Tgal 🥛

246 posts

Tgal 🥛

@t_gal11

GM of @MilkRoad where 300+ subs get smarter about investing.

Katılım Aralık 2020

256 Takip Edilen196 Takipçiler

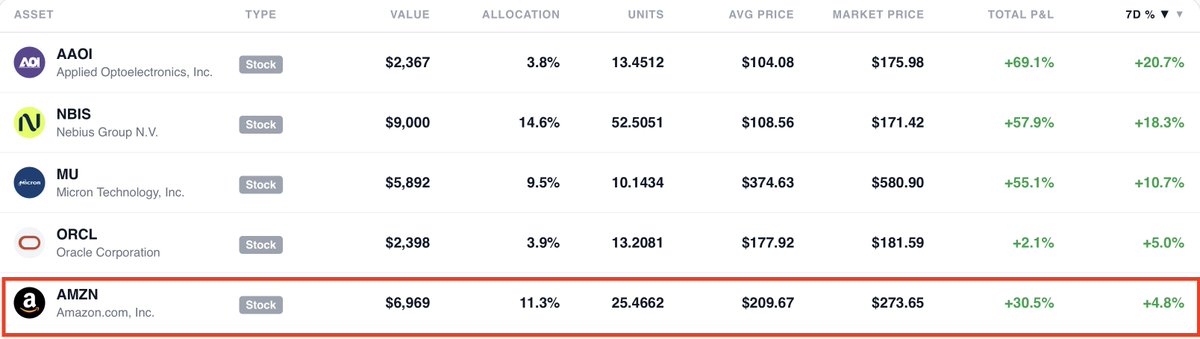

Amazon is still the most underrated stock in the Mag 7 and if you're sleeping on it, you're about to miss the next AWS moment (Save this).

Every few years, Amazon does something it has only done a handful of times in its history, it takes a capability it built for itself and opens it up to the world.

The first time it did this, it created AWS, a business now running at a $142 billion annual revenue rate, growing at 24% year over year, printing 35% operating margins, and projected by CEO Andy Jassy to hit $600 billion in annual revenue by 2036.

What started as Amazon's internal cloud became the backbone of the internet and today, it's doing it again, this time with logistics.

Amazon just launched Amazon Supply Chain Services opening its full freight, distribution, fulfillment, and parcel shipping network to any business on the planet.

And the early signups are P&G, 3M, Lands' End, and American Eagle Outfitters.

These are some of the most operationally sophisticated companies in the world, and they're handing Amazon the keys to their supply chains.

The proof of concept was already there.

Since 2006, independent sellers shipped more than 80 billion units through Fulfillment by Amazon and sellers using Amazon's end to end logistics see nearly 20% higher sales.

Amazon took that model, battle tested it across hundreds of thousands of businesses, and now it's offering it to the entire $1 trillion global 3PL market, a market projected to hit $2.1 trillion by 2032.

Now here's why the stock is still underrated, Amazon is trading at a

P/E of 32.7x on a market cap of $2.9T.

That multiple barely prices in what's already in the building, AWS re accelerating, advertising crossing $50 billion plus and gross margins expanding to 50% in 2025 and this doesn't price in ASCS at all.

This is a company that just opened a new enterprise logistics revenue line targeting a trillion dollar market, and the market is treating it like nothing happened.

The financials back the bull case hard, FY2025 revenue hit $716.9B , up

12.4% year over year. Q1 2026 came in at $181.5B in revenue with EPS of

$2.78, 74% above the consensus estimate.

Milk Road now see $810B in revenue for FY2026 and the earnings machine is not slowing down.

The capex spend $200B in 2026, looks scary on paper but it's the same bet Bezos made with AWS in the early 2000s. Build infrastructure nobody else can afford to replicate, then monetize it for decades.

Every dollar Amazon is spending on robotics, AI forecasting, and logistics density is making the same network it just opened up to enterprises cheaper and faster to operate.

That's operating leverage compounding in real time and this is exactly why Milk Road analysts remain bullish on Amazon.

AWS is accelerating into the AI supercycle and sitting on $244 billion in contracted backlog, ASCS is a multi year enterprise revenue unlock that is just getting started.

We've already started building a significant position and is up on it massively.

If you want to see exactly how we're sizing it, what we're buying, and our full thesis, come join us.

Link in below!

English

@MilkRoadAI This is why my money is on Vincent to be the Milk Road analyst of the summer 😉

English

This is Leopold Aschenbrenner and this clip is from before the hedge fund, before the 13F filings, he raised $225 million and turned it into over $5.5 billion.

This is the thesis in its raw form, his point is simple, look at the jump from GPT-2 to GPT-4 (Save this).

GPT 2 was 2019 and it could sort of count to five before getting confused.

GPT 4 arrived just 3–4 years later scoring in the 90th percentile on exams like the bar, LSAT, and GRE, while solving complex math and playing chess.

That’s not incremental progress but rather a leap into an entirely new category of intelligence in less time than a college degree and his conclusion, play that forward.

Just a few more jumps like that, on a fairly short time horizon, basically this decade and we're going to hit extremely, extremely powerful systems.

Now here's where it gets interesting. Leopold didn't just say this but he put real money behind every implication of it.

His thesis was, if AI scales this fast, it will need compute at a scale the world has never built before.

The bottleneck won't be the algorithms bur rather the physical infrastructure like power, data centers and networking.

So while everyone else was buying Nvidia, Leopold was buying what Nvidia depends on.

Bloom Energy, CoreWeave, Lumentum, Core Scientific, Iren, Applied Digital, even Intel calls all ripping as AI turns power, compute, and chips into the real bottlenecks.

The whole fund is just the GPT-2 to GPT-4 chart, extended forward, and then asked, what does the world need to exist for that to happen?

He answered that question, then bought it.

Milk Road PRO is doing the same, come join us for our entire thesis Link below.

