Will P

8 posts

I am back as promised :)

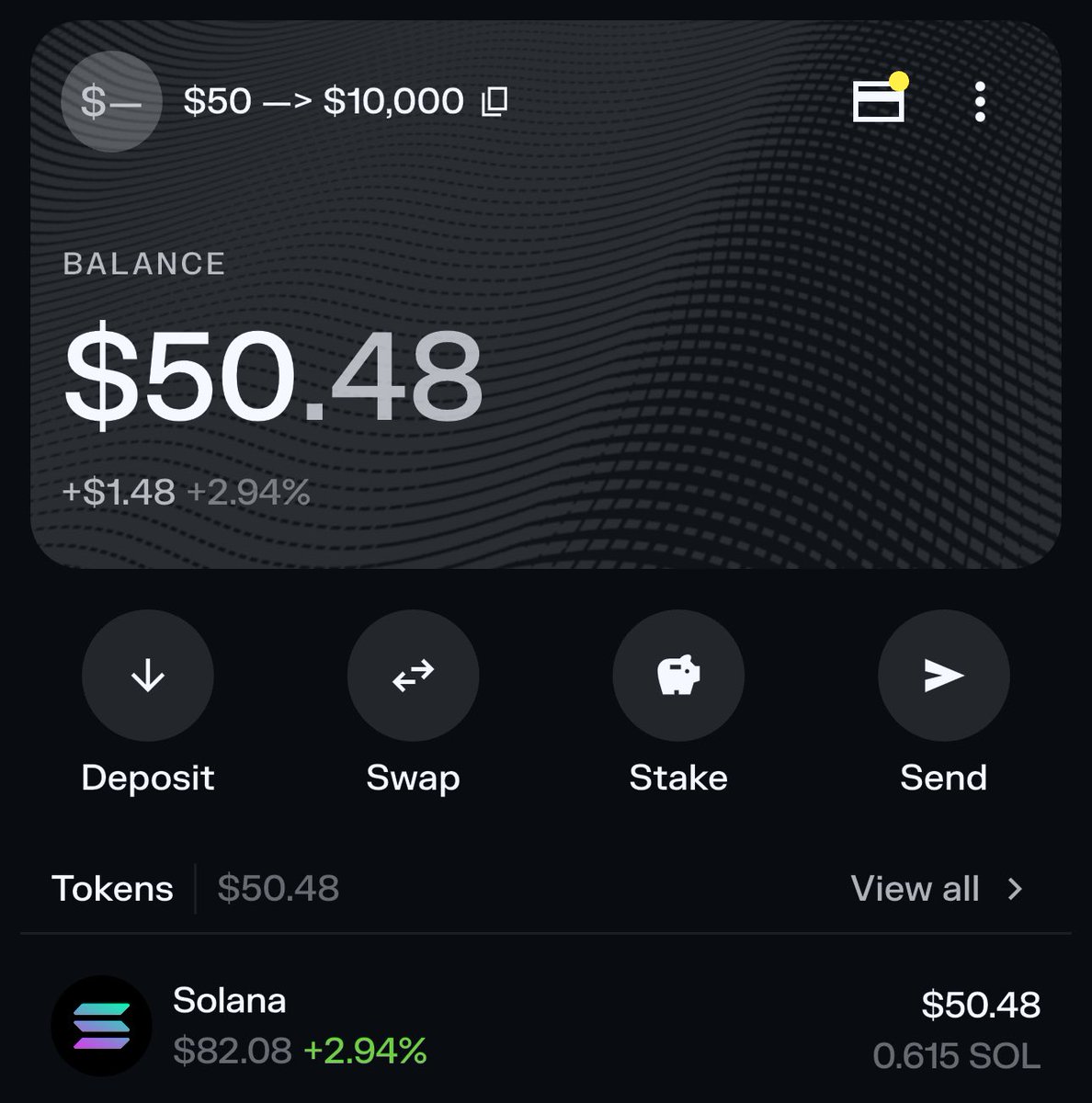

Time to start the $50 —> $10,000 challenge

Last time it took me about 7 days, will try doing it faster this time

If you want to follow want to follow along, comment below and I’ll send you an invite to the call group

Gonna lock comments in 24 hours

English

$ONDS Here is the truth:

Ondas is too cheap right now.

In no world should Ondas be down 7% YTD after everything they've accomplished this year.

At $9.45, Ondas has a market cap of roughly $4.4B with $1.55B in cash on the balance sheet.

That's an enterprise value of about $2.86B against $375M in guided 2026 revenue. Management has called that a floor. We all know by now that $375M is conservative.

EV/Revenue at current price is ~7.6x while Ondas is guiding 7x revenue growth.

The math gets even more ridiculous if the stock continues lower:

At $7 — EV drops to $1.72 billion. That's 4.6x.

At $6 — EV drops to $1.26 billion. That's 3.4x.

At $5 — EV drops to $790 million. That's 2.1x.

The stock is currently pricing in essentially zero premium on a business that just delivered 605% revenue growth and raised guidance by 120% in the same breath.

Cash per share alone is $3.32.

You're paying $6.13 above cash for everything else: the platform, the backlog, the acquisitions, and $375M in guided revenue that management has already called conservative.

Just something to think about. I have already held through multiple 50%+ drawdowns so I can handle this macro-driven weakness, but my conviction only grows.

It is my opinion only that anything below $10 is an obvious buy for a company of this quality.

I will now prepare myself for the tourists in the comments whining about dilution or whatever else they'd like to cry about today.

English