When portfolios come under pressure, criticism naturally increases. That is not always easy to read, but it can still be useful. One recent comment suggested moving half the portfolio into bonds, cash and gold until the macro picture becomes clearer.

I am not going to do that, but it did raise an important question: is the portfolio clearly positioned for the current environment?

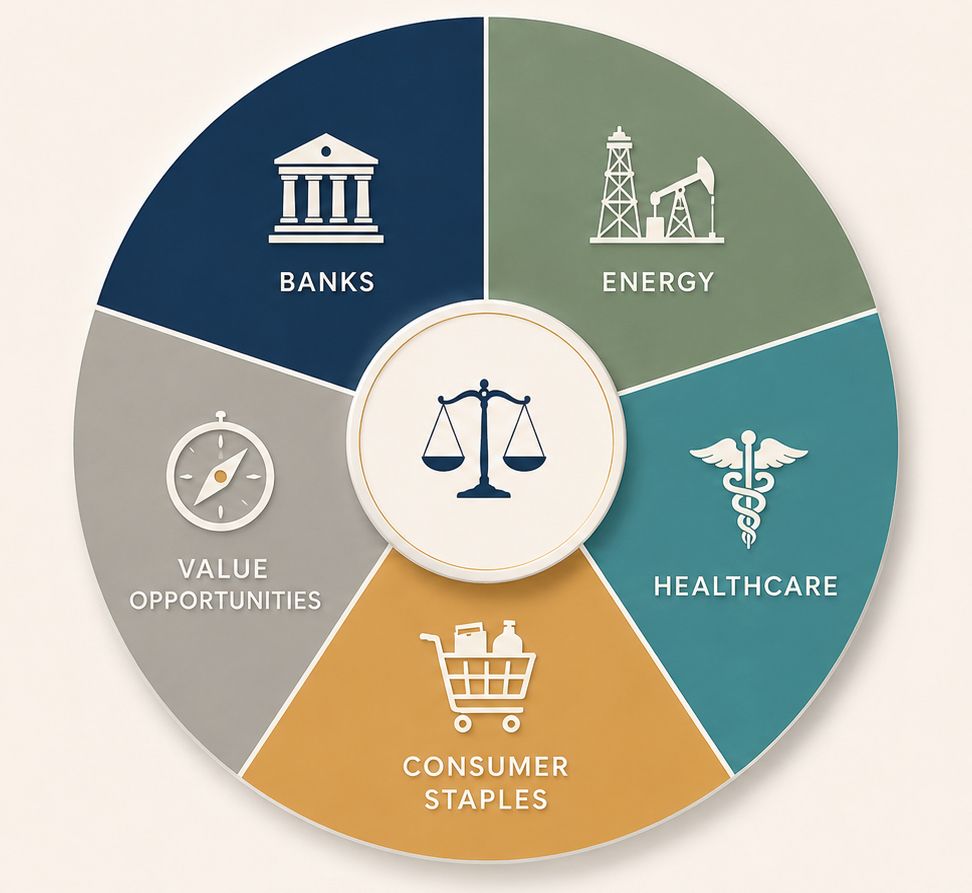

At the moment, the portfolio is split into five equal buckets:

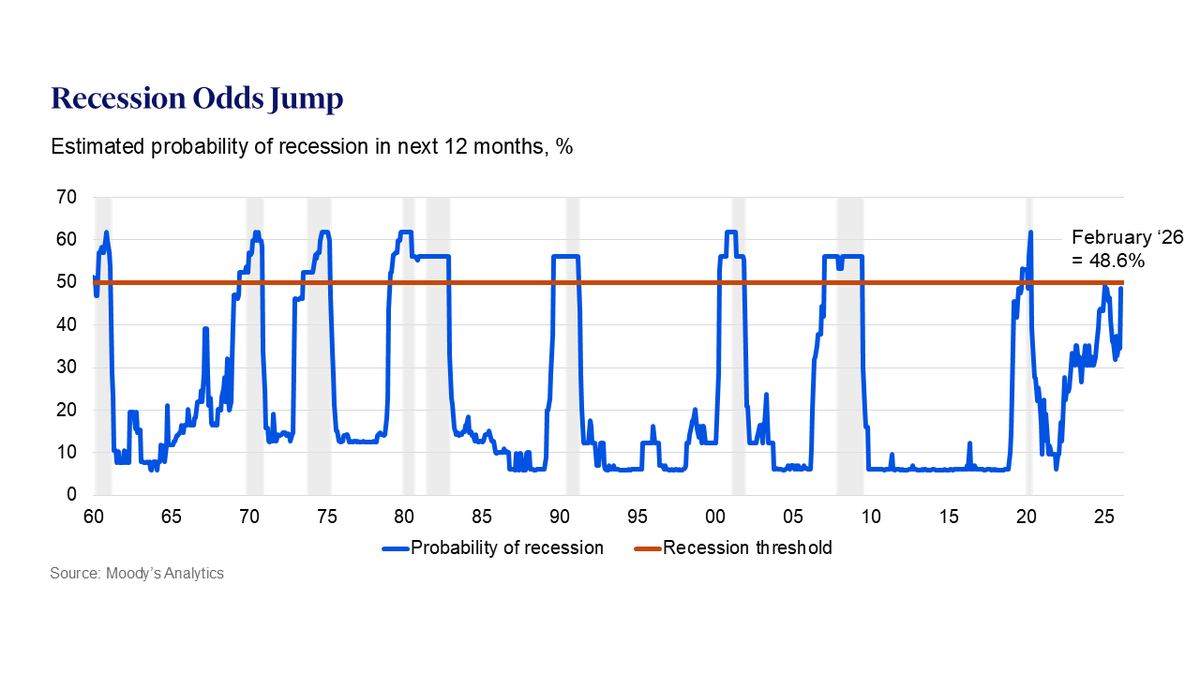

• Banks (20%) – positioned for improving growth and easing recession fears

• Oil & oil-related (20%) – reflects the persistent impact of the Strait of Hormuz disruption on energy markets