Milk Road AI@MilkRoadAI

Leopold Aschenbrenner, the 24 year old who wrote a 165 page AGI manifesto, got it right on the money, and turned it into a $5.5 billion hedge fund. And he's identifying the single most important milestone to watch for in all of AI. The question is can AI automate AI research itself? Here's why that question matters so much. Right now, a few thousand human researchers at the frontier labs are driving all the progress. They design experiments, write papers, propose architectural improvements, build the next generation of models and it's an incredibly small workforce doing incredibly high-leverage work. If an AI system can do that job even partially, the feedback loop changes completely. The AI makes algorithmic improvements, which produces more powerful AI, which makes better improvements, faster. You go from linear progress to compounding returns and a decade of research could compress into a year. Aschenbrenner says there's a "pretty reasonable chance" this happens within five years. He's not alone, Anthropic says they're on track to fully automate AI R&D as soon as early 2027. OpenAI has publicly targeted a fully autonomous AI researcher by March 2028 and Sam Altman has said a research intern level AI will exist before the end of this year. If he's right, the next few years won't look like the last few years but they'll look like nothing we've seen before. The future is bright!

English

This is WILD!

Bloom Energy just reported Q1 2026 earnings and the stock is up nearly 10% in after hours right now.

And the man with the most to gain is a 24 year old who got fired from OpenAI.

Leopold Aschenbrenner ran safety research at OpenAI until the company let him go.

He then wrote a 165-page essay arguing that AGI was arriving faster than any investor understood and that the people who would win were not the ones who owned the best AI model.

They were the ones who owned the electricity and that thesis became a hedge fund called Situational Awareness LP and he turned $225 million into $5.5 billion in under twelve months.

His largest single position is an $875 million stake in Bloom Energy and with tonight's 10% move, that position is now worth more than $2.2 billion and still climbing.

The catalyst is obvious in hindsight but almost no one saw it coming.

Bloom announced a 2.8 gigawatt fuel cell deal with Oracle, the largest on site power commitment in the history of enterprise computing.

Bloom delivered in 55 days against a 90-day commitment, Oracle gave Bloom a warrant for 3.53 million shares and the total backlog is now estimated at $20 billion.

His other major positions follow the same electricity-first logic.

$700 million in CoreWeave and a massive short on Infosys betting that AI coding agents destroy the outsourced IT business.

Intel call options printing multiples on a 53% run and a 10% activist stake in Core Scientific, a Bitcoin miner converting its power infrastructure into AI data center hosting.

The entire Wall Street AI trade was piled into model companies and chip companies.

Aschenbrenner looked at the same thesis and concluded the real bottleneck was whether the power grid could deliver enough electricity to run the models.

He was right, and the returns are public record.

One of our analysts at Milk Road called this exact play two months ago, took a massive position in Bloom Energy, and it is already up over 55%.

If you want access to the full thesis and what we are watching right now, go PRO. Link below.

English

Chamath Palihapitiya, one of the most connected investors in tech and his warning is the clearest framing of the AI compute crisis anyone has put into words.

"It is a five alarm fire for them. They need to have land, power, shell."

He's talking about Anthropic and OpenAI and the threat he's describing is called the Friendster effect.

Friendster was the dominant social network before MySpace and Facebook and it didn't lose because it had a bad product but rather it lost because it couldn't keep the site up.

Demand outpaced infrastructure, the experience degraded, and users left for one that actually worked.

Chamath's argument is that OpenAI and Anthropic are approaching exactly that moment.

The numbers are already showing it, Anthropic is growing so fast that it had to cut Claude's thinking depth during peak hours, cap agentic sessions, and test removing Claude Code from its $20 plan entirely.

GitHub Copilot paused new signups, paying enterprise customers are hitting usage walls they've never seen before.

Dario Amodei himself admitted there is "no hedge on earth" against the risk of over-purchasing compute meaning he's deliberately staying lean on capacity, even as the demand wall approaches.

The core problem is structural, OpenAI and Anthropic grew up renting capacity from hyperscalers AWS, Azure, Google Cloud.

That was fine when they were small but now they're so large that dependency is a strategic liability.

Every token they sell runs on someone else's infrastructure and every capacity decision belongs to someone else.

And when demand spikes faster than anyone planned, there's nothing they can do in real time except throttle.

Building your own infrastructure takes 18 to 24 months minimum, you need to acquire land, secure power, construct shell and none of that happens fast.

That's why Google's $40 billion commitment to Anthropic this week is about more than just money but rather about securing the land, power, and infrastructure that Anthropic needs to not become Friendster.

Whoever controls the compute controls the frontier and right now, the AI labs with the best products are the most dependent on infrastructure they don't own.

Milk Road AI@MilkRoadAI

Alphabet just committed up to $40 billion more to Anthropic and pledged at least 5 gigawatts of computing power to back it. To understand why Google keeps writing bigger and bigger checks, you have to understand Anthropic's compute crisis. Anthropic's revenue ran at $9 billion at the end of 2025. By March 2026 it was $30 billion, more than tripling in a single quarter. Over 1,000 enterprise customers are now spending more than $1 million a year on Claude, a number that doubled in under two months and Anthropic is capturing 73% of all first-time enterprise AI spending. The problem is the growth is so fast, Anthropic can't physically serve all of it. Both Anthropic and OpenAI are currently turning away business because they don't have enough compute to fulfill demand. OpenAI's CFO said she spends significant time trying to source last-minute GPU capacity and that without it, there is no revenue. At Anthropic, paying Claude subscribers started hitting session caps during peak hours earlier this month, a public acknowledgment that infrastructure is failing to keep pace with demand. Dario Amodei knows this as he stated that Anthropic is compute-constrained, and that compute is the primary bottleneck for both model development and deployment. Expecting more Anthropic deals to be made over the next few months.

English

Meta just signed a deal with Amazon to deploy tens of millions of AWS Graviton CPU cores into its AI infrastructure and Andy Jassy himself called it out as one of the most important signals in tech right now.

"Agentic AI is becoming almost as big a CPU story as a GPU story."

