Sabitlenmiş Tweet

don

1.1K posts

don

@Thedonkey

building the world’s fiat rails

in between Katılım Ağustos 2023

269 Takip Edilen837 Takipçiler

@AriEiberman @joinpeanut I fight for ppl's rights for privacy, not for avoiding paying taxes.

We have our duties as citizens.

English

@Thedonkey @joinpeanut It surprises me coming from you.

Well played👏🏻

English

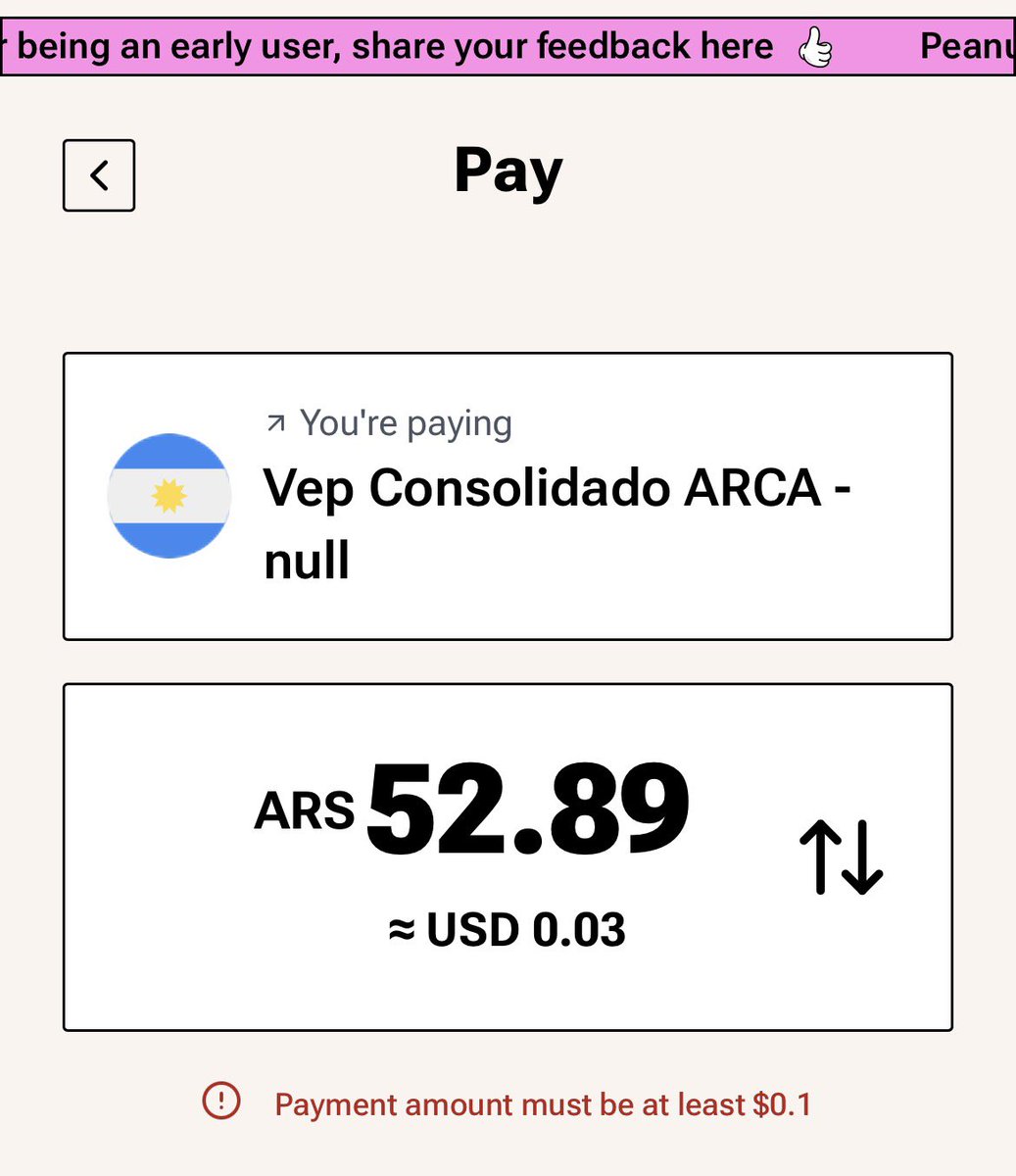

Am I the only one who is trying to pay govt taxes debt with stablecoins?

