Sestio

62 posts

Sestio

@sestiofinance

AI-Powered Portfolio Analytics & Risk Intelligence

Katılım Mayıs 2025

8 Takip Edilen8 Takipçiler

When prediction market odds jump after a macro shock, what you’re seeing is a repricing of the probability distribution.

The real challenge isn’t estimating one event.

It’s modeling how multiple events interact:

• war escalation

• inflation prints

• approval ratings

• election outcomes

Once traders start holding positions across these markets, it becomes a portfolio risk problem, not a single bet.

English

BREAKING: The odds of the Democrats winning the Senate in midterm elections surge to a new high of 47%.

Democrats also have a record 85% chance of winning the House of Representatives.

Odds have surged since the Iran war began.

English

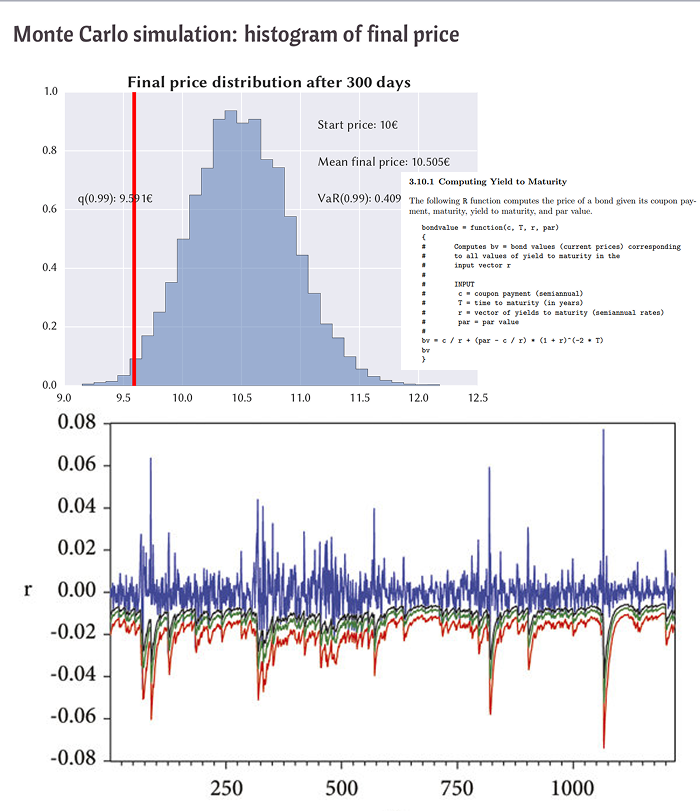

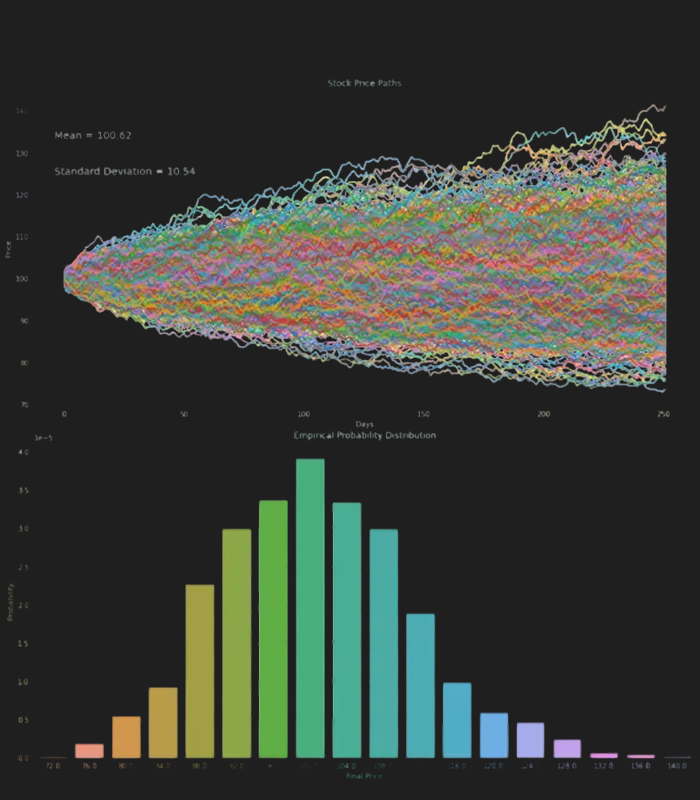

Most Polymarket traders look at a price chart and see a line

What they should see:

→ A Monte Carlo distribution of possible outcomes (not one path - thousands)

→ Volatility clustering that tells you exactly when to widen spreads

→ Formulas that turn "I think YES" into a precise expected value

The gap between intuition-based trading and model-based trading is the gap between losing slowly and compounding edge.

Good breakdown of the MIT math that actually applies here.

Roan@RohOnChain

English

@hanakoxbt Kelly is optimal under independence. In practice, correlated resolution shocks turn “fractional Kelly” into implicit leverage.