There are two reasons CPUs have become critical at scale.

The first is reinforcement learning, you don't just dump data into a model and train it anymore.

You put it in an environment, give it tasks, let it try things, score its outputs, and train on what worked and those environments run on CPUs, not GPUs.

The more capable AI gets, the more complex those scoring environments become and all of it runs on CPU.

The second is deployment, once a model is trained, its outputs don't go straight from a GPU to a human.

They route through apps, APIs, and agent workflows, all CPU bound on the backend.

That's exactly what this Meta-AWS deal confirms.

Graviton5 runs 192 Arm Neoverse V3 cores on 3nm TSMC, with a cache 5x larger than the prior generation and 33% lower inter-core latency, purpose-built for agentic workloads at this scale.

The demand signal is staggering, Andy Jassy revealed two large customers tried to buy out Amazon's entire 2026 Graviton capacity and he had to turn them down.

Amazon's chip business is running at a $20 billion annual revenue rate, growing triple digits and Jassy says if sold standalone, it's closer to a $50 billion run rate.

Everyone was watching GPUs but our analysts at Milk Road saw this coming.

Two of our top Pro holdings are AMD and Amazon, both sitting directly in the path of this CPU buildout before today's headlines.

If you want to see what we're buying next, come join us.

Link below.

Milk Road AI@MilkRoadAI

Intel just reported Q1 2026 earnings and the stock is up 12% after hours and AMD is running alongside it, up nearly $10. This is the exact opposite of what Wall Street expected going in. Intel entered today's report with one of the most skeptical setups in the semiconductor space. The stock was already up 80% year to date on AI hype but analysts were forecasting Q1 revenue down ~2% year over year to around $12.3B, near zero EPS, and gross margins barely above 34%. Six of eight analysts covering Intel had neutral ratings, and the mean price target was below where the stock was already trading. What Intel delivered was better than that and in a market where the bar was set this low, even a modest beat on revenue and any early signal of improvement in the foundry business is enough to send the stock flying. But here is what the beat is actually telling you about CPU demand. Server CPU shipments in the data center are accelerating driven directly by AI infrastructure buildout. Hyperscalers are building at a pace that requires not just GPUs, but enormous volumes of x86 CPUs to run the orchestration, inference serving, and cloud workloads that sit around every GPU cluster. Every rack that goes into a data center needs dozens of server CPUs and that demand environment is what Intel just confirmed and AMD sells into the exact same market. Lisa Su laid it out in AMD's own presentation months ago, training compute is scaling 4x per year while inference tokens grew 100x in the last two years alone. When Intel confirms that CPU demand in the data center is stronger than feared, AMD doesn't just benefit from the sentiment lift but rather benefits from the same structural demand. And unlike Intel, AMD doesn't have a $2.5 billion foundry operating loss dragging on its margins every quarter. AMD's data center revenue hit a record $5.38 billion in Q4 2025, up 39% year over year and the full year came in at $10.27 billion, up 34%. Our analysts at Milk Road saw this coming. They took massive positions in AMD months ago before today's move, before the Intel print, before the broader market started connecting the dots between CPU demand and the AI infrastructure buildout. If you want to see exactly what they're buying next and why, you can try Milk Road Pro for $1. Link below!

English

Intel just reported Q1 2026 earnings and the stock is up 12% after hours and AMD is running alongside it, up nearly $10.

This is the exact opposite of what Wall Street expected going in.

Intel entered today's report with one of the most skeptical setups in the semiconductor space.

The stock was already up 80% year to date on AI hype but analysts were forecasting Q1 revenue down ~2% year over year to around $12.3B, near zero EPS, and gross margins barely above 34%.

Six of eight analysts covering Intel had neutral ratings, and the mean price target was below where the stock was already trading.

What Intel delivered was better than that and in a market where the bar was set this low, even a modest beat on revenue and any early signal of improvement in the foundry business is enough to send the stock flying.

But here is what the beat is actually telling you about CPU demand.

Server CPU shipments in the data center are accelerating driven directly by AI infrastructure buildout.

Hyperscalers are building at a pace that requires not just GPUs, but enormous volumes of x86 CPUs to run the orchestration, inference serving, and cloud workloads that sit around every GPU cluster.

Every rack that goes into a data center needs dozens of server CPUs and that demand environment is what Intel just confirmed and AMD sells into the exact same market.

Lisa Su laid it out in AMD's own presentation months ago, training compute is scaling 4x per year while inference tokens grew 100x in the last two years alone.

When Intel confirms that CPU demand in the data center is stronger than feared, AMD doesn't just benefit from the sentiment lift but rather benefits from the same structural demand.

And unlike Intel, AMD doesn't have a $2.5 billion foundry operating loss dragging on its margins every quarter.

AMD's data center revenue hit a record $5.38 billion in Q4 2025, up 39% year over year and the full year came in at $10.27 billion, up 34%.

Our analysts at Milk Road saw this coming.

They took massive positions in AMD months ago before today's move, before the Intel print, before the broader market started connecting the dots between CPU demand and the AI infrastructure buildout.

If you want to see exactly what they're buying next and why, you can try Milk Road Pro for $1.

Link below!

