Sabitlenmiş Tweet

Thogdad

4.5K posts

Thogdad

@thogdad

Northerner. Creator. Maverick.

In people’s heads Katılım Aralık 2011

57 Takip Edilen68K Takipçiler

I have shifted most of my portfolio activity to the paid section, but as a little Christmas gift, I will reveal my next big bet, $Nexa Resources, which accounts for over 60% of my portfolio. I expect a shortage in the supply of this stock. The skyrocketing EBITDA is attracting investors like moths to a flame, and the free float is shrinking rapidly. The company is a leading zinc and silver producer, owned by a Brazilian billionaire dynasty, with vertically integrated smelting. And zinc is something that no one is paying attention to right now. Because it seems boring. But that will change soon, especially in combination with silver. Zinc is where silver was a few months ago, on the verge of a breakout. People also forget that not only silver benefits from future battery demand, zinc-ion batteries are also projected to grow significant in market share.

English

Nexa Resources $NEXA Deep Dive: The 2026-2028 Transformation

1/11: 🏆Since my last update on $NEXA, followers who got in early have already banked ~100% returns.

But here’s the kicker: we are just getting started. This stock still has massive gas in the tank, and I’m dedicated to bringing my followers even more high-conviction alpha like this. Let’s break down why the next leg up is imminent.

2/11: The 2025 Foundation

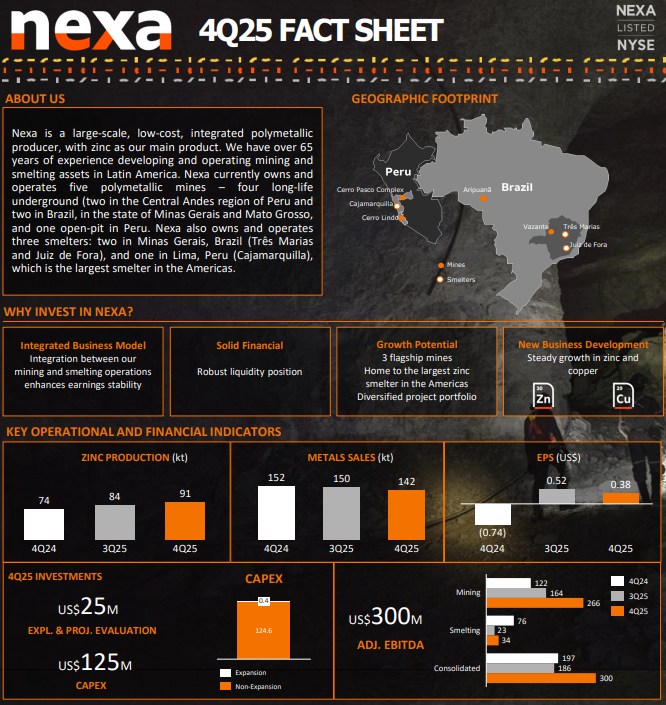

Nexa confirmed they hit all 2025 targets:

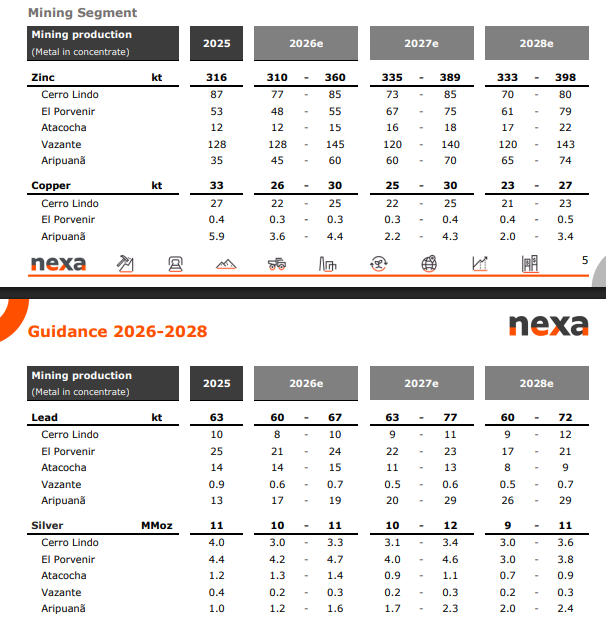

316kt Zinc, 33kt Copper, and 11MMoz Silver.

