SquareCap

118 posts

BÖRSEN PÅ PLUS!! 🔥 Stockholmsbörsen rusar och återhämtar hela fallet på -2,8% som mest!! Nu åter på plus. De aktierna som stigit mest från dagslägsta är Boliden +6,3% Sandvik +5,6% och Atlas +4,8% #PrataPengar #Finanstwitter

Svenska

☕️ Jobbfredag!

Och ny chans att vinna en signerad DiTV-kopp, denna gång med ingen mindre än JACOB WALLENBERGS autograf.

Marknaden tror på 59 000 nya jobb, vad tror du?

Posta din gissning som en kommentar. Närmst vinner Wallenberg-koppen. #finanstwitter

Svenska

$ABB går verkligen som tåget i år! 🚂

Över 18% redan! 🚀

Fint som aktieägare i Investor 💼

Frågan är om man inte ska ta in bolaget i väskan vid nästa dipp, om den nu ens kommer? 🤔

#finanstwitter #FinTwitt

Svenska

@ELiInvest_ Alla dessa ”experter” i kommentarsfältet är just dem som har sämre avkastning än Investor och bara egentligen borde hålla.

Svenska

Handlar ju inte aktivt men allt i denna grafen skriker skala av Investor B eller vad säger ni andra experter?

Svenska

@vintermust Var det inte du som sålde allt i augusti och har missat all avkastning?

Svenska

@aleabitoreddit @DeepValueBagger You are wrong on $apld, $CRWV have already exercised their option so $11B locken in, then you didn’t mention that they have a new $5B lease with an unnamned investment grade hyperscaler. So they have $16B in revenue locked in.

English

Neocloud Ecosystem Cheat Sheet Part 1/2:

Bullet Point Positive vs. Negatives.

Full List by Marketcap:

$CRWV ($66.2B)

$NBIS ($32.85B)

$IREN ($16.52B)

$APLD ($9.69B)

$RIOT ($7.34B)

$CIFR ($7.3B)

$WULF ($6.36B)

$HUT($5.39B)

$CLSK ($5.01B)

$HIVE ($1.74B CAD)

$WYFI ($1.29B)

$WLAC($600m IPO)

$DGXX ($393M CAD)

$SLNH ($281.9M)

_

Summary

When comparing, a major source of alpha generation currently lies in the megawatt valuation arbitrage, which involves converting low-multiple Bitcoin power capacity into high-multiple AI hosting capacity.

The second major alpha is margin generation, which involves being vertically integrated from the bottom up from GPU orchestration to software.

Coreweave ( $CRWV ) - $66.2B Marketcap

🍏Positives

________________

- Sector leader by scale: quarterly revenue of $1.21B (+206.75% YoY) and EBITDA of $607.69M; on pace for $5B+ ARR in 2025.

- $30B+ backlog, anchored by:

- $14B Meta deal,

- OpenAI

- $6.3B NVIDIA GPU backstop agreement,

- growng Gov contracts via CRWV Federal .

- Expansion into U.S. government infrastructure is a major long-term moat if backstopped by federal workloads.

- NVIDIA partnership ensures utilization floor; de-risks GPU oversupply.

- Positioned as hyperscaler alternative with Tier 1 clients and national buildout footprint.

Negatives

________________

- Aggressive capex: Q3 spend of $2.9–3.4B, with 2025 full-year guidance of $20–23B.

- High-cost debt structure: Over $1B in projected annual interest, versus competors using low- or zero-interest convertible notes.

- Q2 GAAP net loss of $291M, signaling limited profitability despite scale.

- Execution risk remains high: e.g., failed $9B Core Scientific acquisition due to shareholder rejection.

- Competitors like Nebius are closing the full-stack gap, weakening CoreWeave's software moat.

Nebius ( $NBIS ) - $32.85B MarketCap

🍏Positives

________________

- $17.4B Microsoft deal for full-stack AI infrastructure (possibly rising to $19.4B).

- Active include many enterprises such as MSFT, Shopify, Accenture, governments, and AI startups.

- 71%+ gross margins on AI infra segment; profitable at the EBITDA level.

- 1 GW+ powr secured, targeting dense GPU deployments across new sites.

- Fully integrated software+hardware stack, which increases opex and is a moat.

- $10B+ in assets, from $5.8B+ cash, ownership of companies like Clickhouse that powers Anthropic, Meta, and others growing rapidly.

Negatives

________________

- Execution risks around full-stack delivery and latency SLAs could derail rollout.

- Microsoft is the primary anchor on forward revenue extreme contract dependency (high concentration risk projected AI revenue)

- 71% gross margin figure not representative of forward revenue or execution at scale and could lower to a more conservative 50-65% number.