Milk Road AI@MilkRoadAI

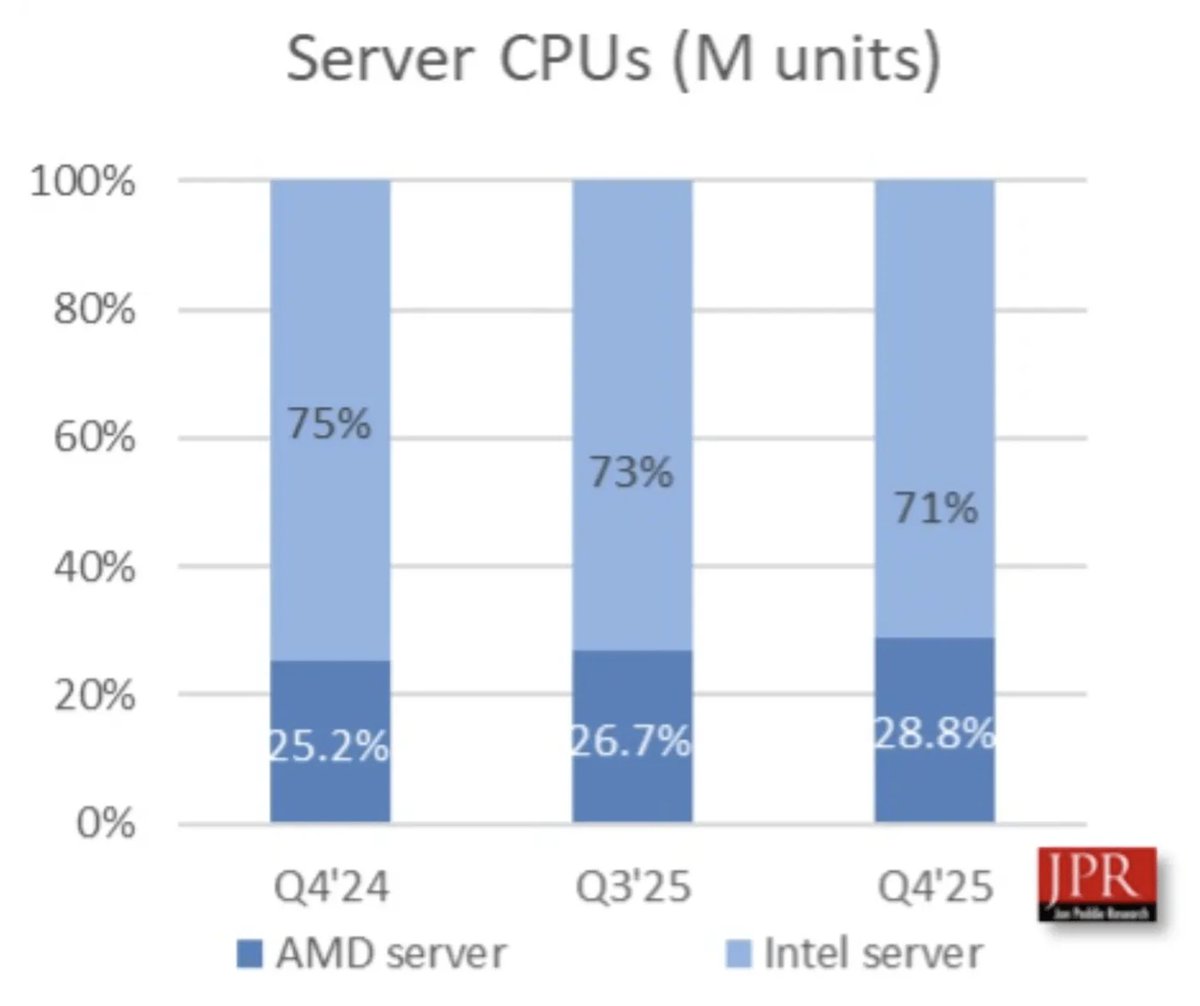

Everyone is buying Nvidia but we bought AMD (Save this). Nvidia owns the GPU but AMD owns what's breaking next, the CPU. The entire AI industry spent 3 years building infrastructure around the wrong chip and they just figured that out. Intel got caught flat footed, admitted it on an earnings call and started cannibalizing its own business to keep up. AMD has been quietly eating their lunch the whole time and we took a position before most people connected the dots. For 3 years the AI infrastructure story was perfectly simple. GPUs are king, Nvidia dominates, buy Blackwell but hen agentic AI broke everything. An AI agent doesn't just answer questions. It browses the web, runs code, checks calendars, calls APIs, manages memory, and coordinates with other agents in parallel often without you touching anything. Every one of those steps, the tool calls, the memory lookups, the routing, the orchestration runs on the CPU. CPU workload went from 5-10% of total AI compute to roughly 50% almost overnight and the whole industry built for the wrong chip. Jensen Huang said it out loud at GTC 2026 and it made everyone in the room do a double-take. Agentic AI consumes one million times more tokens than a standard chatbot prompt. Global AI token usage doubled from 6.4 trillion to 13 trillion tokens in just six weeks. IDC projects enterprise AI agent usage grows tenfold by 2027. Agent-related API call loads are rising a thousandfold. Intel CFO David Zinsner stepped onto the Q4 earnings call and admitted publicly, on the record, that server CPU demand had caught them off guard. The company that has manufactured CPUs for 50 years. Built around server processors. Caught off guard by demand for its own core product. The shortage is real and it's getting worse across the board. In China, wait times for server CPUs have stretched to six months. Standard enterprise chip delivery timelines are hitting 8-10 weeks. Server CPU prices in China are up over 10% and climbing. Andy Jassy disclosed in his shareholder letter that two large AWS customers asked to buy all of its Graviton CPU capacity for 2026. AWS had to say no. Atlassian went from 5% to over 30% Graviton adoption in a single year because the cost savings were too obvious to ignore. AWS added 50% of all new CPU capacity over the past two years on ARM, surpassing Intel and AMD combined in new capacity additions. When Intel fumbles, AMD picks up the ball. Server CPU market share: 3% in 2017. 25.2% in Q4 2024. 26.7% in Q3 2025. 28.8% in Q4 2025. In Q4 alone, AMD grew server CPU shipments at more than triple the seasonal average. Intel still holds 71% of the market but the direction of travel is unmistakable. Every quarter Intel struggles with supply, AMD gains ground it historically does not give back. And AMD isn't standing still , they're locking in hyperscaler relationships and multi-year infrastructure decisions with every new win. Here's what most people are missing because Turin barely launched. AMD's 5th Gen EPYC only came out in late 2024 and just crossed 50% of AMD's server revenues for the first time in Q4 2025. Semiconductor cycles take 6-8 quarters to fully ramp. AMD is in quarter 2. The hyperscalers adopting Turin right now are making multi-year infrastructure decisions every win over the next 4 quarters is sticky, compounding revenue that builds a moat competitors will spend years and billions trying to replicate. And while most chip companies have to pick a side, AMD doesn't. EPYC is taking CPU share from Intel while MI300X competes with Nvidia H100s for AI training and inference. Morgan Stanley estimates $3 trillion in data center construction flows through the global economy by 2028. McKinsey puts total AI infrastructure spending approaching $7 trillion by 2030. AMD captures budget from two completely separate line items simultaneously. In late 2024, Intel and AMD did something that tells you everything about where this is heading. They formed the x86 Ecosystem Advisory Group, a formal defensive alliance with Microsoft, Alphabet, Meta, and Broadcom on the founding board. Two old rivals joining hands because ARM is winning. Half of all new compute capacity shipped to hyperscalers in 2025 was ARM-based. Arm Holdings just built its first-ever chip, the AGI CPU delivering more than double the performance per rack versus x86 systems. First customers, OpenAI, Meta, SAP, Cloudflare. CEO Rene Haas has set a $25B revenue target for 2031 and then Nvidia unveiled the Vera CPU at GTC 2026 now selling one CPU for every two GPUs in Blackwell NVL72 configurations. When the GPU king enters the CPU market, you know the shift is real. The scorecard for who wins this. AMD is the clearest near-term winner, gaining server CPU share during Intel's supply crunch with EPYC still early in its ramp cycle and MI300X competing on the GPU side simultaneously. Milk Road Pro saw this early. Turin just starting to ramp. Intel clearly on the back foot, double exposure to both CPU and GPU spend. We took a huge position months ago and that position is already up over 35% in the past 2 months. Our analysts are finding the next plays before they make headlines. If you want access to the full thesis and what we are watching right now, go PRO just for a $1. Link below!

