TheYieldFarmer

1.3K posts

TheYieldFarmer

@theyieldfarmer

Love the smell of fresh yields in the morning....👃%

Katılım Eylül 2020

373 Takip Edilen194 Takipçiler

TheYieldFarmer retweetledi

172 days ago the Stream team messaged me to complain about a snarky tweet I had made about their vault code.

This was the last message I sent them.

Obviously they did not listen and we are in fact worse off because of it.

Contrary to what many seem to feel, none of what happened came out of nowhere. As with any good bubble/blow up it has been slowly brewing and was simply a matter of time till it burst.

It took one conversation with their and 5 minutes of scrolling their Debank to realize that this was going to end poorly.

And while Stream was the most egregious, they are far from the only ones out there with bodies to hide.

So while I have my 15 minutes of CT's attention here are a few long, but hopefully final, thoughts on our latest saga.

First on Stream in particular.

Even I was surprised at the size of their loses, and while we wait to see what the official reason for the hole is, I think its pretty obvious you don't delegate 9 figures of user capital to "external managers". And the only way you loose that amount of money is leverage trading shitters.

Seems clear these kids started directionally trading with user capital while lying about it. This isn't a phenomenon unique to DeFi, it's a tale as old as time. And ironically one of the primary original selling points of the benefits of DeFi, to not allow this.

Nonetheless, I still don't think the market has fully grasped the extent of the insolvency. At time of writing this xUSD is trading at about $0.25 or 20% of its PPS of 1.27 and deUSD is at $0.99 still. So lets do some math.

If we look at the current state of Stream's assets their total DeBank bundle claims $138m and liabilities of their dashboard says $160m of user deposits.

However, seams safe to write off all of the value in 0x15 at this point, given its almost all xUSD and deUSD levered positions that they have no ability to ever unwind. And assume their new msig 0x14b is all of the returnable funds which is currently $63m.

Then we come to the liabilities, which is where the recursive looping and unbacked minting kicks everything up. Since they have no viable path to repay their xUSD loans we can assume that all will eventually end in liquidation in some capacity. Which given the limited on chain liquidity likely leads to lenders taking possession of the xUSD posted as collateral, which fully breaks their recursive accounting and causes a 2X+ of the outstanding xUSD liabilities and creditors that will be looking for repayment and redemptions.

My best estimate from Debank is they have a total of close to 300m xUSD currently leveraged across their wallets. At current PPS of 1.27 this increases their outstanding liabilities by about $380m to $540m.

Which would then give an expected redemption value of 63/540 for close to a 90% loss or $0.14 per xUSD.

Of course this also means deUSD will take at minimum 20-30% bad debt, assuming their 1:1 agreement won't hold up given Stream doesn't have enough to pay Elixir back in full even if they did abide by it.

And anything lent or backed against xUSD or deUSD takes on their equivalent amount of bad debt.

Fun thought experiment for the reader is how do you price the 6.2m deUSD 0x14 currently holds given its redemption price is dependent on xUSD's.

Now, I have no idea when or if these liquidations will actually occur. Given all the oracles are hardcoded, lenders only recourse is to wait till the interest accrual liquidates them.

Places like Elixir's Morpho market on Plume this is likely to happen soon given Morpho's adaptive IR curve the borrow rate is already 190%.

On Euler, especially Plasma, it could take months given the hardcoded caps on the IR curves.

While I would expect the redemption process to take weeks to months, it is also possible they keep these positions alive long enough to just serve withdraws to circulating shares and therefore all lenders to xUSD will take a 100% loss in order to reduce the losses for current xUSD holders.

This exact reason is why, regardless of their shitcoin trading practices, what they were doing with collateralizing the self looped shares was extra levels of retardio even for this industry.

And as always is another friendly reminder that leverage is a fickle bitch and magnifies in both directions.

_____________

While I will leave most of the pontificating about the long term effects to DeFi to the clearly ever so alert CT crowd, obviously we have some issues.

At Yearn we have been speaking about this for quite some time, but seams the rest of DeFi has now woken up.

While any new meta such as Curation or Vaults, will have people pile in and there are bound to be bad actors or those that cut corners.