English

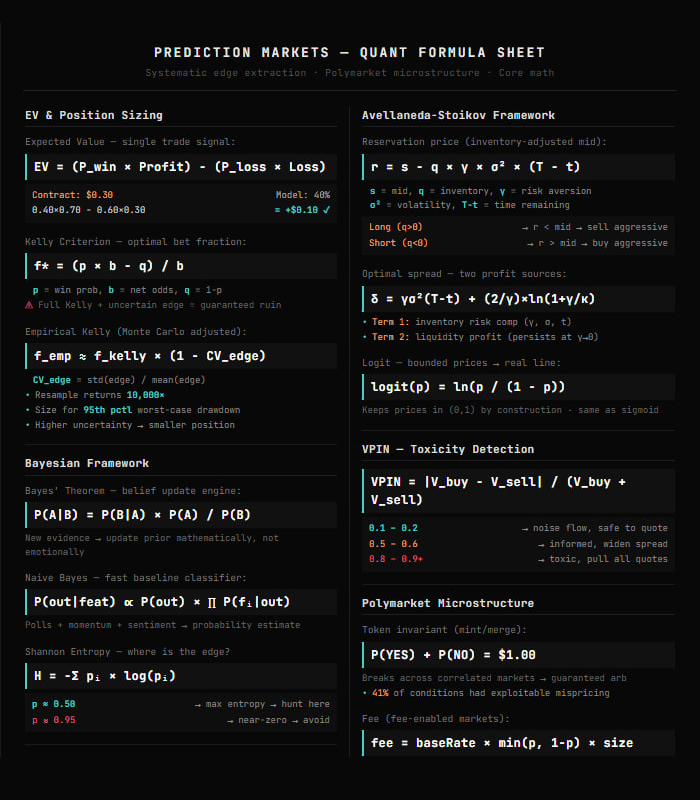

Quants compute EV on every single trade - retail just guesses

You see a Polymarket contract at $0.30 and think "that feels low."

A quant opens same contract and the edge is already calculated.

The difference between you and them is one equation:

EV = (P_win × Profit) - (P_loss × Loss)

$0.30 contract. Model says 40% true probability.

EV = (0.40 × $0.70) - (0.60 × $0.30) = +$0.10

That $0.10 is not a guess.

It's a systematic signal repeated across hundreds of contracts simultaneously.

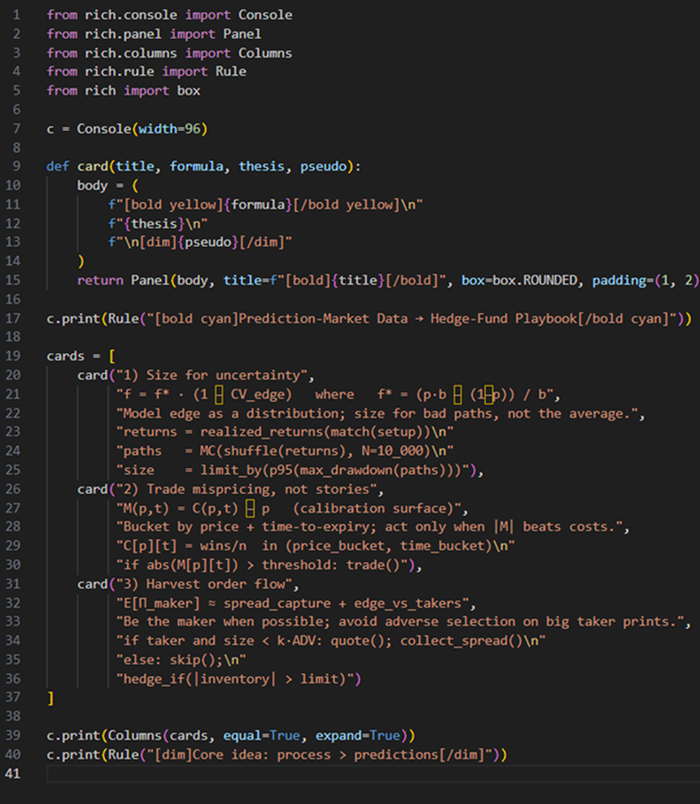

But knowing EV isn't enough. You need to size it:

f* = (p × b − q) / b

And even Kelly lies to you - it assumes your probability is perfect.

It never is. That's why institutions haircut it:

f_empirical = f_kelly × (1 - CV_edge)

One contract means nothing.

Hundreds of +EV trades with proper sizing - that compounds into a career.

Gut feel scales to zero.

Math scales to millions.

Roan@RohOnChain

English

$50 → $1,000/day

OpenClaw has been running for 72 hours straight

no breaks. no sleep. no mercy.

it uses Claude Sonnet to read the market like a chess engine - every 5 minutes it scans thousands of Polymarket contracts

Calculates true probability, and only bets when the edge is real

here's what happens every 5 minutes:

- Claude Sonnet builds a fair value model

- scans 9,900+ live markets

- ignores anything under 5% edge

- sizes the bet (Kelly criterion, capped at 8% bankroll)

- fires the order via CLOB

- profits pay for their own API costs

the agent has one rule: don't die

if balance hits $0 - it's over forever

may.crypto {🦅}@xmayeth

English

@herit01 @DrHansTrading @RohOnChain Win rate alone is misleading.

