Q4 was when Amazon asked investors for patience.

Q1 was when it gave them evidence.

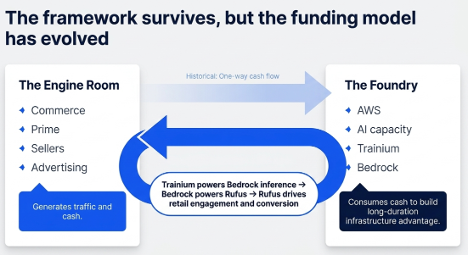

The $200B AI capex reset looked frightening because free cash flow was going to disappear. The question was whether Amazon was building ahead of demand or into demand.

Q1 points to the latter.

AWS accelerated to 28%.

Backlog surged to $364B.

Trainium commitments reached $225B.

The chip business crossed a $20B run-rate.

But evidence is not cash.

FCF fell to $1.2B, and Amazon raised $53B of long-term debt.

That is the new Amazon debate.

The Foundry has answered back.

Now it has to pay for itself.

nikhs.substack.com/p/amazon-1q26-…

English