This clearly goes far beyond that. Almost every major "risk manager" showed themselves to be baphoon's in some capacity far beyond just those that directly allocated to Stream assets. Due diligence is the primary slower of growth and therefore gets thrown out first.

Users see vaults labeled as Prime, Core, Horizon, High Yield, etc all with a Curator name that means nothing to them and just end up chasing yields inevitably pushing the industry up the risk curve.

We need standardization, we need proper transparency and due diligence, and we need to understand when you treat financial markets like a high growth SAAS tech play, things like this are bound to happen.

A risk managers job is to say NO. If you are not doing that, or just waiting till shit goes sideways to try and pull your funds faster than others. Your not a risk manager you're a clown.

Hopefully as the system absorbs nine figures of bad debt it makes those leading the charge think a bit harder before they list the next shiny new shitcoin.

Outside of improvements to curation my top personal hope is this makes all vault providers currently using the black box method of off chain pricing their shares to change course.

This is one of the most terrifying widespread adoptions of this cycle, in which multisig's are arbitrarily setting the PPS of their vaults based on undisclosed off chain pricing logic.

And to be clear Stream is not the exception here, this is now standard practice from almost every vault provider, including basically all of the largest players. If you are in a blah, blah USD or "Vault yada yada", "YieldCoin Whats its Nuts" or whatever, you are almost certainly subject this.

As the industry continuous to move to a less cypher punk value set, we should make sure there is a distinction between decentralization and transparency. Even in places where we move to more centralized/trusted systems, transparency should still exist in its full force. Otherwise we really are just banking but worse.

While events like this always remind me why I am embarrassed to tell people I work in crypto, so far there does seem to be a positive response and recognizing our shortfalls.

Though I am sure next cycle a new group of kids will come along claiming they've got the best risk adjusted yields around and we will run it back once again.

Our only hope is each time this happens a few more people learn to demand more out of those they trust their money to.

English

TheYieldFarmer retweetledi

Like, RT and follow to open this box 👀

Will pick out a few winners for a special reward 💜

English

Every quest adds strength to the soil!

I'm collecting beans to fuel Gassy Jack's climb out of the gassy world 💨 Invite others to multiply the growth and share in the rewards. Jump in now👇

ethgas.com/community/onbo…

ethgas.com/community/onbo…

English

TheYieldFarmer retweetledi

Debunking the FUD that Hyperliquid prioritizes protocol revenue over traders

On 10/10, Hyperliquid ADLs net made users hundreds of millions of dollars by closing profitable short positions at favorable prices. If more positions had been backstop liquidated, HLP could have made hundreds of millions of dollars more in pnl, while being exposed to an irresponsible amount of risk. ADL passed on HLP's potential pnl to users while decreasing HLP's exposure, a win-win.

As a reminder the ADL queue on Hyperliqid has always followed a similar formula to what most CEXs use, incorporating both leverage used and unrealized pnl on the open position.

Finally, thanks to everyone for the feedback on ADL. Suggestions generally increase complexity, such as partially offsetting long and short positions in historically correlated assets. I don't know of other major venues that use more complex logic for the ADL queue. Simple formulas are more robust and understandable by users. Nonetheless, there is research being done on whether there can be substantial improvements that merit more complexity.

English

$7.5T moves daily in TradFi FX.

Now it moves onchain with @MentoLabs, and I’m part of it.

Claimed my FX ID.

Claimed my FX ID. You?

→ discord.gg/mentofx

English

TheYieldFarmer retweetledi

We don't need to ask "wen binance, wen binance" any more..

Projects need to give them 5%-8% of supply tokens for listing to their platform plus listing fee to just list on Binance Alpha.

On Hyperliquid, everything is permissionless. There is no listing fee, no listing department, and no gatekeepers.

Next project TGE, people will ask " When Hyperliquid? "

Hyperliquid@HyperliquidX

On Hyperliquid, there is no listing fee, no listing department, and no gatekeepers. Spot deployment on Hyperliquid is permissionless. Anyone can deploy a spot asset by paying a gas fee in HYPE. Deployers can choose to receive up to 50% of trading fees on their spot pairs. Everything is transparent and verifiable onchain. The full defi lifecycle includes building a project, launching a token, and trading that token. Every step of that journey can be done permissionlessly on Hyperliquid.