With ~50% accuracy, you need your average win > average loss just to break even.

Kelly only works if expectancy > 0.

If the edge isn’t there, sizing accelerates losses.

English

@DrHansTrading @sestiofinance @RohOnChain With this kind of stats I shouldn't be losing money but here I'm... That's why I took it upon myself to feel in my knowledge gaps... Cuz I can quickly pick up on patterns but I don't Kelly sizing doesn't intuitively come my primal brain 😄

English

The doom loop assumes fixed demand.

The abundance case assumes frictionless diffusion of productivity gains.

Reality is probably a distribution problem — who captures the gains, how fast they transmit to prices, and whether institutions adapt.

Market volatility is repricing uncertainty, not forecasting apocalypse or paradise

English

I spent 100 hours over the past week researching, writing and editing the piece we just put out.

It’s a scenario, not a prediction like most of our work. But it was rigorously constructed, dismissing it outright requires the kind of intellectual laziness that tends to get expensive.

And we’ve released it for free. Hopefully you enjoy it.

citriniresearch.com/p/2028gic

English

What’s fascinating is how quickly implied disruption risk gets priced into duration-heavy equities.

You can literally see factor exposures (growth, tech beta, long duration) light up after major AI releases.

It’s not just “AI replaces X” — it’s systematic repricing of future cash flow uncertainty.

English

Anthropic is quite literally targeting a new trillion-dollar industry every day now.

Every time a new Claude-based AI tool emerges, stocks in that industry are erasing $100B+ worth of market cap.

The craziest part?

We all know exactly what’s happening in real-time.

English

@jimcramer He's right that that agent/data pair is the weak link—at Sestio we treat every agent run like regulated output, encrypting it and streaming it through the same guardrails as our APIs so we can keep raising the risk budget instead of letting those workloads run unprotected.

English

I totally get the destruction of SAAS and Enterprise software but the agents-which are unprotected- and the data, which they generate much more than humans, is unprotected, so i would be raising numbers, pt, Crowdstrike, not lowering.

English

@k1rallik @Polymarket This is also why letting LLMs “estimate probabilities” internally is dangerous.

Without deterministic sizing + variance modeling, you’re just amplifying noise with confidence.

English

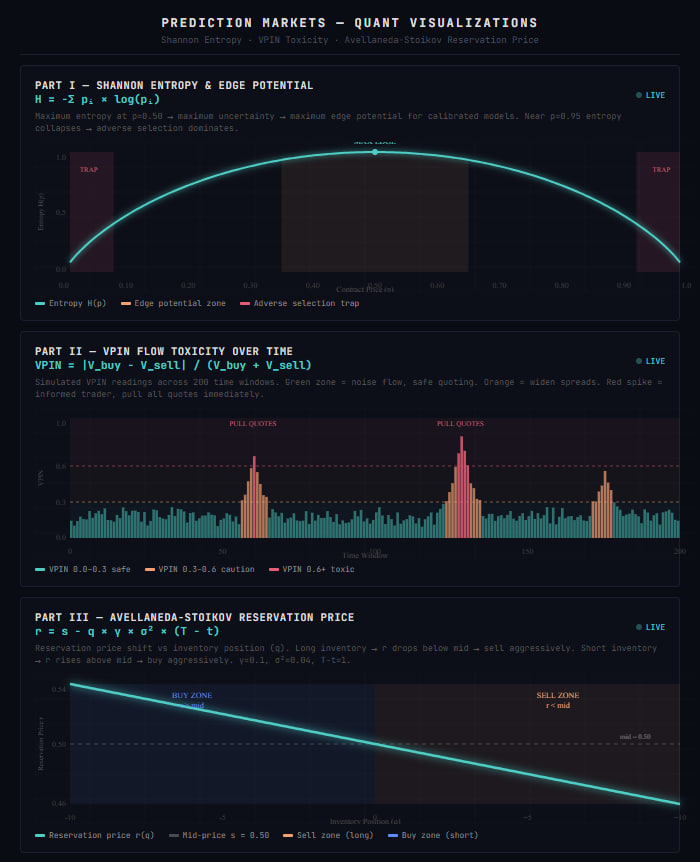

You're Not Losing. You're Just Playing the Wrong Game

Prediction markets aren't betting sites - they're a live lab for human bias and market microstructure.

A massive public dataset just dropped: 400M+ Polymarket trades.

Stop sizing positions based on "gut feeling". You're just donating money. Hedge funds haircut their Kelly size to account for uncertainty.

Formula:

Position = Kelly_Size * (1 - Uncertainty_Variance)

Mispricing is 2D: it's Price + Time to resolution.

Mispricing = Actual_Win_Rate - Implied_Probability

Find where the market is systematically wrong and only trade when the gap clears your costs.

The most savage takeaway: Makers structurally beat impatient takers. Not by predicting the future better, but by harvesting the spread from emotional retail flow.

Roan@RohOnChain

English

If you’re building finance agents, analytics should be infrastructure — not prompt engineering.

We built Sestio to be that layer.

Early access: sestio.com

DM if you’re integrating agents in fintech.

English