Sabitlenmiş Tweet

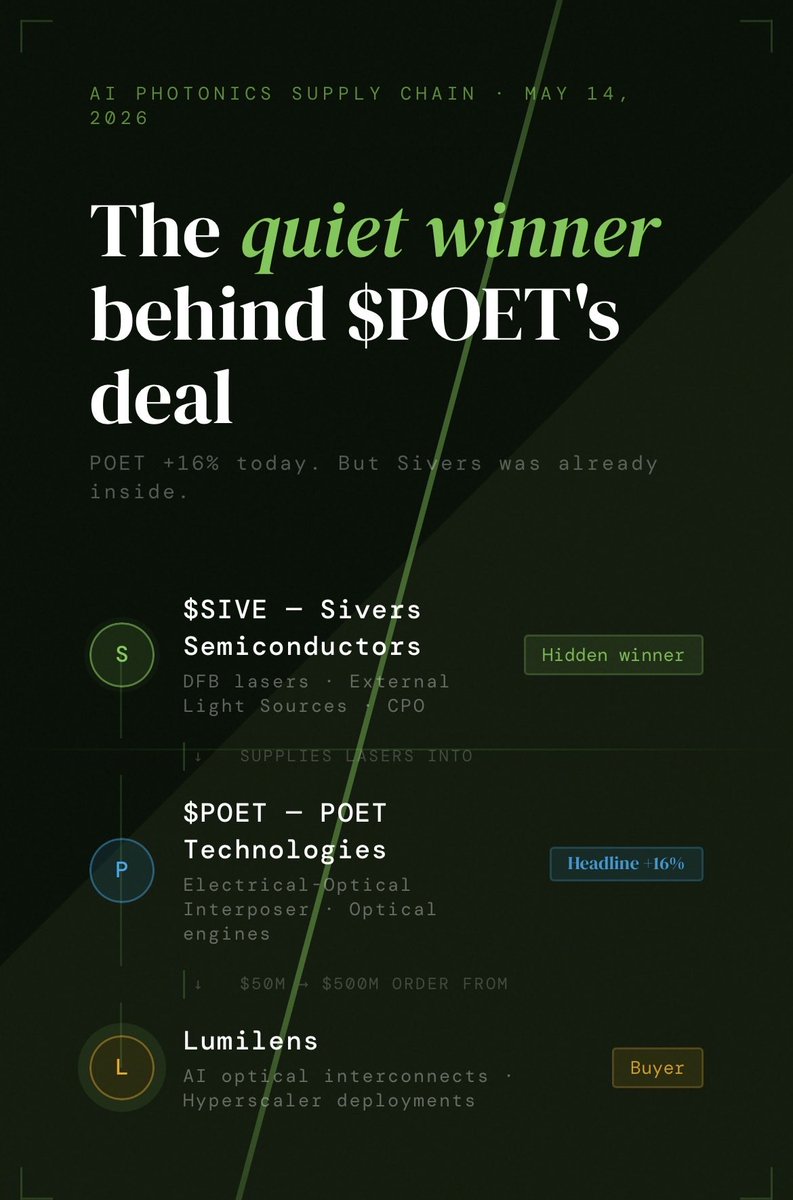

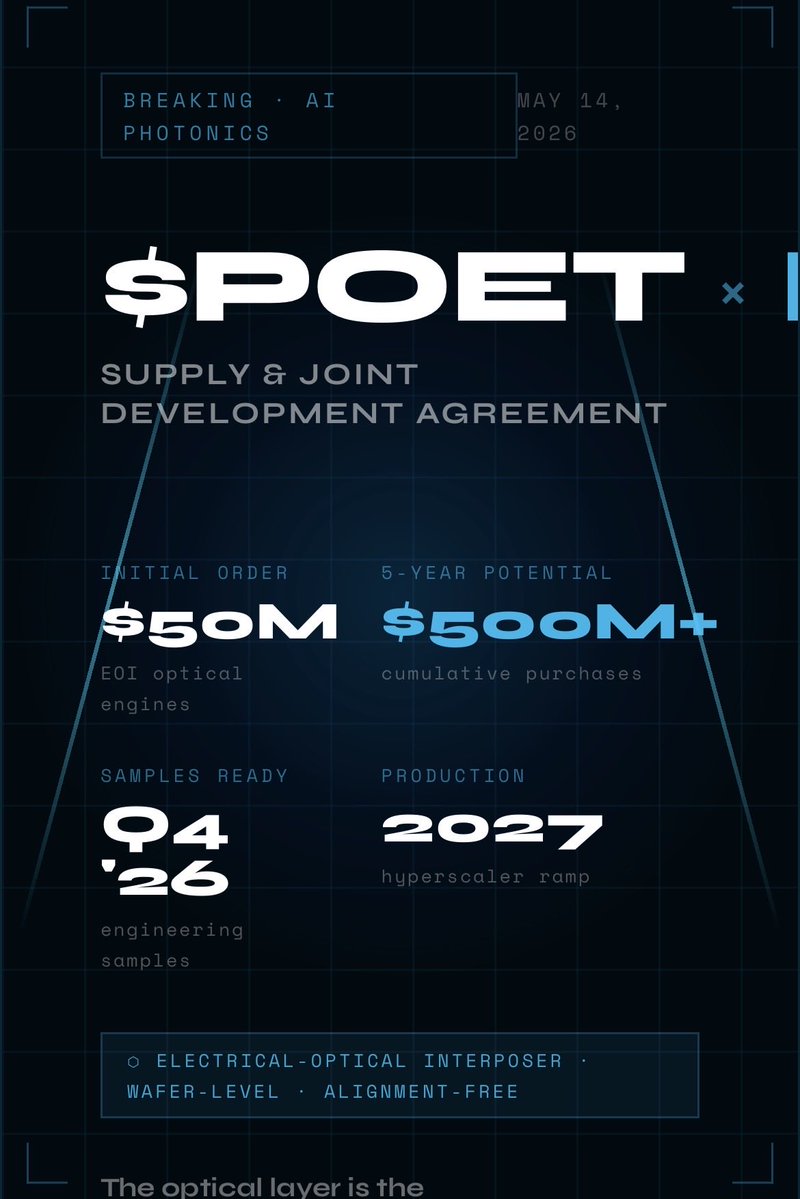

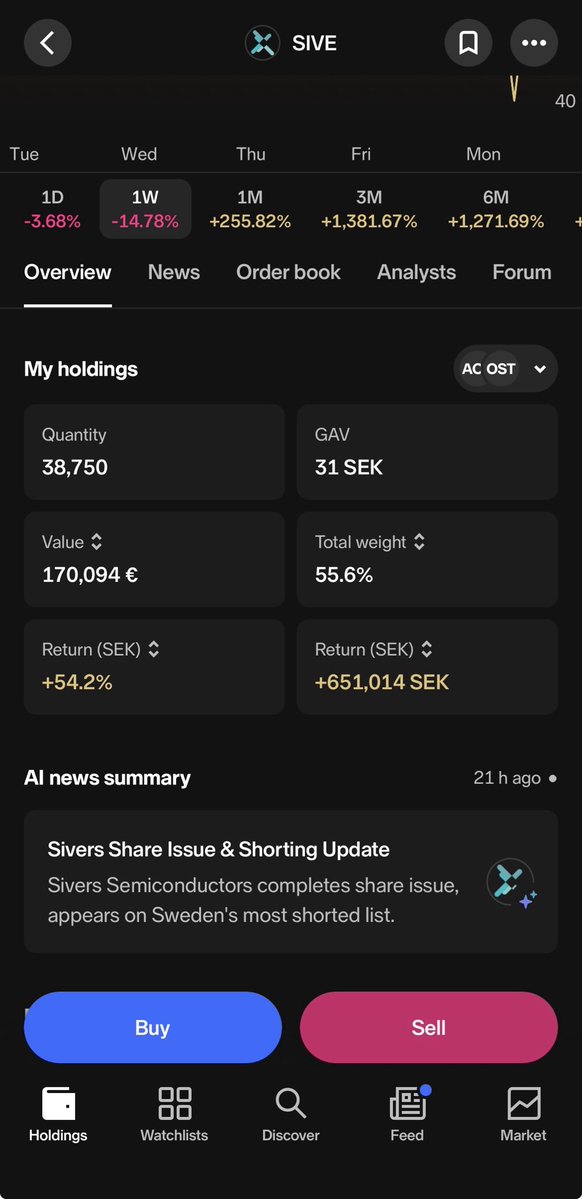

Putting money where my mouth is holding ~40k shares of $SIVE

Watch this position retire me and make me millions in a year. +$10B is only 10x from here while $LITE and $COHR are sitting at $70B

Thesis from: @aleabitoreddit

English