English

TheYieldFarmer retweetledi

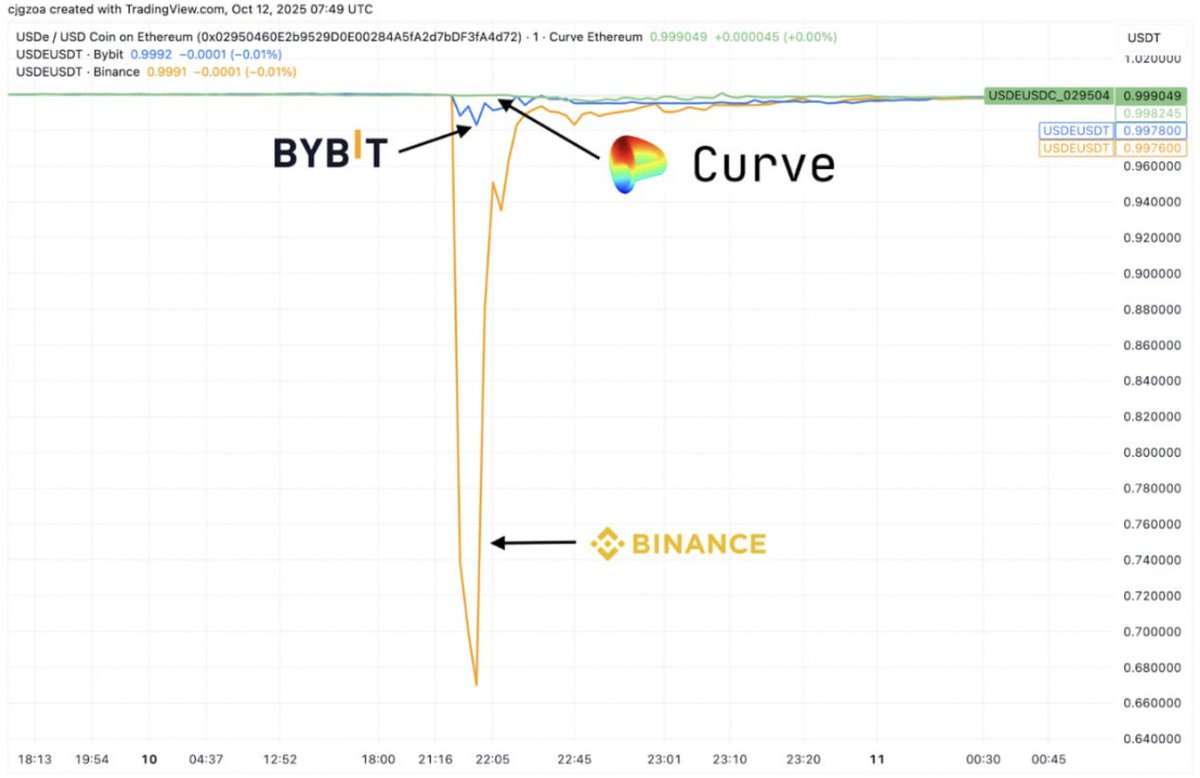

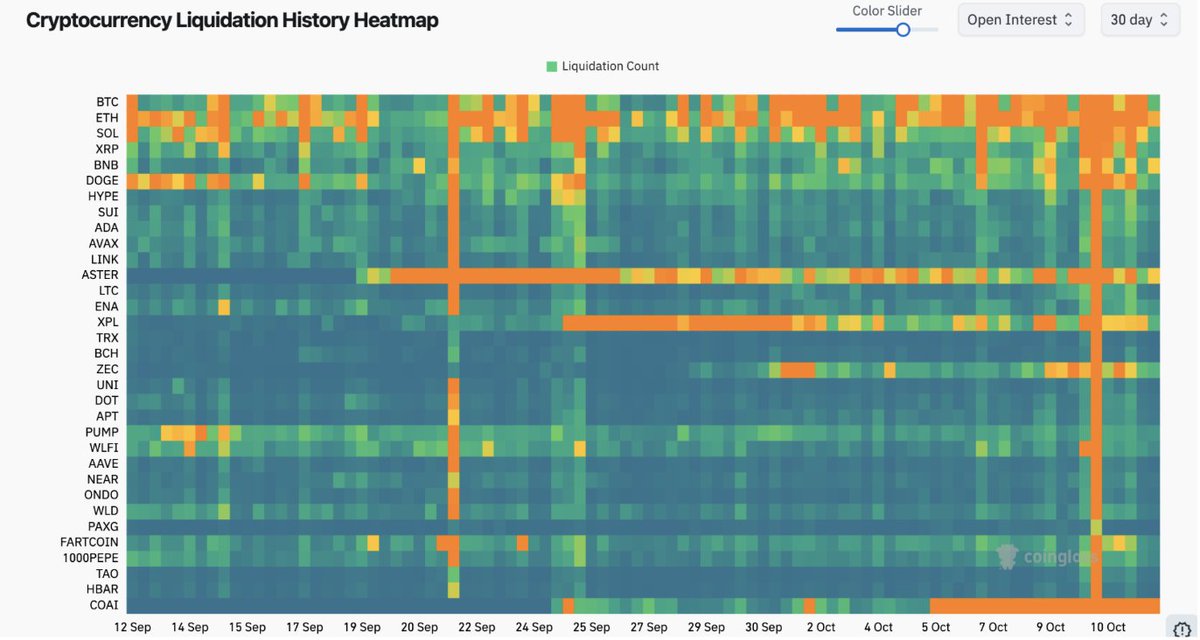

Oct 10 Crypto Massacre: Binance Edition

The most important microstructure fact from the October 10th crypto massacre isn’t just “volatility was high and we had chain congestion,” it’s that the reference/pricing/quotes many desks and DEXs lean on became unreliable, exactly when everyone needed it most.

As it stands today, I am cautious to make acquisitions on what the root cause was. It is easy to point fingers at Binance right now but I don’t think that is justifiable, yet. The timing of depegs and initial cascade is still being looked into.

This is subject to change with more info.

However, for us onchain users, the main issue was that Binance prices their wrapped assets at spot market price and not underlying value price. This is a known flaw that many borrow/lend protocols have identified, such as Solend and Aave, and is the reason many loopers were largely okay.

Using secondary market pricing as an oracle for a token backed by real dollars (or SOL with an LST) makes no sense -> given the market price != the real price.

Crypto has too many venues, so why should the Binance market for USDe be the bearer of truth when in reality USDe is always backed by real value. The mint/redeem price should be the bearer of truth not Binance.

Binance’s unified-margin stack was marking key collateral (USDe, BNSOL, wBETH) off its own spot order books. In the dislocation, those local markets detached from underlying value, WBETH printed in the $400s at one point while ETH itself traded multiples higher, and USDE/BNSOL also plunged on Binance versus external venues. Quoting for USDE was terrible and essentially caused anyone who was long an asset with usde as the collateral to get liquidated.