English

Everyone is buying Nvidia but we bought AMD (Save this).

Nvidia owns the GPU but AMD owns what's breaking next, the CPU. The entire AI industry spent 3 years building infrastructure around the wrong chip and they just figured that out.

Intel got caught flat footed, admitted it on an earnings call and started cannibalizing its own business to keep up. AMD has been quietly eating their lunch the whole time and we took a position before most people connected the dots.

For 3 years the AI infrastructure story was perfectly simple. GPUs are king, Nvidia dominates, buy Blackwell but hen agentic AI broke everything. An AI agent doesn't just answer questions. It browses the web, runs code, checks calendars, calls APIs, manages memory, and coordinates with other agents in parallel often without you touching anything.

Every one of those steps, the tool calls, the memory lookups, the routing, the orchestration runs on the CPU. CPU workload went from 5-10% of total AI compute to roughly 50% almost overnight and the whole industry built for the wrong chip.

Jensen Huang said it out loud at GTC 2026 and it made everyone in the room do a double-take. Agentic AI consumes one million times more tokens than a standard chatbot prompt. Global AI token usage doubled from 6.4 trillion to 13 trillion tokens in just six weeks. IDC projects enterprise AI agent usage grows tenfold by 2027. Agent-related API call loads are rising a thousandfold.

Intel CFO David Zinsner stepped onto the Q4 earnings call and admitted publicly, on the record, that server CPU demand had caught them off guard. The company that has manufactured CPUs for 50 years. Built around server processors. Caught off guard by demand for its own core product.

The shortage is real and it's getting worse across the board. In China, wait times for server CPUs have stretched to six months. Standard enterprise chip delivery timelines are hitting 8-10 weeks. Server CPU prices in China are up over 10% and climbing.

Andy Jassy disclosed in his shareholder letter that two large AWS customers asked to buy all of its Graviton CPU capacity for 2026. AWS had to say no. Atlassian went from 5% to over 30% Graviton adoption in a single year because the cost savings were too obvious to ignore. AWS added 50% of all new CPU capacity over the past two years on ARM, surpassing Intel and AMD combined in new capacity additions.

When Intel fumbles, AMD picks up the ball. Server CPU market share: 3% in 2017. 25.2% in Q4 2024. 26.7% in Q3 2025. 28.8% in Q4 2025. In Q4 alone, AMD grew server CPU shipments at more than triple the seasonal average. Intel still holds 71% of the market but the direction of travel is unmistakable. Every quarter Intel struggles with supply, AMD gains ground it historically does not give back. And AMD isn't standing still , they're locking in hyperscaler relationships and multi-year infrastructure decisions with every new win.

Here's what most people are missing because Turin barely launched.

AMD's 5th Gen EPYC only came out in late 2024 and just crossed 50% of AMD's server revenues for the first time in Q4 2025. Semiconductor cycles take 6-8 quarters to fully ramp. AMD is in quarter 2. The hyperscalers adopting Turin right now are making multi-year infrastructure decisions every win over the next 4 quarters is sticky, compounding revenue that builds a moat competitors will spend years and billions trying to replicate.

And while most chip companies have to pick a side, AMD doesn't.

EPYC is taking CPU share from Intel while MI300X competes with Nvidia H100s for AI training and inference. Morgan Stanley estimates $3 trillion in data center construction flows through the global economy by 2028. McKinsey puts total AI infrastructure spending approaching $7 trillion by 2030. AMD captures budget from two completely separate line items simultaneously.

In late 2024, Intel and AMD did something that tells you everything about where this is heading. They formed the x86 Ecosystem Advisory Group, a formal defensive alliance with Microsoft, Alphabet, Meta, and Broadcom on the founding board. Two old rivals joining hands because ARM is winning.

Half of all new compute capacity shipped to hyperscalers in 2025 was ARM-based. Arm Holdings just built its first-ever chip, the AGI CPU delivering more than double the performance per rack versus x86 systems. First customers, OpenAI, Meta, SAP, Cloudflare. CEO Rene Haas has set a $25B revenue target for 2031 and then Nvidia unveiled the Vera CPU at GTC 2026 now selling one CPU for every two GPUs in Blackwell NVL72 configurations. When the GPU king enters the CPU market, you know the shift is real.