$IREN - $16.52B marketcap

🍏Positives

________________

- 2.91 GW power secured, diversified across North America, and expanding more than 3GW in renewable power capacity.

- Full control over power, land, and data center construction = vertical efficiency and higher margin control compare to other bare metal.

- Targets customers (e.g., AI labs, hyperscalers) who might bring their own Type-1 orchestration and prefer bare-metal control.

- Historically the most efficient and profitable large-scale BTC miner and better positioned to handle rising GPU power/cooling requirements in B100/B200 generations for AI cloud pivot.

- Targeting an ARR of over $500 million by the first quarter of 2026 by buildouting out a fleet of 23,000 NVIDIA B200/B300 + AMD MI350X GPUs.

Downsides

________________

- No well-known enteprsie/hyperscaler contract visibility and limited disclosed large SLA deals yet

- Not a full-stack provider; acts as Tier-1 (shell/colocation) = lower margin and tenant risk and illustrative GPU target. Meaning it is unable to capture the highest-margin revenues associated with integrated, proprietary full-stack cloud

- Quoted 92% margins excludes expense recognition, and with D&A and would be much lower at scale.

- The substantial capital expenditure required for the large-scale GPU purchase risks negative returns if future utilization rates fail to meet expectations

$APLD

🍏Positives

________________

- $5B Macquarie financing facility, with first draw building 400MW AI campus.

- Tenant: CoreWeave fully leasing Polaris Forge 1 (400MW), scalable to 1GW.

- Proprietary waterless liquid cooling optimized for dense AI workloads

- Capex-light via preferred equity.

- AI-first buildout focused on latency, fiber, and power pairing in North Dakota.

Downsides

________________

- Large-scale buildout depends on continued draws from Macquarie’s $5B facility.

- 400MW CoreWeave lease is all-or-nothing; no clarity on tenant diversity.

- Execution risk at Polaris Forge: weather, zoning, grid integration delays.

- Exposed to single-tenant concentration and private-market GPU pricing dynamics.

$RIOT

🍏Positives

________________

- 600MW idle capacity in Corsicana, TX under AI redeployment review.

- Gigawatt-scale infrastructure in place, ready for rapid pivot.

- Leverages one of the lowest power costs in the U.S. (ERCOT access).

- TTM Gross Margin of nearly 60% as of Q2 2025, primarily derived from its core mining business. The successful implementation of this contract gives more confidence in converting additional existing mining sites into high-multiple HPC capacity.

Negatives

________________

- AI pivot is purely exploratory; no firm buildout announced.

- 600MW idle capacity = opportunity, but also dead capital for now.

- Canceling mining expansion (8.3 EH/s) may weaken near-term revenues.

- Needs permits, fiber, GPU supply, and anchor tenant before AI rollout can begin.

$CIFR

🍏Positives

________________

- 10-year, $3B+ computing 168MW agreement with Fluidstack + $GOOGL

- Agreement is substantially de-risked by a $1.4 billion commitment from Google to backstop the Fluidstack lease

- High-margin, low-risk hosting model with leased facilities.

Negatives

________________

- Fluidstack deal is 10-year but fixed-price, limiting upside if GPU rental rates increase.

- $1.3B convertible debt adds dilution risk if equity markets weaken.

- Site buildouts dependent on few customers, very high fill and utilization risk.

_

Since the data center sector is so nuanced and broad thought it would be helpful if I wrote created a full TLDR list for newcomers to see the tradeoffs of each approach.

I'll probably go back and add more stuff to $CIFR and $APLD and others in one final post since it didn't get enough justice.

I just didn't realize how much time this took to write up + please correct me if any figures are off lol.