Okay, so if Binance was a big contributor to the mass liquidations onchain, how did Binance cause me to get liquidated on other perp DEXs?

Because in crypto perps, fair value is synthesized from a small set of anchors, and Binance is still the heaviest anchor. Most perps, CEXs and DEXs, blend top-venue spot feeds and many DEX oracles ultimately reference those same feeds.

When the largest venue’s API stalls, Binance, and its local spot marks misprice wrapped collateral, two things happen in the market maker (MM) stack: (1) inventory and margin models start screaming false signals (your collateral is supposedly worth 40–80% less when it is not), and (2) the external “mid” used to place quotes, skew sizes, and choose venues no longer feels trustworthy.

With no defensible mid, MMs do the only rational thing: pull size, push their quotes way back, or go dark entirely until they can recompute risk.

This is why some perp DEXs, those that held up better than others, still couldn’t fill some users’ bids. There were no market makers willing to quote. That gap shows up to end users as “spreads went crazy” and “can’t get filled,” even on DEXs that did remain online. It’s not that no one wanted to make markets; it’s that you can’t price what you can’t mark.

In a unified-margin regime, collateral marks flow straight into the math for liquidation thresholds. If WBETH is valued off a thin, dislocated spot print rather than its redeemable ETH value, your cross-portfolio buffer can vanish in seconds, even if your directional book is fine.

