💸 Jon 💸@traderjon01

$ASTS (AST SpaceMobile Inc) - the stock retail loves & is the most bullish on. Here's why it's a fan favorite! 🧵

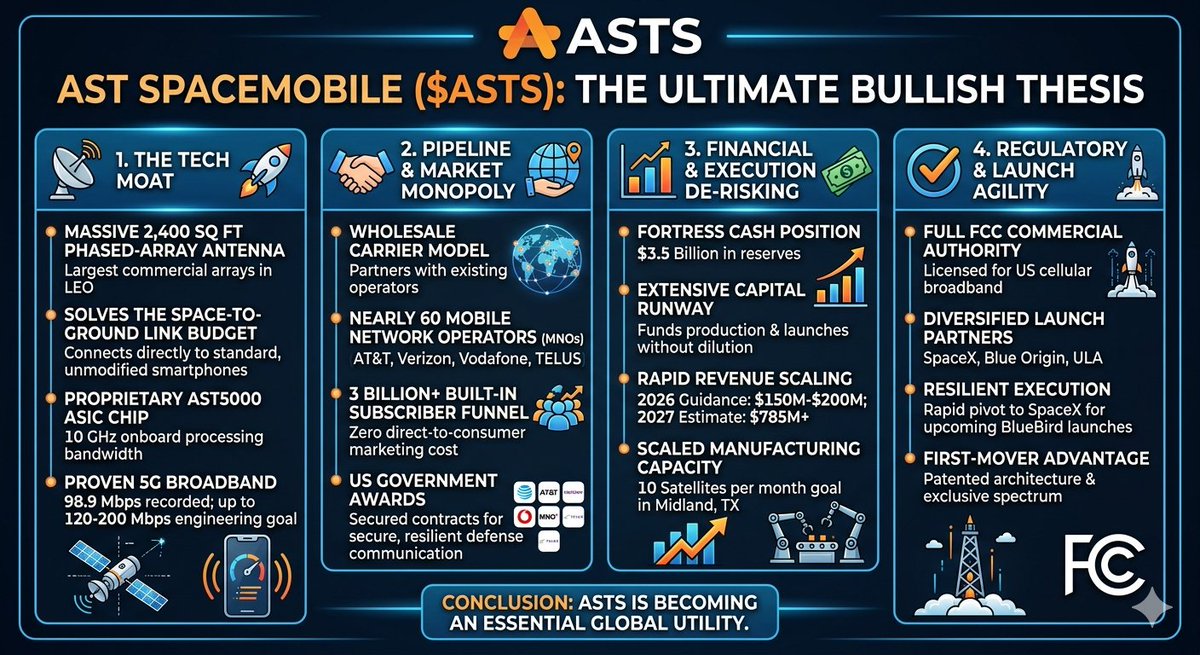

THE TECH

The real due diligence isn’t just about "satellites in space"—it’s about the sheer physical scale and proprietary silicon architecture.

* The Block 2 BlueBird satellites feature a massive 2,400-square-foot phased-array antenna aperture (the largest commercial arrays ever in LEO). This size solves the fundamental link-budget problem of space-to-ground physics, allowing a satellite hundreds of miles away to connect directly to standard, unmodified smartphones.

* Powering this is the proprietary AST5000 ASIC chip, giving each satellite an incredible 10 GHz of onboard processing bandwidth.

* This isn't theoretical: Recent tests hit peak download speeds of 98.9 Mbps using Block 1 directly to standard phones. Block 2 is engineered to push 120 Mbps to 200 Mbps per coverage cell. We are talking true 5G broadband streaming, video, and heavy data not just low-bandwidth emergency text messaging.

THE COMMERCIAL & GOVT PIPELINE

ASTS isn't competing with traditional wireless providers; it’s acting as their neutral wholesale carrier. They have built an exclusive tollbooth on a massive global subscriber base with zero direct-to-consumer marketing costs.

* The MNO Ecosystem: Partnered with nearly 60 Mobile Network Operators globally (AT&T, Verizon, Vodafone, TELUS). MNOs integrate the service directly into existing billing plans (like a $10/mo "everywhere coverage" add-on) and split the high-margin revenue with ASTS. This gives them a built-in acquisition funnel of over 3 billion subscribers.

* The Hidden DD (Government Backlog): While retail focuses on consumer cellular, institutional "smart money" is watching the defense applications. ASTS quietly secured three new US Government awards via prime contractors. This secure, space-based cellular network gives the military resilient communication lines that don't rely on vulnerable ground infrastructure, creating a massive, high-margin dual-revenue stream.

THE BALANCE SHEET

The classic bear case against pre-revenue space tech is constant dilution. The Q1 2026 update essentially shattered that narrative:

* Fortress Cash: $3.5 Billion in cash reserves as of March 31, 2026. This massive capital cushion provides a clear runway to fund upcoming production and multi-launch manifests without needing dilutive capital raises.

* Financial Scaling: Reaffirmed 2026 revenue guidance of $150M–$200M, scaling rapidly to a consensus estimate of $785M+ by 2027 as more hardware goes live.

* Manufacturing Cadence: The Midland, Texas facility is scaling toward a steady production cadence of 10 satellites per month with a 95% vertical integration rate. Phased arrays are completed through BlueBird 28, with units 11 through 33 already in advanced assembly.

REGULATORY & LAUNCH AGILITY

* The Ultimate De-Risk: The FCC officially granted AST SpaceMobile full commercial authority to deliver direct-to-device cellular broadband across the United States.

* Execution Agility: After the Blue Origin upper-stage engine failure sidelined BlueBird 7, management didn't skip a beat. They rapidly shifted to a SpaceX Falcon 9 for a mid-June launch of BlueBirds 8, 9, and 10. It proved ASTS is diversified and not single-threaded to a single rocket provider's delays. Their launch strategy spans SpaceX, Blue Origin's New Glenn, and ULA’s Vulcan Centaur.

While competitors are still testing or restricted to basic text messaging, ASTS holds a massive first-mover advantage rooted in proprietary cellular spectrum agreements and patented, giant phased-array architecture. Building 2,400 sq. ft. arrays at scale creates an incredibly barrier to entry.

ASTS is successfully executing the pivot from a speculative lab project to an essential global utility.

Peers: $GSAT (Globalstar) $SATS (EchoStar) $IRDM (Iridium Communications) $RKLB (Rocket Lab) $LUNR (Intuitive Machines) $PL (Planet Labs) $SPIR (Spire Global)