Also would save me time if people helped fill out the rest lol so would appreciate it too for 2/2.

~~~ Help with the Crowdsourcing ~~~

Serenity@aleabitoreddit

The Neocloud thesis aged well. 1 month later: $CRWV 120.34 → 135.64 (+12.7%) $NBIS 107.70 → 126.49 (+17.5%) $WULF 10.63 → 13.69 (+28.8%) $IREN 41.68 → 64.69 (+55.2%) $CIFR 11.47 → 20.70 (+80.4%) $BITF 2.54 → 4.51 (+77.6%) $WYFI 22.83 → 36.52 (+59.9%) $GRRR 19.90 → 16.95 (−14.8%) $SLNH 2.75 → 2.81 (+2.2%) $RIOT 17.69 → 23.01 (+30.1%) $MARA 16.13 → 19.61 (+21.6%) $CLSK 12.96 → 20.21 (+56.0%) $HUT 33.16 → 49.95 (+50.6%) This is only the beginning of the largest AI data center buildout in history and everyone on finx is still early. I'm very bullish on the Neocloud sector across the board, but personally have concentration in $NBIS due to the highest asymmetrical return.

English

@livetefterfire Vad spelar utdelningen för roll om aktien fortsätter dumpas?

Svenska

Tja.. EVO:s rapport var ju ingen höjdare direkt🙈 De tjänade dock 1,25 euro/aktie i kvartalet så utdelningen till våren borde vara säker = jag fortsätter hålla och klippa kupong.

Svenska

@RikLangsamt Du borde byta namn till Fattig Snabbt med den portföljen

Svenska

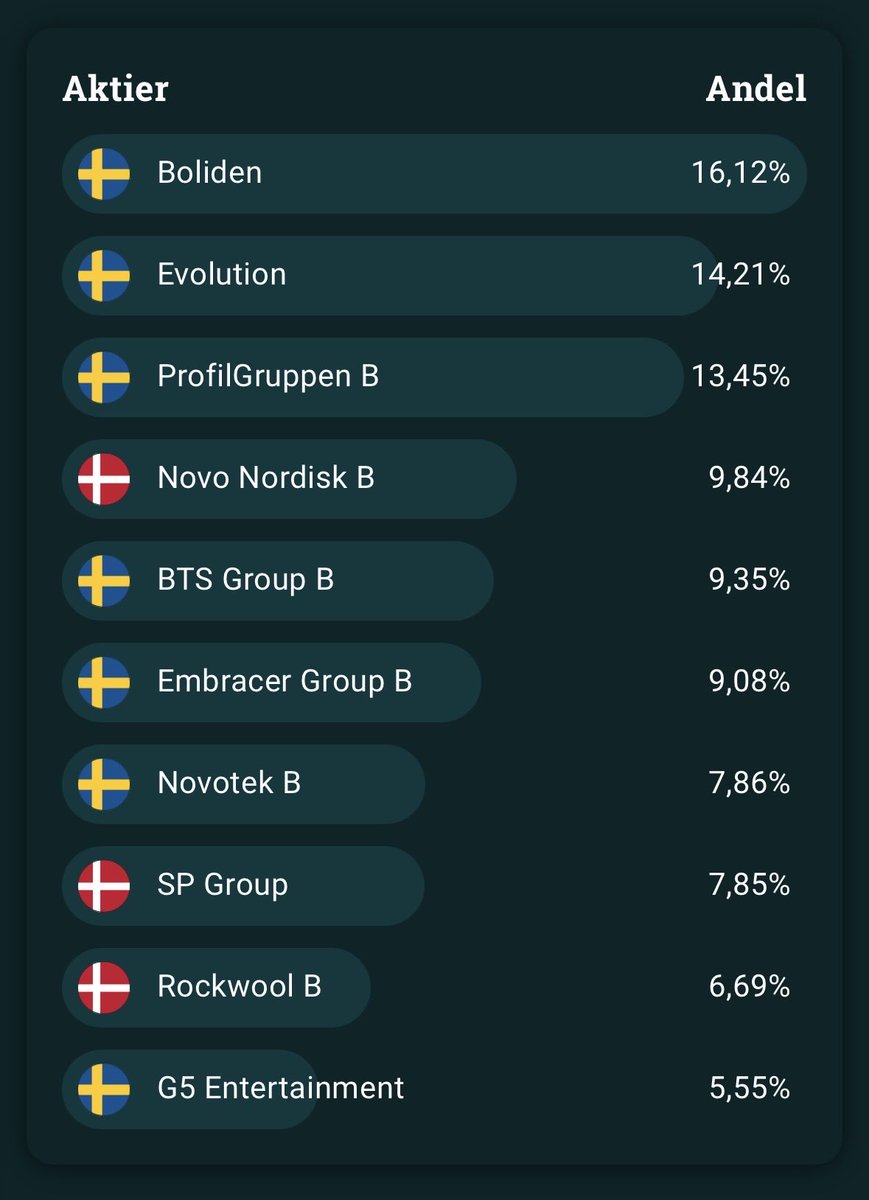

Screener-portföljen💼

Uppdatering #31

För första gången någonting så sker inga affärer. Månaden slutar på -1,87% men med betydligt större rörelser i många aktier. Boliden +19%, EVO -12%, Profilgruppen -13,5%, Novo -10%.

YTD: -1,31%

Sedan start: +2,05%

Sälj❌

-

Köp✅

-

Svenska