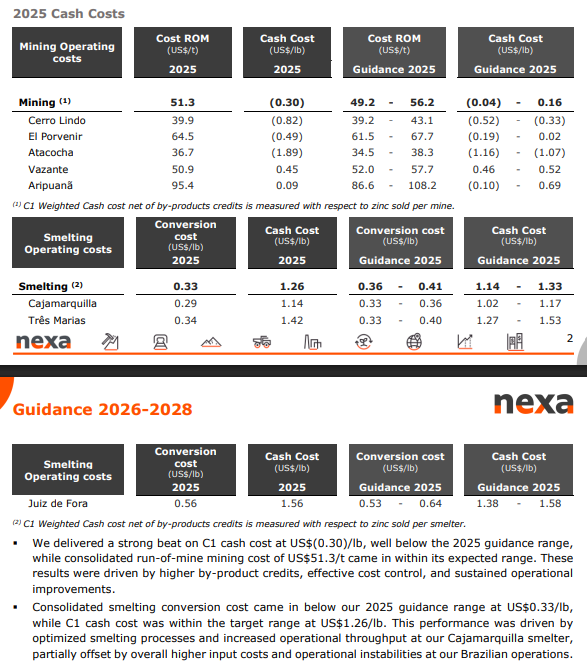

A key highlight was the Mining C1 cash cost, which ended 48% below guidance due to operational efficiencies and higher by-product credits.

3/11: Strategic Valuation Snapshot

$NEXA is currently a massive deep-value play. While the market waits for Q1 results, the valuation multiples are hitting historical lows relative to the current commodity rally.

Share Price: ~$10.40

Market Cap: ~$1.38B

Net Debt: ~$1.15B

Enterprise Value (EV): ~$2.53B

EV/EBITDA 2026e: ~2.7x (vs. Industry avg of 5-6x)

4/11: EBITDA & Net Profit Forecast (2026–2028)

Based on today's spot prices

($Zn: 1.51/lb | $Cu: 5.94/lb | $Ag: 83.60/oz) and adjusted for silver royalties:

2026e: EBITDA: $920M | Net Profit: $440M

2027e: EBITDA: $1,150M | Net Profit: $590M

2028e: EBITDA: $1,180M | Net Profit: $610M

5/11: The Guidance vs. Reality Gap

Official 2026 guidance is based on conservative price assumptions:

Zinc: $1.29/lb (Current Spot: ~$1.51)

Copper: $4.54/lb (Current Spot: ~$5.94)

Silver: $42.0/oz (Current Spot: ~$83.60)

The delta between Nexa's "Plan" and "Today's Market" suggests a massive earnings beat is coming.

6/11: The Silver Royalty Nuance ⚠️

Critically, Nexa has streaming agreements (e.g., at Cerro Lindo) where a portion of silver is sold at fixed lower prices. Even with this "royalty drag," the remaining "Free Silver" at $80+ creates a parabolic FCF boost that is not yet priced in.

7/11: Aripuanã – From Ramp-up to Cash Cow

Zinc production at Aripuanã is guided to surge +49% in 2026 (45-60kt). With the 4th tailings filter online and plant stability achieved, this asset finally moves from a CapEx drain to a major EBITDA contributor.

8/11: Smelting Recovery

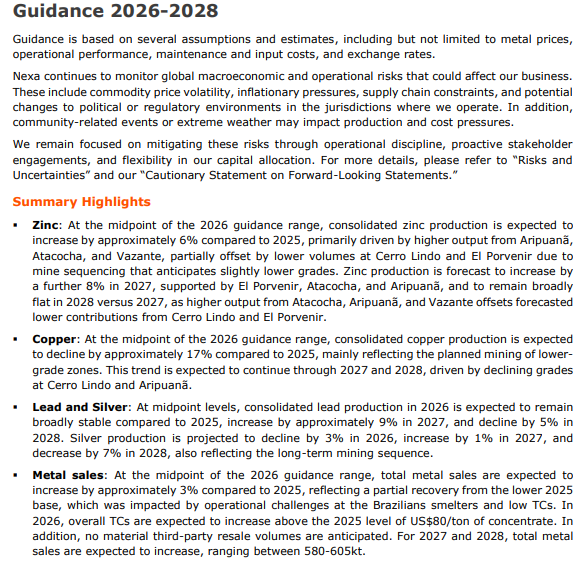

Smelting metal sales are projected to grow to 570-600kt in 2026. More importantly, Nexa assumes Treatment Charges (TCs) will recover to ~$175/t from 2025 lows of $80/t, significantly improving margins at the Brazilian smelters.

9/11: Disciplined Capital Allocation

2026 CapEx is set at $381M. Nexa is focusing on mine development ($122M) to extend the life-of-mine at Vazante and Aripuanã, ensuring long-term production stability.

10/11: Investment Verdict

Nexa is trading at a P/E of <3.2x based on my 2026 Net Profit estimates. The vertical integration (mines + smelters) provides a unique hedge that pure-play miners lack.

Rating: STRONG BUY

Price Target: $18.50 (+78% Upside)

11/11: Summary for $NEXA Bulls

Operational stability + Production growth at Aripuanã + Commodity price explosion = A massive re-rating candidate.