This is why many basis (delta neutral) traders still got wrecked, especially those with high leverage as they quickly learned about ADL.Forced liquidations then hit books already thin on the bid, pushing prints further from fair and propagating the error into everyone else’s “index” via cross-venue references, which sounds good in theory, but as explained above, is flawed when the leader goes bust.

From a market maker’s (MM) point of view, the decision tree was brutal but quite an easy decision. Try to make a market but risk going bust or pull liquidity?

When your collateral present value (PV) and cross-venue mid diverge from reality, value at risk (VaR) explodes and your kill-switches trip.

This compounded with API/chain congestion, wallet throttles, and venue halts. MMs often couldn’t move collateral or lay off basis even if they noted the mispricing and wanted to get out. This is why some MMs fared better than others.

Lastly on MMs, contrary to CT, market making in that type of environment is massively -ev for these market makers. That’s why many desks yanked liquidity late, widening spreads further, and lived to re-enter once feeds normalized and collateral marks were patched.

On venue performance: it’s fair to note @HyperliquidX remained up (users are still hot about ADL), @Lighter_xyz was down for ~4.5 hours, @paradex was down for ~1 hour, and several centralized venues had intermittent issues amid the cascade.

But uptime really isn’t the primary point here. It is reference/pricing/quote integrity and microstructure flaws on Binance’s side and other venues over-indexing on Binance’s prices. How is a team, Binance, that has been in the industry for 8 years still mispricing assets?

They price their wrapped assets at spot market price and not underlying value price. Marking them to thin spot prints instead of underlying redemption value is a first-principles error.

If the system’s “price of record” is wrong, the rational market-maker response is to just pull all liquidity, which is smart for them, and even the best-engineered matching engine can’t conjure fills out of risk-model uncertainty.

Zooming out: could a big Binance-focused MM have gone belly-up? I think so. The combination of (a) collateral PV shock from mis-marked wrapped assets, (b) inability to mobilize margin, and (c) stale/broken APIs is exactly the recipe that flips well-behaved delta books into forced-liquidation machines.

We’ll know more when desks publish their post-mortems; for now, my opinion is that this largely stems from Binance.

Last, on near-term flow and the macro overlay: Monday and Tuesday pose serious mark-to-market risk for traditional funds, as dealers who manage margin will need to crystallize losses. A surprise détente headline can always rip risk higher and, perversely, with a large cohort of six- to eight-figure crypto traders now structurally sidelined, the pain trade may indeed be up.

However, I also see the other side: “Hey, the market puked; I’m piling all my cash in for the meteoric rise and a resumption of ‘up-only season,’” only to watch the wick get filled in the direction no one wants to see.

Either way, I think in order to step into the market with bids in a meaningful way you need to assume Trump and Xi laugh it off and shake hands, which who knows, might already be happening.

English

app.upshift.finance They raised $16M with a TVL of $360M - Upshift is launched and powered by

@august_digital Deposit and earn points!

English

@ZssBecker Top 3 comments that like and retweet will get a share of the allocation. Paste your sol addy below

4rG1AzeJqjKzKhm7KyiCSMVdDzTZNe1CaMqjz6w6V9nn

English

@SajwaniCrypto Nice one ser 8DKPMZfUef3FHUDKCkbvzTMGVmWDgd26FySLzvBtokDC

Indonesia

TheYieldFarmer retweetledi

Bera without OPSEC risks losing their NFTs and precious HONEY, consider that @berachain mainnet is close. That turns every win Bera got into a potential loss.

That’s why as a Bera like you should care.

mirror.xyz/holisticbera.e…

English

TheYieldFarmer retweetledi

Made bags with $MEW?

Cabbage AI Feed flagged it as a green-win at $6M MCap.

A whopping 186x, according to the ATH. 🤯

What if you could also identify such wins early? Here’s your shot:

> Follow @cabbagedotapp

> Like + 🔃 RT this tweet

> Sign up for the waitlist using this link: cabbage.app/?ref=wod5jb9k

English

TheYieldFarmer retweetledi

TheYieldFarmer retweetledi