@joinpeanut at least can read the QR from arca.

English

Some people search for meaning.

NOIR travels with it.

No fixed place.

No announcements.

Just movement between silence and observation.

Most don’t notice when he arrives.

Only when he’s gone.

He speaks rarely,

because unnecessary words weaken perception.

opensea.io/item/ethereum/…

English

Selfcustody is the key for a more balanced relationship between users and banks / institutions.

Neobanks are key for users having their assets and taking control of their income.

Using pre-paid credit card / debit cards, self custody, no institution taking a cut from your income without you consenting.

This is where it starts.

English

@Thedonkey Hi Don interesting reflection on actual facts. I did not understand the "how it gets spent" part tho. Are you suggesting crypto debit cards are what people should be using instead of crypto credit cards (on neobanks for example)?

English

We are living a debt epidemic, and it has become so common that most people no longer recognize it as one.

Four out of every five Brazilian families are in debt right now. Half of them have no way to pay it back. The same pattern, in different forms, is repeating across most of the world.

- In Brazil, 80.2 percent of families carry debt, the highest level in 16 years of tracking.

- 85 percent of that debt sits in credit cards, where revolving interest routinely crosses 400 percent a year.

- Among families earning up to three minimum wages, 38.9 percent are already behind on bills, and nearly one in five says they have no ability to pay them next month.

- Globally, total debt sits above 235 percent of world GDP.

This is the steady state.

The bear market and the migration of attention toward AI have pulled the conversation in crypto away from the things that originally made it matter. That is a natural cycle. But it is worth using this moment to remember why these tools were built. The use case that justifies their existence is not somewhere in the future. It is in the inbox of every family staring at a bill they cannot pay.

The most common explanation for the debt epidemic is that people lack financial education. This is wrong. The United States runs the largest financial education infrastructure on the planet. Personal finance is taught in public schools. Television networks, podcasts, and bestselling books are dedicated to teaching ordinary people how to manage money. And yet US household debt reached 21.2 trillion in Q1 2026, with credit card balances at a record 1.277 trillion, and 37 percent of Americans cannot cover a 400 dollar emergency without borrowing. If education were the missing variable, the country that produces the most of it would have the lowest debt. It has the opposite.

The problem is not informational. It is structural. People know they should not be in debt. People know they should save. The issue is that the system makes acting on that knowledge nearly impossible, because the money never sits long enough in the household's hands for any plan to take effect. Telling someone to budget when their salary is already partially deducted before it arrives is not education. It is theater.

The mechanism is simple. In the current setup, the creditor decides the order of payment. When a family owes money on a credit card, an overdraft, a personal loan, a buy now pay later plan, and an installment for an appliance, the bank decides what gets collected and when. The salary lands in an account held by the same institution that holds the debts, and the institution applies its own priorities to that money before the worker sees it. The family spends the rest of the month reacting to whatever pressure arrives next.

This is the structural fact that matters. The order of payment is decided by whoever holds the money, and in the current system that is almost never the household itself.

Every serious framework for getting out of debt rests on the same idea. You list what you owe, you decide the order, you attack one debt at a time until it is gone, then you move to the next. The math of which debt to pay first matters less than the act of choosing. The frameworks work because they put the household back in control of the sequence. But they only work if that control actually exists. In a system where the bank holds your salary, your debts, and the right to deduct payments before you see the money, you do not have the freedom to sequence anything. The bank already sequenced it for you. Without the ability to hold your own income, every debt elimination framework becomes motivational content. With it, the same framework becomes executable strategy.