• Healthcare (20%) – adds resilience if growth weakens and stagflation risks rise

• Consumer Staples (20%) – provides defensive exposure in a slower-growth, higher-inflation environment

• Other value opportunities (20%) – diversified holdings where valuations remain attractive

Just as important is what the portfolio does not own.

I remain underweight Technology, especially Hardware, because I do not believe I have a strong enough edge there. I am also underweight Real Estate, given the risk that interest rates stay higher for longer, which could pressure valuations.

Overall, the portfolio is positioned for two broad outcomes:

• Inflationary boom – through Banks and Oil

• Stagflation – through Healthcare and Staples

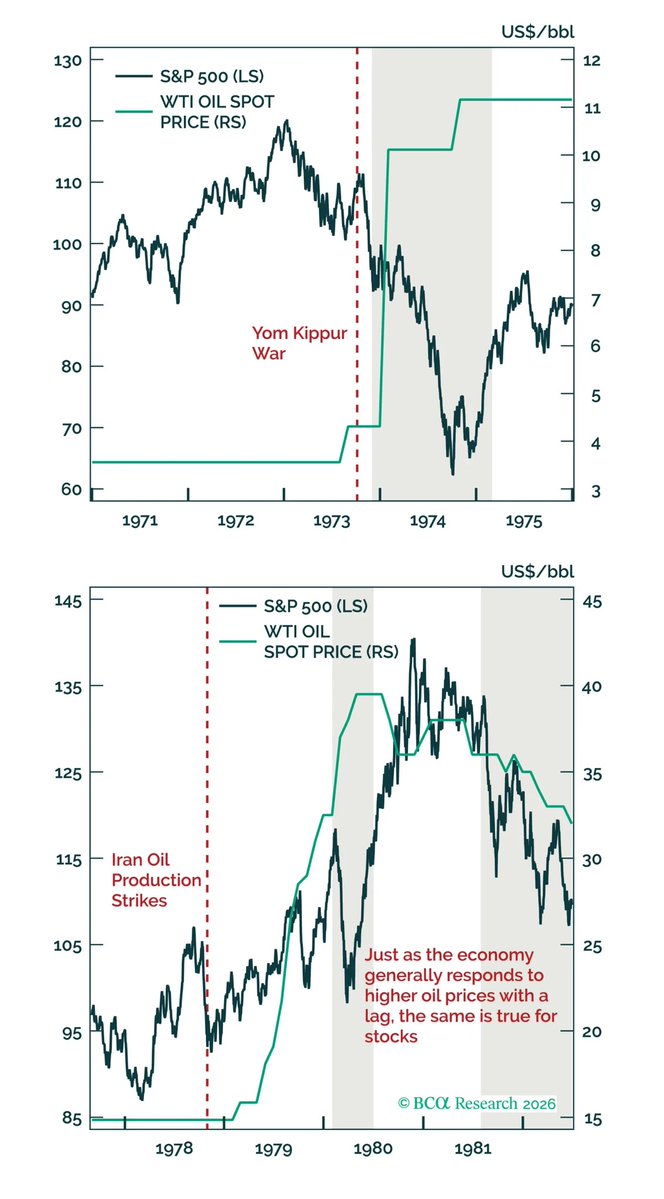

If the Hormuz situation improves materially, it may make sense to reduce some defensive exposure and lean more into cyclicals. For now, balance still looks like the right approach.

#Investing #PortfolioManagement #AssetAllocation #MacroInvesting

𝘛𝘩𝘪𝘴 𝘤𝘰𝘯𝘵𝘦𝘯𝘵 𝘪𝘴 𝘧𝘰𝘳 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘰𝘯𝘭𝘺. 𝘐𝘵 𝘪𝘴 𝘯𝘰𝘵 𝘢𝘯 𝘰𝘧𝘧𝘦𝘳 𝘰𝘳 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯 𝘵𝘰 𝘣𝘶𝘺, 𝘩𝘰𝘭𝘥 𝘰𝘳 𝘴𝘦𝘭𝘭 𝘢𝘯𝘺 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵, 𝘯𝘰𝘳 𝘭𝘦𝘨𝘢𝘭, 𝘵𝘢𝘹, 𝘰𝘳 𝘧𝘪𝘯𝘢𝘯𝘤𝘪𝘢𝘭 𝘢𝘥𝘷𝘪𝘤𝘦. 𝘗𝘢𝘴𝘵 𝘱𝘦𝘳𝘧𝘰𝘳𝘮𝘢𝘯𝘤𝘦 𝘪𝘴 𝘯𝘰𝘵 𝘪𝘯𝘥𝘪𝘤𝘢𝘵𝘪𝘷𝘦 𝘰𝘧 𝘧𝘶𝘵𝘶𝘳𝘦 𝘳𝘦𝘴𝘶𝘭𝘵𝘴.

English