Open Banker

6 posts

John Pitts@PolicyPitts

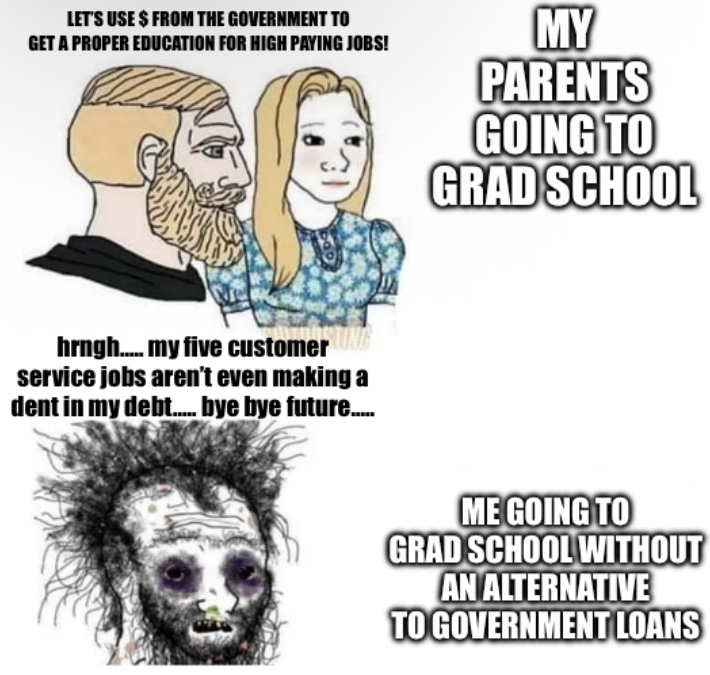

Back to school means 2 things: 1. Mack Wallace writes on the danger and opportunity in the feds exit from graduate student lending; and 2. In an effort to attract the youth demographic, @theOpenBanker has hired my 14 y/o as nepo baby social media intern. Enjoy(?) their tweets.

ZXX

@NikMilanovic @gwlaw Thanks for highlighting! Here's the article link, for anyone who's interested: openbanker.beehiiv.com/p/dangeroussta…

English

We've seen a lot of takes in-favor of the GENIUS Act, so in fairness, I thought I'd share the perspective of someone who's bearish:

Professor Art Wilmarth at @gwlaw belives the GENIUS Act is a deeply flawed piece of legislation that would:

👉Allow nonbank entities to issue uninsured stablecoins without proper oversight.

👉Threaten financial stability, consumer protection, and the broader economy.

His arguments:

🧨 Systemic Financial Risks:

👉Nonbank stablecoins function like uninsured bank deposits, making them vulnerable to runs, similar to past financial crises.

👉Historical parallels: Past crises (1980-92, 2007-09, 2023) showed that uninsured short-term instruments often required government bailouts.

👉Example: In 2023, Circle’s USDC dropped to $0.87 after SVB's collapse; a government bailout was needed to stabilize it.

⚠️ Failures of Stablecoin Technology & Usage:

👉Public blockchains (on which most stablecoins run) suffer from:

Scalability issues

👉Immutability problems (fraud/error correction is hard)

👉“Layer 2” fixes mimic traditional financial systems, so they should be regulated like banks.

👨💻 Big Tech Entry into Banking:

👉The GENIUS Act would allow tech giants (Apple, Google, Meta, etc.) to:

👉Enter the banking space via stablecoin issuers.

👉Gain access to sensitive financial data.

👉Build dominant financial empires, undermining the separation between commerce and banking.

🏦 Shadow Banking 2.0 & Subprime 2.0 Risk:

Stablecoins could:

👉Drain deposits from FDIC-insured banks, harming community lending.

👉Fuel a crypto derivatives boom, creating a speculative bubble like the subprime mortgage crisis.

🧱 Additional Flaws in the GENIUS Act:

👉Weak reserve, capital, and liquidity requirements.

👉Lax chartering criteria for issuers.

👉Poor regulatory oversight, especially over state-chartered and foreign issuers.

👉Minimal consumer protections.

👉No federal safety net for failed issuers—inviting ad hoc bailouts.

@twifintech @thestablecon

English