We need better tools tho.

Self custody is the technical capability to hold your own money outside an institution that has competing claims on it. If your income lands in a wallet you control, in a stablecoin you choose, you decide which debt to pay this month, in what amount, and in what order. The bank stops being the operating system of your finances and becomes one counterparty among several.

This is not an ideological position. It is the structural position that wealthy households already occupy through lawyers, accountants, and separate accounts that let them direct their own cash flow. Self custody gives the same position, in a much simpler form, to people who never had access to those tools.

The second piece is how the money gets spent. Credit cards are the most expensive form of household borrowing on the planet, and they are the default way most people transact. Non custodial alternatives are the opposite. You can only spend what you actually have. There is no revolving balance compounding while you sleep. Paying becomes a deduction from your own assets, not the creation of a new liability.

The technology to deliver this already exists, they have the rails, the wallets, and the user interfaces to put self custody in the hands of ordinary people. What is still missing is the framing. Most of these products are positioned as crypto tools for crypto users. The real opportunity is to position them as what they actually are, which is a way out of the debt epidemic for households that have no other way out. That shift in purpose is not a technical problem. It is a question of who these products decide they are building for, and what proposition they put at the center of their work.

Together, these pieces give a household something the current system does not. A place to hold income that no creditor can touch first. A way to spend that cannot turn into debt. And the freedom to decide the order in which obligations get paid. That is the entire structural difference, and it is enough to change what is possible.

The population using these tools today is small relative to the population that would benefit. That is the natural state of any new technology. The work that comes next is making the same capability available to people who do not have the time or technical background to learn the underlying machinery. The onboarding has to be shorter than opening a bank account. The interface has to assume the user does not want to learn what a private key is. The product has to work for somebody three months behind on a bill, earning a minimum wage, who has never opened a wallet.

The debt epidemic is not going to be solved by the same institutions that produced it, and it is not going to be solved by teaching people lessons they have already heard a thousand times. The solution is a shift in who holds the income and who decides where it goes, delivered through tools simple enough that the shift can actually happen.

English

@Thedonkey how is crypto helping here? apart taking the role of the debit card?

English

@defiremora Comprar carro

Endividar usando a grana de entrada em dívida maior

Consórcio

Português

Top MAIORES cagadas que fiz quando ganhei uma boa grana:

Comprar carro zero km

Português

Quick update: I'm leaving @p2pdotme.

Thanks for the team who showed up every day

The circle admins who built local trust where none existed

The merchants who put their reputation on the line so strangers could move money back home and

The content creators who helped us tell the stories.

Building crypto payments only works when real people trust each other, glad to see how far we got building this.

Not leaving the crypto space tho.

Onwards :)

English

I've been working for a multinational bank since 2012

Joined crypto on 2021

Now I'm becoming some kind of @solana DevRel/KOL in my country (Argentina)

I need to quit my job and go full web3 ASAP

I need to help and on board more Argentine developers to solana

Trying to find some time to put together a proposal for @Superteam

I have a small team in mind to start with

But I need to start yesterday

English

@CiscoCANFT @thesunno @isasuarezes @p2pmevenezuela We don’t charge gas, just send to your Binance EVM address on base.

English

@thesunno @Thedonkey @isasuarezes @p2pmevenezuela Puedes mandarlos o recibirlos por Base a Binance, pagas la comisión de red que son literal un centavo

Es una wallet EVM descentralizada, si quieres puedes importarla en MtaMsk o Rabby, Trust Wallet y usarla para DeFi, cambiar por USDT, comprar alts, mandar a CEXs

Español

¿Porque mudé el 80% de mis operaciones p2p a @p2pmevenezuela?

En este hilo voy a responder las preguntas más frecuentes del post anterior y explicar algunos detalles técnicos de la manera más sencilla:

Pruebas Zk, medidas anti triangulación, protección al usuario...

