tejada

6 posts

tejada

@tejada444

Value Guy. Avid Reader. Curious. Tweets are own; I keep open mind & may change views. Tweets are NOT investment advice/recommendations. Do your own diligence.

United States Katılım Temmuz 2013

6.3K Takip Edilen922 Takipçiler

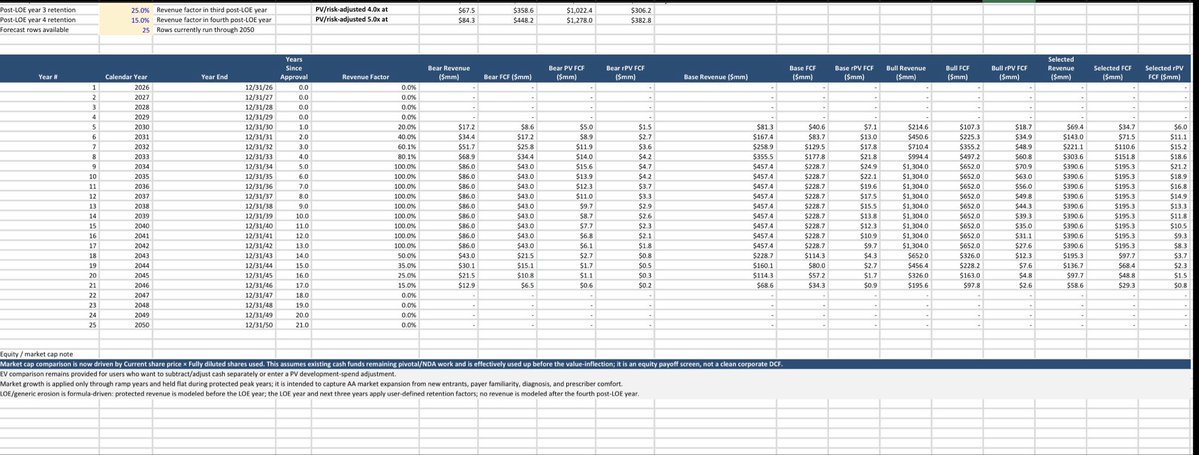

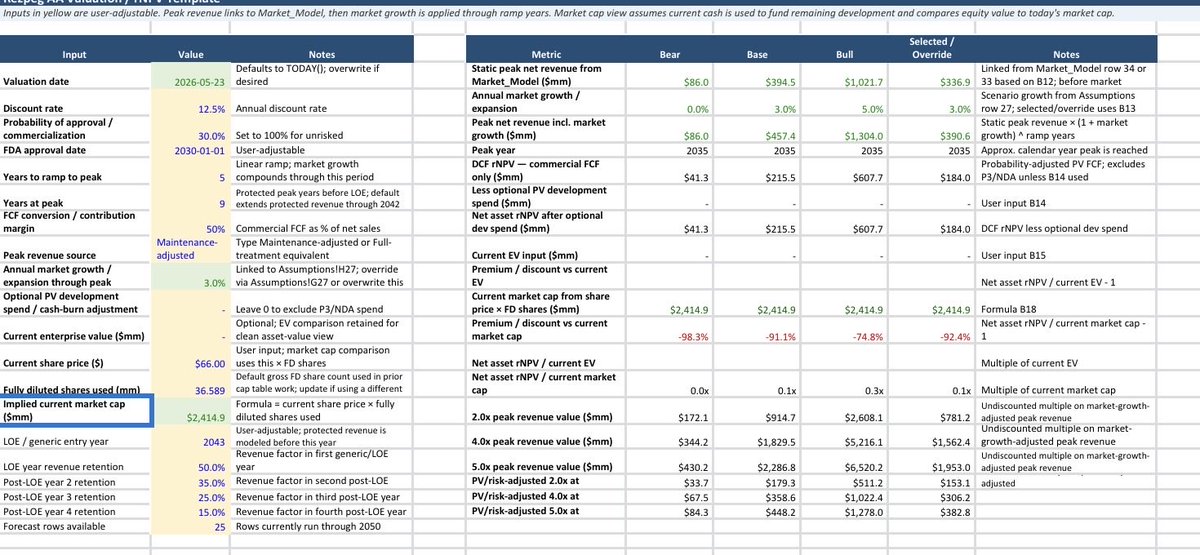

@seedy19tron Certainly. Maybe should’ve been more clear but the model I posted above is ONLY AA.

I think nktr is kinda binary: no cancer, POS markedly up; AA then yes 700m range

Working on AD, hopefully tm or Monday

English

$nktr

rezpeg value in AA is a 3 variable problem:

- mechanism linked longterm safety: cancer signal? (shared with AD) (over past few weeks this has, for me, evolved into the only thing that matters)

- maintenance durability

- proving efficacy (messy and heavily imputed p2)

Systemic AA market expansion could be a fourth.

Primarily bc of my concern of a delayed immune-surveillance risk, I use ~30% POS.

dcf inherently flawed in biotech but it forces ideas to paper and numbers to ideas: consideration of mechanics and links. Small adjustments create large output changes. Actual numbers should be taken with grain salt. That said, pics of mine for AA are attached. A link to a downloadable version including assumptions to play around with will follow this post.

Low POS, 50% gross to net, and q3m maintenance requires low AA valuation ($200-300m).

Note: this is an equity payoff rather than clean asset DCF as for simplicity I’ve assumed cash currently in NKTR used for trial completion, rather than cash outflows in the DCF. Doing it this way requires comparing to market cap rather than EV. The model has the flexibility to change this if downloaded

A few points:

1) I don’t think a legit NKTR valuation can have markedly different POS for AA/AD; they should be within 10-15% of each other. Rezpeg works. The big monster in the closet is do we get cancer signal with 1000+ people being on this drug longterm? If it’s gonna happen, p3 or commercial will reveal it.

2) commercial uptake likely depends on heavy gtn discounts.

3) rezpeg can differentiate from JAKs on maintenance. This is big for commercial uptake as q3m highly patient friendly. However, has to be built into the model. At any one time say 30-40% of patients will be q3m rather than q2w

4) ISRs don’t matter

English

Added to $GPCR at these levels. Underperforming name in my biotech portfolio, but I find the valuation attractive.

English

@Biohazard3737 One more:

3) LTE + bispecific = greater immunogenicity / ADA. How did you address that / think of that?

English

@ElMonoGran42994 No. Lots of in-class cytokine competition and pricing erosion from dupi biosimilar.

With novel MoA and immune reset MOA, $nktr is literally—not just first and best—in class…but by itself.

English

@tejada444 Problem is the dozen of competitors preventing this scenario from ever happening

English

@JoseRestonVA Despite my curiosity, I won’t ask what that level that is but look forward to hearing about it, if and when the opportunity is right!

English

@tejada444 I am watching it. I like the company but it has not reached the levels where I would get back in for the type of r/r I want to get. I am in no rush.

English