@borspicker Förstår inte folk som antingen håller kvar eller t.o.m. köper mer, finns mer avkastning att hämta på annat håll och finns lixom inget som kommer att dra upp kursen så mycket att det är värt att hålla $evo

Svenska

@SkugganIV Att värderingen är låg har evo ägare sagt senaste 5 åren, finns inget som kommer lyfta kursen så pass att man får bra avkastning jämfört med något annat. Sälj och köp något annat är mitt råd

Svenska

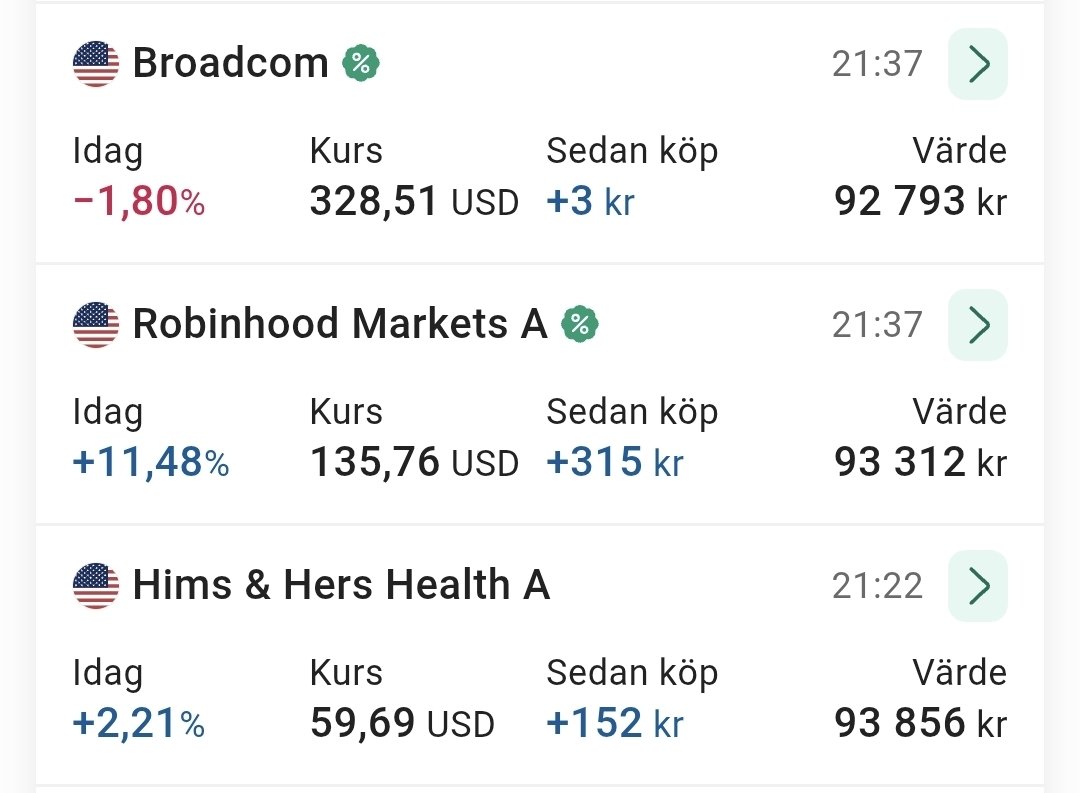

@finanskristen Yes det gör jag, men är mest bull APLD, finns en anledning till varför både Nvidia och Coreweave äger aktier i APLD:)

Svenska

@finanskristen Jo, jag med egentligen, men detta är ett undantag, har så otroligt mycket tillväxt framför sig, dem signade en deal med Coreweave på 11B dollar 15 år framåt och har flera till deals på gång

Svenska

@squarecapital3 Brukar undvika företag som inte går med vinst, men det kanske jag ska sluta med.

Svenska

@30M_Innan30 Hur delar du på svenskt och utländskt? Allt på kf eller separat?

Svenska

@avanzabank @skaaltamigfan Vi är ju inte dumma @avanzabank. Ni mjölkar oss på pengar. Men ni kommer inse att ni förlorar mer pengar på att kunderna lämnar pga detta.

Svenska

@skaaltamigfan I dagsläget är det möjligt att byta courtageklass en gång per dag. Förstår att det inte är optimalt just vid den situationen du beskriver. Vi vet om önskemålet och om det sker förändringar på den fronten får vi låten framtiden utvisa.

Svenska

Private Banking-revolutionen är nära 👀 Just nu har vi en grupp med 10 starka betatestare av vår nya diskretionära förvaltning. En helt digital tjänst som rullas ut till alla våra Private Banking-kunder när tiden är inne 😎#finanstwitter

Svenska