Va hilo

Cisco | CryptoAlert@CiscoCANFT

Sin Binance, ¿cuál es la alternativa para hacer P2P en Venezuela? Ayer hice este post sobre lo que significa que Sunacrip regule Binance en Venezuela y varios me preguntaron sobre alternativas Desde la semana pasada (antes de los rumores), he estado probando una alternativa que me vienen recomendando hace unas semanas: @p2pmevenezuela Este protocolo descentralizado es muy usado en India, Brasil, Argentina y Colombia y hace poco llegaron a Venezuela Luego haré un post más detallado y técnico, pero mientras te cuento rapidito lo que me gustó y lo que no: Lo que me gustó: •Me tomó menos de 10 minutos abrir la cuenta, comprar USDC desde mi banco con Pago Móvil y tenerlos disponibles •Es perfecta para micropagos: pagué directo al QR del pago móvil del vendedor desde mis USDC y el comerciante recibió los Bs en su banco, todo en menos de 3 minutos. Con Binance u otro CEX hubieran sido 15-20 minutos buscando comerciante, pagando, liberando... •El protocolo p2pme hace todo el trabajo sucio (matching de órdenes, pagos y liberación). Ni tú ni el comerciante se enteran de los detalles técnicos, se siente como pagar directo con USDC a tasa "Binance" •Es privado y descentralizado: Usan pruebas ZK y no almacenan ningún dato tuyo (identidad, teléfono, cédula). No hay base de datos que hackear o exponer •Es verdaderamente autocustodia: puedes exportar tu wallet e importarla en cualquier otra billetera. Incluso si el protocolo llegara a fallar, siempre tienes acceso a tus fondos Lo que no me gustó: •Es una ladilla cuando el vendedor quiere una captura del pago. Solo me pasó una vez entre 7 compras. Le expliqué que era un sistema nuevo y le mostré la transacción en la wallet. Ella ya había recibido la notificación normal en su banco, así que se resolvió rápido •Tienen un solo proveedor de verificación social ZK. Eso es un punto de centralización que no me gusta. Sin embargo, el whitepaper menciona explícitamente el uso de “Reclaim y otros ZK verifiers” y habla de un verifier registry on-chain para agregar más proveedores en el futuro. Ojalá lo implementen pronto •Las tasas: en el momento de este post la diferencia de precio entre Binace p2p y P2pme es de 0.6% para la compra de usdc y 1.7% para la venta. En teoría conforme haya más adopción debería cerrarse más En resumen, no es perfecto y todavía hay cosas por pulir Pero después de leer la documentación completa y probarlo en vivo, siento que la propuesta va en la dirección correcta: Menos confianza en empresas, más confianza en código, incentivos y matemáticas Sobre todo, para mí gana por ser fácil y rápido Si alguna vez te ha pasado que tienes liquidez en cripto pero no tienes moneda local y te da la misma ladilla que a mí lidiar con el P2P de Binance para un pago pequeño, vas a agarrarle el gusto a p2pmevenezuela.

Español

eu amo quando o governo quer proibir algo relacionado a cripto

pq ai eu lembro o motivo de estar em cripto, que é justamente nao sofrer proibição do governo

Modular Crypto 🔲@ModularCrypto

USDT e USDC podem ser proibidos no Brasil. O Banco Central já mandou nota ao Congresso. Se avançar, o mercado cripto muda de vez. Isso e muito mais no Modular DailyNews de hoje. Crypto, IA e o futuro na sua caixa todo dia. Assine grátis newsletter.modularcrypto.xyz/p/banco-centra…

Português

A common critique of P2P fiat-crypto systems is that the fiat rail itself, like Pix in Brazil, is inherently traceable, so anything built on top inherits that traceability. The critique is partially correct and worth taking seriously. But it transfers by inertia to architectures that don't share its assumptions, and the conflation hurts honest discussion of what privacy is actually achievable. Brazil's Pix has the strongest publicly documented forensic surface of any major instant payment system, so it's a useful case study, and the lessons generalize.

