Bittractor

5.7K posts

Bittractor

@user889889

Entrepreneur, venture investor, strategy trader

Manhattan, NY Katılım Ocak 2016

1.5K Takip Edilen357 Takipçiler

@ilzmcfly So why is stock not green big time? What am I missing?

English

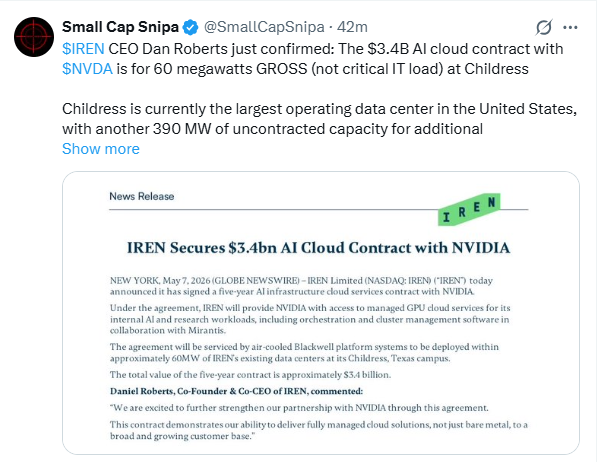

$IREN WHAT DID I DAY? 😱

The Nvidia Deal is confirmed to be 60MW Gross of Capacity by Daniel Roberts

That is 75% more than the Microsoft Deal for Air-Cooled B300's instead of Liquid Cooled GB300's

This is by far the best neo-cloud deal signed in the market.

-> Extremely Lucrative and Profitable deal with 40-50% Profit Margins.

-> First neo-cloud deal to include software/fully managed cloud solutions

Site: 250MW Air Cooled Childress for 2027

60MW Gross

- Annual price per MW Gross: $11.33M 🤯

- ARR: $680M

- PUE: 1.45 (Estimate - High end)

- Total GPU's: 22,068 (Estimate - High end)

- Total GPU costs: $1,544,760,000 for GPU's (Estimate - High end)

- Total Retrofit Costs: $4-$5M per MW (Estimate-High end)

- Total Retrofit & GPU Cost: $1.785B – $1.845B (Estimate-High end)

- Net Profit Range: $1.555B – $1.615 Billion

- Net Profit Margin: 45.7% – 47.5%

B300's and Air-Cooled Capacity

And now confirmed negotiations are underway with Hyperscaler's and Frontier labs for 2027 capacity.

Great job to $iren and the Robert Brothers. While other criticize their prior deal this is a extreme improvement and a showcase of their capabilities.

Strong deal and strong terms.🚀

McFly@ilzmcfly

The 60MW to $NVDA from $IREN seems to be in Gross MW’s Why? IREN says they are deploying the NVIDIA Blackwell chips "within 60MW of existing data center capacity." "Existing Capacity" is code for "Total Grid Power Available in our old buildings." Thus, the NVIDIA deal is almost certainly 60MW Gross. NVIDIA is hiring IREN to run their internal R&D workloads. This requires a massive software/operator layer (Mirantis) which justifies a much higher price per actual "chip-watt” Standard Air-Cooling PUE: ~1.15 to 1.20. That would mean IT load is more like 51MW which equals $13.33M per MW of IT for B300’s (Nvidia) vs the $9.7M per MW of IT for 200MW IT of B300’s (Microsoft) That would be a 37.42% Increase from the Microsoft deal 😱 In the 1-3 pictures attached you can clearly see that they refer to “existing data center capacity” as MW gross. Math: 150MW Gross referred to as 100MW IT in the second slide. 250MW existing capacity is gross because 250MW + 150MW/100MW IT= 400MW Gross left available at Childress Childress is 750MW Gross: 350MW Contracted + 400MW Available = 750MW Childress: 290MW Gross - Microsoft (LC) 60MW Gross - Nvidia (AC) 150MW - Liquid Cooled (LC) 250MW - Air Cooled (AC)

English

@perry_lin1 @TeraWulfInc So this is the last hurdle for final signing?

English

$WULF After some communication with the @TeraWulfInc team, I was informed that there were only positive intervenors (KY AG and Gov is supportive) who filed by the May 20 deadline as stipulated in the order. psc.ky.gov/order_vault/Or…

Given the lack of opposition, they expect the timeline for approval to be accelerated. Justified Data Campus is happening and a customer lease is on the way.

English

@EndicottInvests Probably they already banked another 1-2B today.

