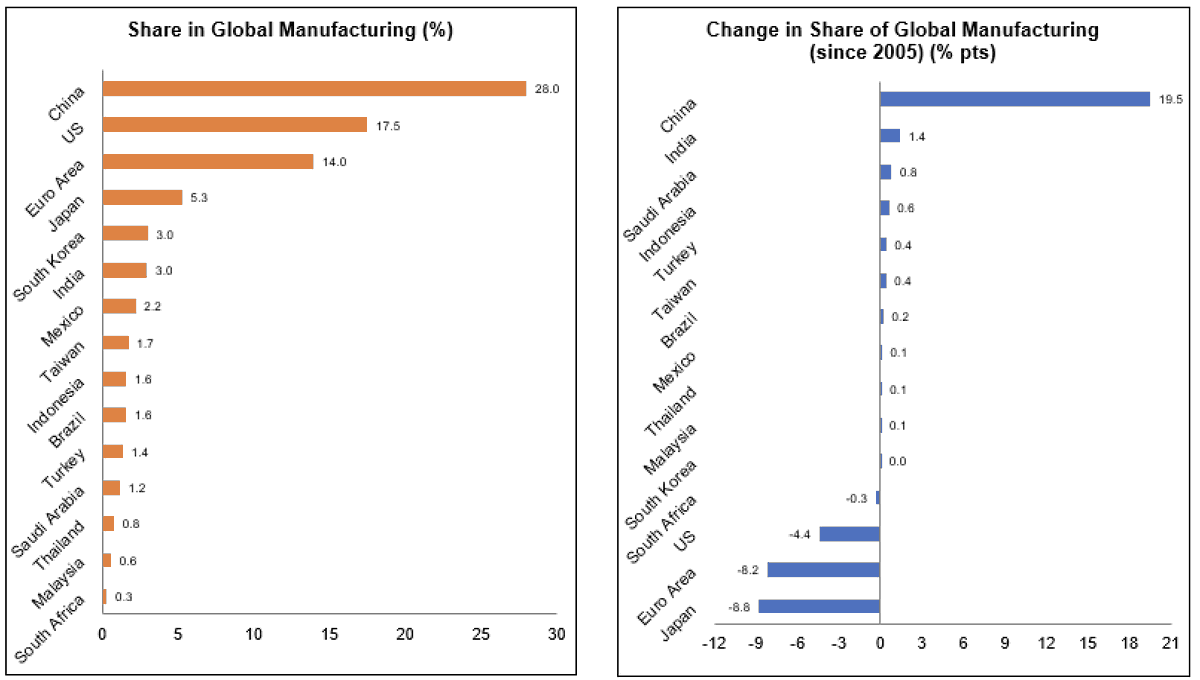

China today accounts for 28% of global manufacturing.

In the last 20 years it increased its share by a staggering 20% points. Pretty much what US, Europe and Japan lost.

No other emerging market using lower wages or tech innovation could come close to what China has achieved.

English