The critique gets a lot right. Pix participants must retain XML message contents for 10 years. DICT query logs persist for 2 years with mandatory headers tying queries to payer CPF via PI-PayerId and PI-EndToEndId. AML records under Circular 3.978 require at least 10 years. For systems where the crypto user is the direct Pix payer, this is decisive: their CPF lives in payer PSP logs for a decade. For systems with centralized fiat-to-token issuance, correlation is even cleaner because the issuer holds the mapping between payer identity and on-chain destination. For systems requiring federated peg-out, additional choke points exist as forensic clocks. This is correct forensic analysis.

But the critique assumes specific architectural choices: crypto user as direct Pix payer, centralized issuer, federated bridging, KYC custodial wallets at endpoints. Change those assumptions and most join points disappear.

Consider an alternative architecture, abstracted from any specific product. On-chain matching with stake-based reputation and no custody. Pix validation via zkTLS, where the protocol receives proof the Pix occurred without seeing the data. Smart account wallets with no KYC anchor and no CEX endpoints. A pulverized network of human merchants with volatile application caches. Off-ramp flows where the client sells crypto and receives Pix into a legitimate third party's account, never directly handling Pix with their own CPF.

Apply the same forensic framework. EndToEndId and DICT logs still exist but bind the merchant's CPF to the third party's CPF. The crypto client appears in neither field. The 10-year payer PSP record is irrelevant to identifying the client. Centralized issuer doesn't exist, so there's no entity that holds the payer-to-address mapping. Federated peg-out doesn't exist, so no administrative timing windows as forensic clocks. On-chain clustering heuristics like multi-input and peel chains require KYC anchors to bootstrap entity identification, and AA wallets without co-mingling degrade these significantly.

I'm not claiming absolute privacy. What remains is real. Temporal correlation between Pix settlement and on-chain transaction enables statistical matching, mitigated by volume but not eliminated. Live cooperation from subpoenaed merchants before caches expire still yields information. Heavy users create patterns identifiable even without explicit KYC. Real, but qualitatively different from "tax authority queries CPF and sees everything." Directed investigation has to start from outside the system and depends on human cooperation at each hop.

Privacy in P2P fiat-crypto rails is stratified, not binary. Against pure chain analysis, high with AA wallets and no CEX endpoints. Against tax authority CPF queries, high in third-party off-ramp mode. Against long-term application retention, high with volatile caches. Against directed investigation, medium, depends on pulverization and human cooperation at each hop.

The blanket claim that fiat rails leak so all P2P built on them leaks equally is wrong in a way that matters for users making real decisions. Architecture choices change which forensic paths exist. The user offramping into a third party's account through a non-custodial protocol with a non-KYC wallet is in a structurally different position from the user buying tokens directly from a centralized issuer with their own bank account. The discussion worth having isn't whether privacy in P2P fiat-crypto is real. It's which threat models specific architectures defend against, where they degrade, and what users can reasonably expect at each stratum.

Hugo Quinteiro@Hugo_Quinteiro

Não é privado se utiliza pix 👇🏻

English

@BitcoinViral999 @p2pmevenezuela Verifying regular KYC is easier.

For you, and for the govt.

English

Amigos de @p2pmevenezuela es bastante tediosa la verificacion de redes sociales. ☹️

Español

Fala Hugo, beleza? Muito bom teu artigo e fiquei impressionado com teu conhecimento técnico dos mecanismos por trás. Ajudou a enxergar várias coisas. Acho que a única parte que podemos ser honestos e que I artigo assume premissas que nem toda arquitetura compartilha.

Tudo que tu levantas sobre logs PSP por 10 anos, DICT amarrando PI-PayerId a EndToEndId, retenção da 3.978, sigilo não oponível ao BC pela LC 105, é verdade. CT na Liquid não esconde valores de quem tem chaves de desblindagem ou logs de aplicação. Peg-out federado cria choke points temporais rastreáveis. Forense legítima.

