🇧🇷 15y Public Equities (ex-Head of Research @ top Brazil fund). Experience w/ Alternatives & Illiquids. Former Public Co. Board Member. Tech enthusiast.

I know. The point is more directional: the most relevant clients are signing long-term supply agreements. This increases business predictability and serves as a cushion whenever the cycle normalizes. It deserves a higher multiple. Clients wouldn't be signing those contracts with they were planning towards 2028 only. The demand seems to be more structural in nature.

The memory triopoly ($MU, SK Hynix, Samsung) are all expanding capacity. Server memory is still getting tighter. Here's why.

Memory SxD tightness + hyperscalers signing long-term supply agreements means no supply glut in sight. $MU should trade closer to $NVDA, not at 8x P/E.

Hyperscalers have now committed 60-70% of industry Server DDR5 volumes under 2-3 year enhanced LTAs — fixed volume, partially fixed pricing. Companies don't sign multi-year supply agreements into an expected glut. The sector's largest buyers just voted with their contracts.

$MU

MU guided ~81% gross margins for Q3 FY26, with returns on invested capital at 35.2% — up from a loss trough in 2023. The "supercycle vs. 2028 glut" debate is looking at the wrong pool.

My assumptions:

1. HBM's factory tax: each HBM wafer consumes 3.0x the resources of regular memory today, rising to 4.1x by 2028 as the next generation (HBM4) ramps.

2. HBM's share of total production: 11.4% (2025) → 19.3% (2026) → 29.9% (2027) → 35.7% (2028) — driven by AI chip demand.

→ Net result: regular server memory production declines -4.6% in 2026, -9.0% in 2027, -3.9% in 2028 — while total factory output keeps growing at +4.8% annually.

The demand per chip is compounding. Memory per flagship NVIDIA chip, by generation:

· A100 (Ampere, 2020): 80 GB HBM2e

· H200 (Hopper, 2024): 141 GB HBM3e

· B200 (Blackwell, 2025): 192 GB HBM3e

· Vera Rubin (2026E): 288 GB HBM4

· Feynman (2028E): est. ~450 GB HBM5

~5.6x per flagship chip in eight years, or ~2.3x more memory when stacking Feynman (2028) against Blackwell (2025).

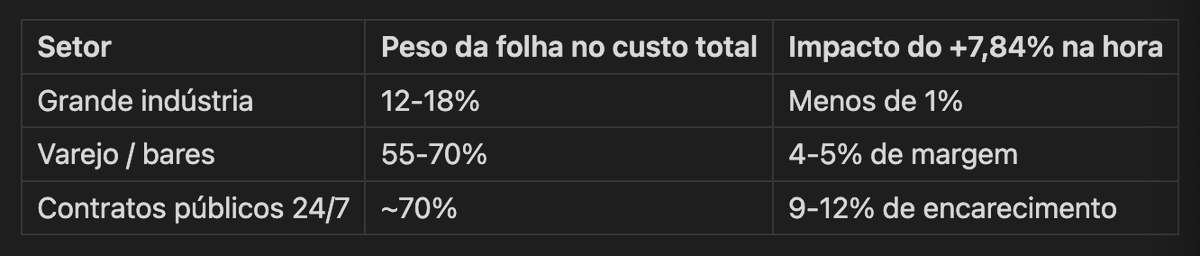

O que não dá pra modelar: a velocidade de pejotização que o MEI expandido vai induzir. Se for alta, o Estado perde INSS e FGTS ao mesmo tempo que paga mais em custeio. Ninguém calculou esse rombo acumulado ainda.

O que atenuaria o impacto:

→ Regulamentação excluir contratos públicos 24/7 do novo limite de jornada, preservando cofres públicos

→ Prazo estendido para 36+ meses pelo Senado

Se qualquer das duas ocorrer, o impacto fiscal desaparece e a tese principal cai.

O principal prejudicado pela PEC 6x1 não é o varejo. É o Tesouro Nacional: o governo é o maior contratante de vigilância e limpeza 24/7 do país, e vai pagar de 9% a 12% a mais por esses contratos. Em seguida, a $GPSS3, maior fornecedora desse tipo de mão de obra no país.