The market is sleeping on the "Silver & Gold" credits. Once the FCF starts hitting the balance sheet, the stock won't stay at $10. Stay tuned for more deep dives! 🚀⚒️

#NEXA #Zinc #Silver #Copper #ValueInvesting #Mining @the_analyst_24

Not a financial advise. Do your own DD.

The Analyst@the_analyst_24

$NEXA I've found an opportunity for a cheap #commodity investment and good #inflation protection with a mining stock. Nexa Resources S.A. Market Cap: US$ 927 mm Net Dept: US$ 1,479 mm EV: US$ 2.406 mm Adjusted EBITDA Q3/2025: US$ 186 mm My forecast for 2026 minimum: US$ 800 mm EV/EBITDA 2026: 3 ⛏️ Nexa Resources S.A.'s business model is an integrated approach: Mining: Extracts key metals (mainly #zinc, #copper, #lead, #silver) from polymetallic mines primarily in Brazil and Peru. #Smelting: Processes the mined ore into refined metals (zinc ingots, copper cathodes). Sales: Supplies these refined products and by-products to various global industries (construction, automotive, electronics). This 'mine-to-metal' strategy maximizes value creation and manages the supply chain! #Mining #Zinc #Commodities

English

EARNINGS ARE OUT: $NEXA

The wait is over. Nexa Resources $NEXA just released its FY2025 results, and as I predicted in my previous thread—where early followers already banked a ~100% return—the "Green Giant" is officially waking up.

If you thought the run was over, think again. The delta between these results and the 2026-2028 outlook is one of the biggest alpha opportunity in the mining sector right now.

Here is the full post-earnings breakdown. 🧵👇

1️⃣ The 2025 Foundation: A "Clean Beat"

Nexa confirmed they hit the upper end of all 2025 targets:

✅ Zinc: 316kt | Copper: 33kt | Silver: 11MMoz.

Most importantly: Mining C1 cash costs came in 48% below guidance at -$0.30/lb bcs of by Products.

Yes, negative! This is a low-cost machine firing on all cylinders.

The "Negative Cash Cost" Explained

In the mining industry, "Cash Cost (C1)" is a standard metric used to measure the cost of producing the primary metal (in Nexa's case, Zinc). The "negative" value occurs due to the By-Product Credit Accounting.

The Logic:Nexa doesn't just mine Zinc. In the same ore, they find Silver, Gold, Copper, and Lead. When they sell these "by-products," the revenue generated is subtracted from the total production cost of the Zinc.

If the revenue from Silver and Gold is higher than the actual cost of mining and processing the entire ton of ore, the cost for the Zinc effectively drops below zero. Essentially, the Silver and Gold pay for the entire operation, and the Zinc is produced "for free" plus a profit margin.

2️⃣ Valuation Snapshot: Deep Value in Plain Sight

Despite the strong numbers, $NEXA is trading like a "distressed" asset while commodities are at record highs.

• Share Price: ~$12.02 (Spot)

• Market Cap: ~$1.59B

• Net Debt: ~$1.18B (Aggressive deleveraging)

• Enterprise Value (EV): ~$2.77B

• EV/EBITDA 2026e: ~1.8x (vs. Industry avg of 5-6x)

3️⃣ The "Guidance vs. Spot" Massive Delta

Nexa’s official 2026 outlook is incredibly conservative. Look at the gap:

🔹 Zinc: Guidance ~$1.30/lb vs. Spot ~$1.51/lb

🔹 Copper: Guidance ~$4.50/lb vs. Spot ~$5.94/lb

🔹 Silver: Guidance ~$42/oz vs. Spot ~$83.60/oz

The market is pricing a "Plan," but the reality is a massive earnings explosion.

4️⃣ EBITDA & Net Profit Forecast (2026–2028)Adjusting for the silver streaming thresholds (Cerro Lindo), here is the trajectory:

💰 2026e: EBITDA: $1.5B | Net Profit: $550M+

💰 2027e: EBITDA: $1.8B | Net Profit: $720M+

💰 2028e: EBITDA: $1.9B | Net Profit: $780M+

5️⃣ The Silver Catalyst: The Threshold is Near

In 1H 2026, Nexa will hit its 19.5M oz delivery threshold. After this, the silver share for the streamer drops from 65% to 25%. Nexa will suddenly sell 75% of its silver at $80+ spot instead of discounted prices. This is a massive FCF pivot that the street hasn't fully modeled yet.

6️⃣ Aripuanã: From Drain to Cash Cow

The "Problem" is no more. Zinc production at Aripuanã is guided to surge +49% in 2026. With the 4th tailings filter online and plant stability achieved, this asset is finally an EBITDA contributor.

7️⃣ Smelting Recovery & Vertical Integration

Nexa isn't just a miner; it's a refiner. Smelting sales are projected at 570-600kt. With Treatment Charges (TCs) expected to recover, the margins at the Brazilian smelters are set to expand significantly.