The scorecard for who wins this.

AMD is the clearest near-term winner, gaining server CPU share during Intel's supply crunch with EPYC still early in its ramp cycle and MI300X competing on the GPU side simultaneously.

Milk Road Pro saw this early. Turin just starting to ramp. Intel clearly on the back foot, double exposure to both CPU and GPU spend.

We took a huge position months ago and that position is already up over 35% in the past 2 months.

Our analysts are finding the next plays before they make headlines.

If you want access to the full thesis and what we are watching right now, go PRO just for a $1. Link below!

English

This account appears to be shadowbanned on X.

If you can see this post, please interact. Thank you!

English

$70,000,000,000 just vanished from crypto in a 45 min span.

If you have wallet notifications turned on and are freaking out right now - here's a step by step of what actually happened:

This sell off is the result of (more) bad news hitting a market already on edge.

Think of it like a Jenga tower that's been wobbling for weeks.

Someone finally pulled the wrong block.

$BTC had already dropped from recent highs to around $84k by January 30th.

Liquidity is paper thin right now, because it’s a Saturday (weekend trading is notorious for violent moves).

Take that, and add:

- Explosions at Iran's Bandar Abbas port.

- Trump warning about potential military action.

- A US government shutdown officially kicking in at midnight.

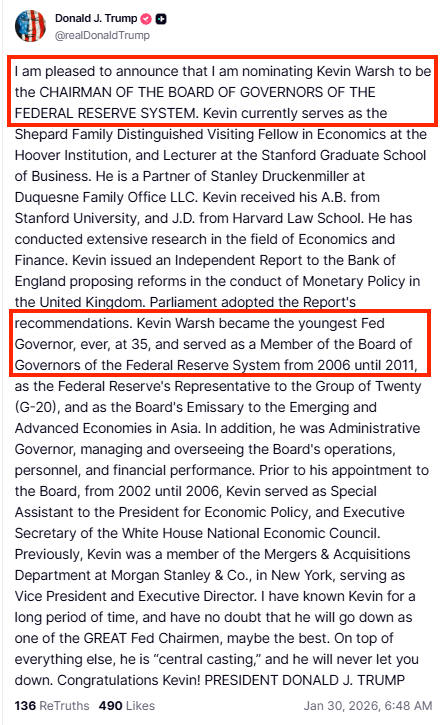

- Trump nominating Kevin Warsh to replace Powell at the Fed.

Risk-off mode activated.

$BTC broke below $81k, triggering a wall of liquidations….

$1.68B+ in positions got wiped, mostly longs…

Forced selling triggered more forced selling…

The crash fed itself.

The mistake people make: They think this was about one thing.

"It's the shutdown."

"It's Iran."

"It's the Fed."

No.

It was everything, all at once, into a market with no liquidity to absorb it.

The reality: Multiple converging pressures created this.

Geopolitical fear. Government dysfunction. Hawkish Fed signals. Extreme leverage getting flushed.

This was a broad risk-off event where crypto, being the highest-beta asset, got hit hardest.

Why you should care:

$BTC tested the $80-83k range, which represents critical support.

Analysts are watching $70-76k to see if it breaks.

But here's the thing…

When overcrowded positioning is getting flushed, it often sets up better entries later.

The fear index just hit its highest negative reading of 2026.

(Extreme fear typically marks bottoms).

What to watch now:

- How quickly the shutdown gets resolved.

- ETF flow direction in the coming days.

- Whether $80k holds as support.

- Any de-escalation in Middle East tensions.

- Fed commentary on rate path.

This is the kind of environment where fortunes are made and lost.

Stay nimble. Manage your risk.

And remember that 45-minute wipeouts are a feature of this market, not a bug.

Ash Crypto@AshCrypto

🚨BREAKING🚨 OVER $70,000,000,000 WIPED OUT FROM CRYPTO MARKET IN JUST 45 MINUTES.

English

The first U.S. bank failure of 2026 just happened on the same day silver had its worst crash in 46 years.

Illinois regulators just shut down Chicago’s Metropolitan Capital Bank & Trust ($261M) citing unsafe conditions and weak capital.

The FDIC stepped in immediately.

First Independence Bank in Detroit is assuming nearly all deposits and assets.

By itself, this might have gotten lost in the noise of the newsfeed…

But it happened alongside something far more dramatic.

Spot gold plunged over 12% to around $4,900 per ounce.

Silver collapsed more than 30% to about $85, its steepest single-day drop since 1979.

Here’s how it all went down:

President Trump nominated Kevin Warsh as Fed chair.

Warsh has historically been known as an inflation hawk.

Markets immediately priced in a stronger dollar policy because of this.

That sent the dollar ripping higher.

(The stronger the dollar becomes → the less need there is for safe haven assets like gold and silver).

Precious metals got crushed on the move, with margin calls cascading through leveraged positions.

As for the bank failure itself? For now, it looks contained.

Insured deposits are safe. The FDIC response was textbook.

But the timing is definitely creating narrative contagion online.

For precious metals holders, this is either a buying opportunity or the start of a larger unwind depending on your Fed policy read.

For $BTC and crypto, a (potentially) hawkish Fed chair nominee and dollar strength typically create short-term headwinds.

Watch Warsh's confirmation hearings closely. His policy signals will determine our direction here.

Dovishness = tailwinds for crypto.

Hawkishness = prepare for further price uncertainty.

Milk Road@MilkRoad

Precious metals are nuking (again)! $7 TRILLION has evaporated from precious metals in 36 hours. (That's the equivalent of the total crypto market going to zero - 2.5x over!) The entire precious metals complex is in free fall: GOLD crashed 13.6% below $4,900. SILVER collapsed 30% below $85. PLATINUM dropped 27.25% below $2,100. PALLADIUM fell 21.5% below $1,700. Stay safe out there folks: This much capital destruction can create ripple effects. Watch for contagion into other asset classes.