English

Only $5B more to go for $IREN ATM

Good find

Mark Hogan@MB_Hogan

$IREN UPDATE: Looks like IREN sold ~$1B of its $6B ATM at ~$43 a share issuing approximately 24M new shares

English

$WULF turns higher +4% pre

Despite no news/slight miss on press release, couple slightly optimistic anecdotes from call moving stock up

>Q1 HPC gross margins were 50% vs LT guidance of 85% for HPC, but broke down several one-timers that get you back to 85%$2.1M of tenant fit our rev and costs during 1Q

>$3.5M of pre-rev operating costs at WULF compute

>$2.1M of dev costs across 1.75GW portfolio of uncontracted dev site

>Adjusting yields 85% segment profit margin

Expects the Kentucky customer to be signed in 2Q (480MW) to be "investment grade super high quality"; hinted at expansion beyond the initial site.

Sounds like it was very competitive process and should expect 'favorable pricing terms' $WULF

English

@MktMavPro NVDA took a call option, not just a direct investment yet. but still, big leap forward for IREN.

English

$IREN falling hard from that spike... Did someone read the fine print? What's happening?

English

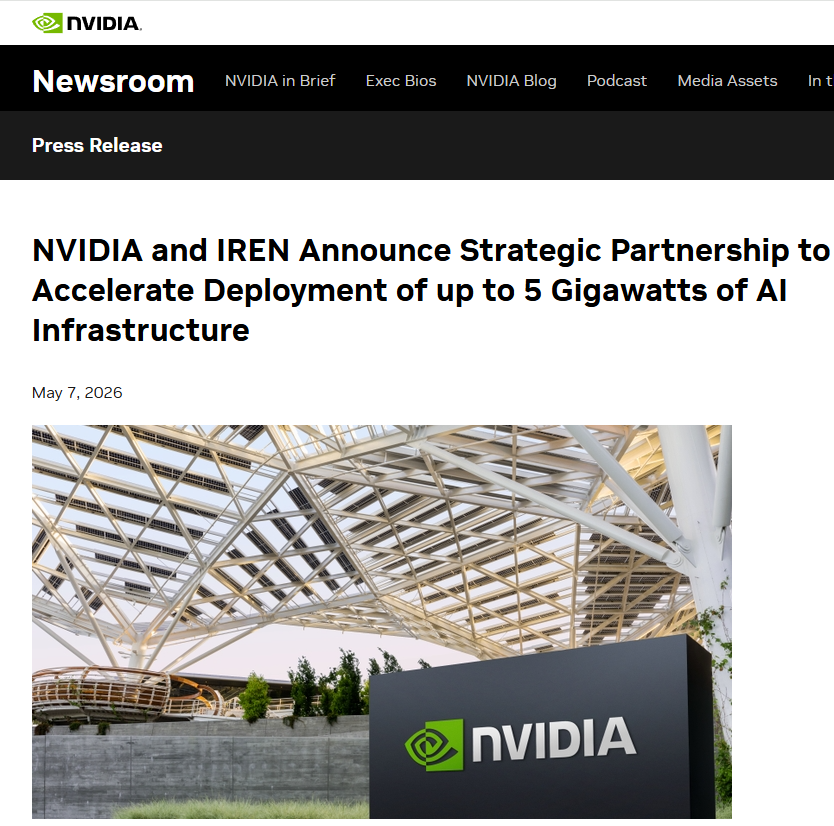

Huge news for $IREN

NVIDIA and IREN Announce Strategic Partnership to Accelerate Deployment of up to 5 Gigawatts of AI Infrastructure $NVDA

When $100 ? In May or June ?

English

@HenriVisne35246 @Alex83110581 With KY site signed, yes. Then CIFR will have OH site for 2nd half and big pipelines coming by July of ecort decision. Both are executing very well, tight race.

English

@accounting_ds the first one to sign a direct deal w/ a hyperscaler, and have more diversified clients among miners, that’s why they have better rates in debt mkt comparing to others, even comparing to wulf. Once they convert MW to revenues, that’s the real inflection pt comes, execution is key

English

@user889889 You understand more than me, which is why I value your opinion greatly, you mentioned the bond markets before, and the pricing miss match between equities

Gonna look into that more

English

Its very important to understand what you own, especially for a company like $CIFR

And not in the tacky way to rally the bulls, in the understanding how valuation works inside this specific ecosystem: power, sites, financing, tenant commitments, construction timelines, and when revenue actually begins to show up kind of way

That’s why obsessing over a “double miss” here feels low signal to me

We now need to collectively view $CIFR as a landlord company mid transition before major AI/HPC tenants start contributing meaningfully to the income statement, that backwards historical data is counting Odessa mining economics and a few other legacy pieces, not the full forward model investors are underwriting

I am not posting this to dunk on anyone, I have lost a lot of money playing different sectors I did not comprehend, for example Space, I make a lot more focusing on what I know and am passionate about, for me that is Energy, intercorrelated with AI and its buildout

HumzyTrades@HumzyTrades

How tf is $CIFR 10% up even after missing earnings A whole lotta stuffs not adding up in this markets lol

English

@HagenMikkel_ @SylentTrade Yes, they announced that weeks ago, but today we learned that the price /mw is 15% higher. Plus, all projects on time, just a few months away.

