.

The pivot from Bitcoin hosting to AI compute is already underway. Active discussions for 350MW of critical IT capacity. Kati 2 specifically designed for AI and HPC workloads.

Now the risks. They are real and worth saying clearly.

Still deeply unprofitable. $57 million net loss in 2025. Negative free cash flow. 26.51 million shares just registered for secondary sale creating overhang.

Bitcoin still makes up a significant chunk of current revenue. Execution on Kati 2 and Dorothy 3 is not guaranteed.

This is not a core position.

It is a speculative bet on a company that owns the two scarcest inputs in AI infrastructure simultaneously. Renewable power and permitted data center land.

At a market cap that does not come close to reflecting what the pipeline could be worth if executed.

Small position. Eyes open.

English

That’s a fair point.

There are definitely parts of the model that aren’t fully proven yet, but that’s the nature of something this early. If everything was already built out and de-risked, it wouldn’t be trading here. I’m betting on the team to execute and evolve this from a small BTC-focused business into something much bigger.

English

@scottnero56 True, but they haven't shared any plan at all. $40 power cost appears to be the aggressive number. They will have rely on traditional sources to support HPC/AI

English

Been digging into a small-cap name that’s actually interesting: Soluna Holdings $SLNH

They’re building data centers directly next to wind/solar farms and monetizing stranded energy — power that would otherwise be wasted.

Today it’s mostly BTC mining/hosting.

But the real angle is where this goes:

→ AI / HPC compute demand is exploding

→ Power is becoming the bottleneck

→ Soluna is positioning as a low-cost, flexible energy + compute layer

They’re still early:

• Small operating base

• Large development pipeline (a lot not built yet)

• Execution + funding risk is real

But that’s also where the asymmetry comes from.

CEO @jbelizaireCEO is worth following — very active, consistently explains the thesis, and actually engages.

This looks like a real opportunity hiding in plain sight.

Microcap (~$150M), so it doesn’t take much for this to move.

If they execute → this re-rates fast

If they don’t → it stays a story

What would you pay to get early exposure to compute infrastructure like CoreWeave or Nebius at this stage?

I just bought in. Positioning while it’s still mispriced.

English

Just watched a deep dive on Soluna Holdings $SLNH, got a lot out of it. @McnallieM

Biggest takeaway for me: their pipeline is clearly shifting toward AI.

Their next major projects:

→ Kati 2: 300+ MW (AI)

→ Dorothy 3: 300 MW (AI)

That’s a massive step up from their current operating sites (~25–50 MW).

We’re talking ~4–10x scale on future builds.

Still early, still in development — but if they execute, this is where the story changes.

Worth a watch: youtube.com/watch?v=LjCHp8…

YouTube

English

Good question, the photo below explains how they’re thinking about it.

Most of what’s operating today is smaller-scale BTC hosting/mining (flexible load).

The bigger AI projects (300MW+) are still in development — likely where you’d see more stable + hybrid power setups.

So yeah, stranded energy alone isn’t enough yet, but that’s exactly what they’re trying to scale into.

Still early.

English

@scottnero56 Who would build the data center? How would they manage the uptime ? Stranded energy alone doesn’t work with AI

English

Nero Scott retweetledi

I gave you probably the most asymmetric play on the data center realm months ago: $SLNH

Looks like Mike Alfred also discovered it.

Here is the thesis:

All cloud providers accelerated compared to the same quarter last year and they all said the same thing:

“We could grow faster if we had more capacity.”

At this stage, main limiting factor is power and permitting, as illustrated by the delays in $NBIS New Jersey data center.

If you have the capacity and secured the power, you are golden.

This is $SLNH.

It builds data centers co-located directly with renewable power plants behind-the-meter, to use energy that would otherwise be wasted or “curtailed”.

It currently has over 100 MW AI-ready capacity in Project Kati 2 with possible expansion to 300 MW.

Project Dorothy 3 also has 300 MW capacity.

Even if it can monetize only this 400 MW currently under development at the industry rate of $1.5 million/year per MW, it’ll generate $600 million annual revenue.

Current market cap is just $190 million.

One of the most asymmetric opportunities in the market.

There is also further optionality as their total pipeline hit 4.3 GW as of March.

Even if it can energize a quarter of this pipeline, we are looking at $1.5 billion revenue.

There isn’t a more asymmetric play in the whole data center space. It’s worth 1% position in every portfolio imo.

Long $SLNH.

Mike Alfred@mikealfred

Connected with an incredible group last night: Justin Blau, Phillip Lord, Michael Saylor, Brandon Lutnick, Phong Le, Frank Holmes, Gary Vecchiarelli, Salman Khan, and more. Interestingly met @jbelizaireCEO, CEO of Soluna, for first time. Very credible. Bought 100k shares just now

English

Nero Scott retweetledi

Good dialogue here for newbies. @SolunaHoldings $SLNH

Dr. Paul Christianson@disruptorinvest

Thanks to everyone for attending our interview with @jbelizaireCEO of @SolunaHoldings. It was a very insightful conversation not only about $SLNH but the industry in general. Here is a recording if you were unable to attend live. x.com/i/spaces/1DxLd…

English

Nero Scott retweetledi

Connected with an incredible group last night: Justin Blau, Phillip Lord, Michael Saylor, Brandon Lutnick, Phong Le, Frank Holmes, Gary Vecchiarelli, Salman Khan, and more. Interestingly met @jbelizaireCEO, CEO of Soluna, for first time. Very credible. Bought 100k shares just now

English

Nero Scott retweetledi

I’m noticing a lot of foreigners who seem to not understand why we’d risk hundreds of lives, spend millions of dollars, and sacrifice several aircraft to rescue one guy. And the reason they don’t understand is also the reason people can’t be made American by a piece of paper.

Daniel Foubert 🇵🇱🇫🇷@d_foubert

Lose all this to rescue 1 pilot and call it your greatest military success of all time.

English

Nero Scott retweetledi

MUST SEE:

This discussion about patriotism turns into a roast QUICKLY!

Caleb Hammer lets them have it!

English