English

Amodei warned AI could wipe out 50% of entry-level jobs and spike unemployment to 20%.

Data shows we are watching the end of the entry-level job market in real time.

Save this video so you remember exactly when the shift started.

The Kobeissi Letter@KobeissiLetter

Recent Layoff Announcements: 1. US Government: 307,000 employees 2. UPS: 78,000 employees 3. Amazon: 30,000 employees 4. Intel: 25,000 employees 5. Nissan: 20,000 employees 6. Nestle: 16,000 employees 7. Microsoft: 15,000 employees 8. Bosch: 13,000 employees 9. Dell: 12,000 employees 10. Verizon: 13,000 employees 11. Accenture: 11,000 employees 12. Ford: 11,000 employees 13. Novo Nordisk: 9,000 employees 14. Microsoft: 7,000 employees 15 PwC: 5,600 employees 16. Salesforce: 4,000 employees 17. IBM: 2,700 employees 18. American Airlines: 2,700 employees 19. Paramount: 2,000 employees 20. Target: 1,800 employees 21. General Motors: 1,500 employees 22. Applied Materials: 1,444 employees 23. Kroger: 1,000 employees 24. Meta: 1,000 employees AI is officially replacing jobs at mass scale in the US. Where will all of these people go?

English

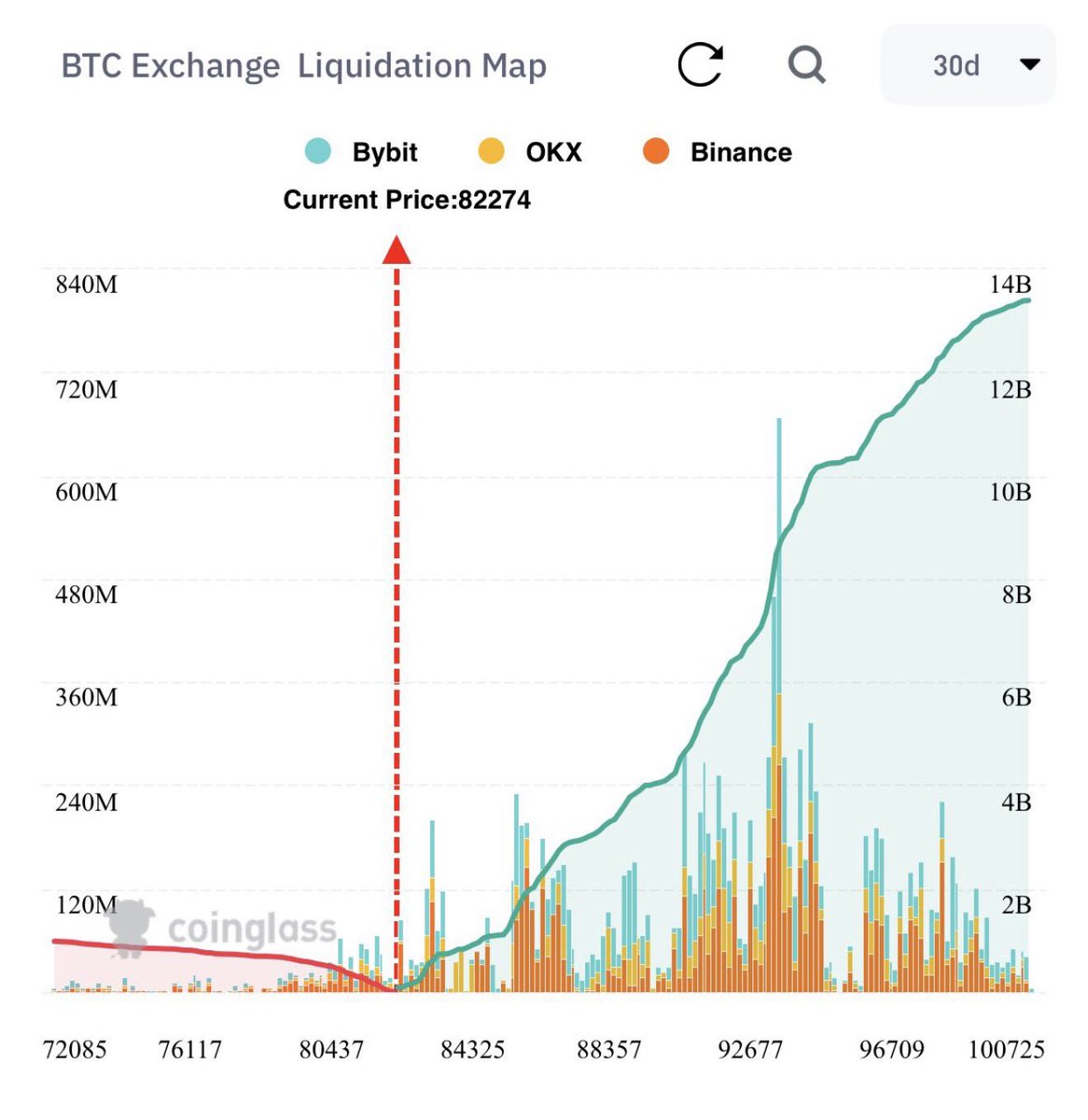

What happens when $14B in shorts are stacked against just $1B in longs?

(Save this. You'll come back to it.)

The current asymmetry in long/short leverage is insane.

And whether you're bullish or bearish, you need to understand what's happening beneath the surface.

Coinglass data is showing that between $84,000 and $100,000, there's up to $14B in potential short liquidations clustered together.

On the flip side?

Roughly $1B or less in long-side risk sitting underneath current prices.

That's a 14:1 imbalance.

Here’s what that actually means…

Liquidation maps show where leveraged positions will get forcibly closed if price moves against them.

When a short gets liquidated, it triggers a market buy.

Lots of shorts liquidating at once creates cascading buy pressure.

(These are the mechanics behind a short squeeze)

Price goes up, shorts get stopped out, their liquidations push price higher, more shorts get stopped out.