English

@SylentTrade No they didn’t.

They announced that several weeks ago.

English

$CIFR just announced they signed another deal with a hyperscaler during their earnings this morning. Don’t be surprised when $IREN announces a deal on their earnings call this thursday afternoon.

English

@user889889 Execution has been phenomenal and leadership speaks with such confidence and integrity, excited to see them execute

English

$CIFR is in a very fascinating spot

Cipher Digital marked the official business model switch, this operation is no longer even slightly correlated to $BTC mining

So now, a public company is undergoing a model change while staying public, how can we accurately forecast numbers when backwards looking data does not support the current mission of the company?

That exact inflection is where I believe significant Alpha exists

You are putting money on the team, an idea, and execution

Execution has been flawless thus far, and if it continues to be, when revenues actually begin to transform the income statement and ERCOT confirms a larger pipeline, a much stronger forecast can be made

So do you think they will be worth more than 7B by then, with 11B already contracted

Seems fairly obvious to me🤷🏻♂️

Daniel S@accounting_ds

$CIFR business update ~ Barber Lake is still on schedule✅ Black Pearl Phase I retrofitting is underway, and Phase II site/layout work began in April✅ Third AI data center campus lease with an investment grade hyperscale tenant✅ $200M corporate revolver, which gives them more liquidity and flexibility to fund the equity portion of the third campus and near term capital needs✅ $CIFR is still on timeline, still attracting hyperscale tenants, and still finding capital to fund the buildout Let’s hear what Tyler has to say, feeling very good about the business update investors.cipherdigital.com/news-releases/…

English

@MktMavPro On time delivery is everything. 700m just a few mth away.

English

Bittractor retweetledi

Good Morning All - As below: $DGXX goes BOOM.

Who is next this week I query?

$SOUN $IMSR $SHMD $CNTMD ?

My Names:

$AMZE

$INTC

$MU

$DGXX

$GLXY

$RKLB

$BMNR

$EOSE

$LAES

$SHMD

$BABA

$CNTMD

$ABVE

$DFNS

$KZIA

$TOYO

$TE

$AMPX

$PHGE

$IMSR

$RDDT

$SOUN

$SIDE (on watch for initiation)

Neil Bhatia@neilsbhatia

If Lively/Baldoni can do it … Iran mustn’t be far … As I said this morning: $SOUN $IMSR $SHMD $DGXX $CNTMD … in no particular order …

English

@accounting_ds Possible if they get 3M approval by July and market them for 2027.

English

@accounting_ds CIFR should trade at higher NOI than the rest due to their client base, this is already reflected in the debt mkt but not in equity mkt yet.

English

I think Im done trading in and out, that's what fucked my $7 basis, also Cipher is so emotionally draining to trade that I will just continue to quietly accumulate at reasonable levels, not too much to talk about on a daily basis with them anymore, pretty crystal clear they will be successful as long as things stay on course

English

Food for thought on $CIFR

Delivery begins in September this year, which should not only begin to transform their income statement but also optically validate their thesis

After the October run, it was fair to say valuation was a little rich at $25

However, after some nice business updates and confirmation of CoLo business model, its hard to say their not undervalued here

Q4 is when Black Pearl begins to deliver as well

Been better places to be this past 6 months but the time is near again

Sort of hard to be structurally bearish any DC stock with S tier clients and recurring revenue, we truly have a compute crisis in a time where somehow Data Centers have become political martyrs

Cipher Digital@CipherInc

Cipher is pleased to announce the following business updates: - Execution of a new 15-year data center campus lease with Hyperscale tenant - Closing of $200m revolving credit facility, supported by leading global financial institutions Read the full press release here: investors.cipherdigital.com/news-releases/…

English

@accounting_ds Hard to predict short term movements. CIFR WULF are good long term investments though. Price movements still volatile, but you can earn extra from selling calls.

English

@user889889 You have always been a great voice of reason and someone with a very nice cost basis

Any predictions for this week across the board? I am thinking many of these companies will move in a pac

English