8️⃣ Capital Allocation & Dividends

2026 CapEx is disciplined ($381M). With the authorized $400M buyback program and surging FCF, Nexa is perfectly positioned to reward shareholders while wiped-out debt.

9️⃣ Investment Verdict: STRONG BUY

Nexa is trading at a forward P/E of <3x. In a world of overvalued tech, this is a fundamental fortress.

🎯 Price Target: $22.00 (+80% Upside)

🔟 Summary for $NEXA Bulls

Operational stability + Aripuanã ramp-up + Silver/Copper explosion = The perfect storm for a re-rating.

My last call was a 2-bagger. This setup for 2026 looks even stronger. Don't sleep on the "Precious Metals" credits. Once the Q1 cash flow hits the balance sheet, this stock won't be at $12.

#NEXA #Zinc #Silver #Copper #ValueInvesting #Mining #Earnings #Stocks #Commodities #Gold #Deleveraging

The Analyst@the_analyst_24

Nexa Resources $NEXA Deep Dive: The 2026-2028 Transformation 1/11: 🏆Since my last update on $NEXA, followers who got in early have already banked ~100% returns. But here’s the kicker: we are just getting started. This stock still has massive gas in the tank, and I’m dedicated to bringing my followers even more high-conviction alpha like this. Let’s break down why the next leg up is imminent. 2/11: The 2025 Foundation Nexa confirmed they hit all 2025 targets: 316kt Zinc, 33kt Copper, and 11MMoz Silver. A key highlight was the Mining C1 cash cost, which ended 48% below guidance due to operational efficiencies and higher by-product credits. 3/11: Strategic Valuation Snapshot $NEXA is currently a massive deep-value play. While the market waits for Q1 results, the valuation multiples are hitting historical lows relative to the current commodity rally. Share Price: ~$10.40 Market Cap: ~$1.38B Net Debt: ~$1.15B Enterprise Value (EV): ~$2.53B EV/EBITDA 2026e: ~2.7x (vs. Industry avg of 5-6x) 4/11: EBITDA & Net Profit Forecast (2026–2028) Based on today's spot prices ($Zn: 1.51/lb | $Cu: 5.94/lb | $Ag: 83.60/oz) and adjusted for silver royalties: 2026e: EBITDA: $920M | Net Profit: $440M 2027e: EBITDA: $1,150M | Net Profit: $590M 2028e: EBITDA: $1,180M | Net Profit: $610M 5/11: The Guidance vs. Reality Gap Official 2026 guidance is based on conservative price assumptions: Zinc: $1.29/lb (Current Spot: ~$1.51) Copper: $4.54/lb (Current Spot: ~$5.94) Silver: $42.0/oz (Current Spot: ~$83.60) The delta between Nexa's "Plan" and "Today's Market" suggests a massive earnings beat is coming. 6/11: The Silver Royalty Nuance ⚠️ Critically, Nexa has streaming agreements (e.g., at Cerro Lindo) where a portion of silver is sold at fixed lower prices. Even with this "royalty drag," the remaining "Free Silver" at $80+ creates a parabolic FCF boost that is not yet priced in. 7/11: Aripuanã – From Ramp-up to Cash Cow Zinc production at Aripuanã is guided to surge +49% in 2026 (45-60kt). With the 4th tailings filter online and plant stability achieved, this asset finally moves from a CapEx drain to a major EBITDA contributor. 8/11: Smelting Recovery Smelting metal sales are projected to grow to 570-600kt in 2026. More importantly, Nexa assumes Treatment Charges (TCs) will recover to ~$175/t from 2025 lows of $80/t, significantly improving margins at the Brazilian smelters. 9/11: Disciplined Capital Allocation 2026 CapEx is set at $381M. Nexa is focusing on mine development ($122M) to extend the life-of-mine at Vazante and Aripuanã, ensuring long-term production stability. 10/11: Investment Verdict Nexa is trading at a P/E of <3.2x based on my 2026 Net Profit estimates. The vertical integration (mines + smelters) provides a unique hedge that pure-play miners lack. Rating: STRONG BUY Price Target: $18.50 (+78% Upside) 11/11: Summary for $NEXA Bulls Operational stability + Production growth at Aripuanã + Commodity price explosion = A massive re-rating candidate. The market is sleeping on the "Silver & Gold" credits. Once the FCF starts hitting the balance sheet, the stock won't stay at $10. Stay tuned for more deep dives! 🚀⚒️ #NEXA #Zinc #Silver #Copper #ValueInvesting #Mining @the_analyst_24 Not a financial advise. Do your own DD.

English

English

Thogdad retweetledi

Hull, England 🇬🇧 English

@shearer_LFC Been a solid 7.0 until recently to be fair. Now I’m pouring it away.

English

@thogdad If Southgate was a pint what would your out of ten be?

English

Thogdad retweetledi