Mas o teu artigo descreve um sistema com características específicas: emissor centralizado tipo TIE, banking node identificável, peg-out federado, e principalmente o cliente cripto sendo o pagador Pix. Quando essas premissas mudam, a maioria dos join points que tu listas não existe.

Imagina um sistema P2P onde o matching é on-chain via stake sem custódia, a validação do Pix usa zkTLS então o protocolo recebe prova sem ver os dados, as wallets são smart accounts não-KYC sem âncora em CEX, os merchants são pessoas físicas pulverizadas com cache aplicacional volátil, e no offramp o cliente vende cripto e recebe Pix em conta de terceiro legítimo, nunca tocando o Pix com o próprio CPF.

Aplica teu próprio framework forense. EndToEndId amarra CPF do pagador, mas o pagador Pix é o merchant, não o cliente. O log existe e não diz nada sobre quem é o cliente cripto. Banking Node e TIE não existem. Peg-out federado não existe, sem janela de 11 a 35 minutos como relógio investigativo. Heurísticas de clustering on-chain ficam fracas porque AA wallet sem histórico KYC e sem co-mingling com endereços CEX não dá âncora para começar o cluster.

Não estou argumentando privacidade absoluta. Sobra correlação temporal Pix-on-chain mitigada por volume mas não eliminada. Sobra cooperação humana do merchant se intimado antes do cache expirar. Sobra log do PSP do merchant, mas com CPF do merchant e do terceiro, não do cliente. Sobra padrão estatístico em uso intensivo. Reais, mas qualitativamente diferentes. Não é Receita olha CPF do cliente e vê tudo. É investigação direcionada precisa partir de outros meios e depende de cooperação humana em cada hop.

Sobre a camada jurídica, a cadeia regulatória que tu mencionas depende de existir entidade brasileira a quem citar. Para protocolos com fundação em jurisdição não-cooperante, governance descentralizada e fundadores anônimos, enforcement direto contra a entidade é improvável. Sobra enforcement contra atores locais. A defesa real é assimetria de custo, não imunidade jurídica.

Agora sim, concordo: Pix por si só não é privado, nunca foi. Também concordo com a crítica a arquiteturas que mantêm o cliente como pagador Pix direto, ou que centralizam emissão, ou dependem de federação. A diferença que aponto é que essas premissas são da arquitetura, não do problema.

Privacidade em P2P fiat-cripto é estratificada. Contra chain analysis pura, alta com AA wallet não-KYC sem ponta CEX. Contra Receita olhando CPF do usuário, alta no offramp para terceiro. Contra retenção aplicacional, alta com cache volátil. Contra investigação direcionada, média, depende de pulverização. Contra enforcement regulatório, baixa para operadores locais, média para usuários.

Teu artigo descreve corretamente os últimos estratos para certas arquiteturas.

Fica o convite: faz uma análise equivalente da documentação e estrutura da P2Pme em docs.p2p.foundation. Aplica o mesmo rigor forense que aplicaste ao DePix, e vamos ver onde os join points realmente caem nessa arquitetura. Acho que o debate fica mais útil assim, e eu leio com o mesmo cuidado que li o teu.

Português

Não é privado se utiliza pix

👇🏻

P2P.me Brasil@p2pmebrasil

Nada muda pro usuário da P2Pme. Privado Autocustodial Descentralizado

Português

Hoje entrevistamos o dev @ManczEd que falou um pouco sobre o seu projeto STRUCTA!!

@SuperteamBR

Português

@NYRKY69 @meta_arg @rpjupiter @Oriebir_br @lorenaalmada @reclaimprotocol @ZKPassport @P2Pdotme Join the TG channel for your region, our team is available to provide you support :)

English

@meta_arg @Thedonkey @rpjupiter @Oriebir_br @lorenaalmada @reclaimprotocol @ZKPassport Sabes porque pasa esto? @P2Pdotme

Español

Quais são hoje as formas mais acessíveis de comprar Bitcoin no Brasil sem perder 100% da privacidade? 👇🏻

Português