Rinse and repeat.

The asymmetry here is extreme.

If $BTC pushes toward $90K and beyond, it enters a zone dense with short liquidations.

Each level breached could trigger the next wave of forced buying.

Meanwhile, downside liquidation risk is comparatively thin.

Now for the reality check...

We just saw over 267,000 $BTC traders get wiped out in a single day.

Price dropped 10% from recent $90K highs.

So the map cuts both ways.

Similar setups have appeared before without triggering the expected squeeze.

Liquidation maps show potential, not destiny.

Market makers and large players see the same data. They can hunt liquidity in either direction.

But the setup has us watching closely.

A move toward $100K would plow through an INSANE wall of short liquidations.

The fuel is there.

Whether it ignites is another question entirely.

Bookmark this and come back to it if/when $BTC makes its next major move.

Thomas Kralow@TKralow

Wow. Probably nothing.

English

BREAKING:

Trump has nominated Kevin Warsh as the next Chair of the Federal Reserve.

Here’s what matters:

Warsh is widely viewed as hawkish on interest rates.

He previously served as a Fed Governor during the 2008 financial crisis and notably became the youngest Fed Governor in history at just 35.

Compared to all other options for Fed Chair, Warsh seems least likely to please Trump.

That suggests he’s far less likely to cut rates simply to satisfy pressure from the White House.

Kevin Warsh as Fed Chair will maintain the credibility of the Fed.

Milk Road Macro@MilkRoadMacro

We now have a new Kevin in the race for Fed Chair: Kevin Warsh. Unlike Hassett, who’s known for pushing rate cuts regardless of inflation... Warsh is generally viewed as hawkish on interest rates. Overall, we think Warsh might be less likely to attempt to please Trump, compared to Hassett. We’ve also seen reports that Wall Street heavyweights believe Hassett lacks the credibility to lead the Fed. Their concern: Hassett could push unwarranted rate cuts despite inflation risks potentially triggering a spike in long-term Treasury yields. May the best Kevin win.

English

"We had a lot of silver at one time but we don't have it now"

Warren Buffet & Charlie Munger explain why they sold their silver holdings in this clip.

With silver prices pulling back sharply, this is an important watch.

Save this video to stay one step ahead of the market.

The Kobeissi Letter@KobeissiLetter

BREAKING: Silver officially enters bear market territory, down -22% from its record high. Gold is now back below $5,000/oz.

English

Introducing Sky Ecosystem Insights.

Sky Frontier Foundation has established Sky Ecosystem Insights to address the lack of standardized financial reporting within DeFi.

This account exists to publish verifiable, institutional grade analysis of the Sky Ecosystem’s fundamentals.

While @SkyEcosystem covers ecosystem updates and product launches, this account serves as an independent analytical resource for the Sky Ecosystem.

The data you'll find on this account, which comes from public sources, will include:

- Quarterly and annual financial reports regarding Sky Protocol.

- Updates and analysis across the Sky Ecosystem and its fundamentals.

- Estimates and modeling for the growth of the Sky Ecosystem.

Think of us as the independent analyst covering the Sky Ecosystem.

The Sky Ecosystem Q4 Update and 2026 Outlook report goes live tomorrow, January 29th.

Follow us @SkyEcoInsights and turn on notifications so you know when the report goes live.

English

@MilkRoad @RealVision @RaoulGMI His house looks like the fake background I use in interviews to make it look like I'm successful 🥲

English

Why You Only Have Until 2030 to Build Wealth w/ @RealVision Founder @RaoulGMI

Gold is moving.

Crypto isn’t.

Raoul explains why that divergence has happened before and what usually follows for Bitcoin when liquidity catches up.

Tune in to know more

⏱ TIME POINTS ⏱

00:00 – Intro

00:52 – Why the 2026 Crypto Cycle Is Different

03:50 – Global Liquidity: The Real Driver of Crypto

09:08 – Raoul Pal x Milk Road PRO Offer

09:22 – The Damage From the Biggest Crypto Liquidation

12:29 – When Retail Comes Back to Crypto

14:31 – $BTC vs Gold: The Catch-Up Trade

16:18 – The Macro Case for a 5-Year Cycle

18:33 – What Happens After This Cycle Ends

20:05 – How Crypto Grows From $3T to $100T

23:21 – Bridge

23:55 – Chainlink

24:15 – Crypto’s Ethos vs Institutional Adoption

28:22 – The Mistakes That Destroy Long-Term Wealth

32:57 – Crypto in a Post-AGI World

36:05 – Raoul Pal’s Portfolio Framework

38:00 – AI Sectors That Could Explode

40:02 – Why Humans Still Matter

46:51 – Why the Clarity Act Matters

47:38 – Raoul’s Best & Worst Calls

52:53 – Wrap-Up

English

@TheDDiscourse @MilkRoadAI @KobeissiLetter There’s literally a post attached naming multiple large companies that have replaced human labour with automations…

English

@MilkRoadAI @KobeissiLetter AI 🤣🤣 AI is no where near advanced enough to replace human employees in any field. Name we one company that did mass lay offs due to replacing people with AI. This is due to taxing corporations to death and destroying the average American mom and pop shops with taxes

English

Recent Layoff Announcements:

1. US Government: 307,000 employees

2. UPS: 48,000 employees

3. Amazon: Up to 30,000 employees

4. Intel: 24,000 employees

5. Nestle: 16,000 employees

6. Verizon: 15,000 employees

7. Accenture: 11,000 employees

8. Ford: 11,000 employees

9. Novo Nordisk: 9,000 employees

10. Microsoft: 7,000 employees

11. PwC: 5,600 employees

12. Salesforce: 4,000 employees

13. IBM: 2,700 employees

14. American Airlines: 2,700 employees

15. Paramount: 2,000 employees

16. Target: 1,800 employees

17. General Motors: 1,500 employees

18. Applied Materials: 1,444 employees

19. Kroger: 1,000 employees

20. Meta: 600 employees

Where will all these people go?

English