Mr Blonde

206 posts

Mr Blonde

@wcrelease

swimming naked with the tide out

Katılım Nisan 2023

222 Takip Edilen131 Takipçiler

@wcrelease $MAI.V I expect to go to $17 CAD within 24 months. $PGDC.V is my portfolios slightly in the money call option on gold. If gold skyrockets, this could easily 10x or more. If gold goes flat it's a 2.5x or so.

$SU is, yes, diversification. If oil prices go over $200, miners crash.

English

Ok I DM'd 20 random finance people that all work on wall street. Consensus (14/15 replies) is Iran has no choice but to fold, they've played all their cards, impossible for them to continue.

That's what we're betting against if we buy oil ladies and gentleman.

English

Never mind… more Ackman antics… would be surprised if it moves a lot.

English

Everyone who went long and used me as a contra is welcome 🤗

$UMG

businesswire.com/news/home/2026….

Arrakis Global@ArrakisGlobal

$UMG They capitalise artist advances, catalog acquisitions and corporate M&A. The artist advances especially looks suspect to me. EBITDA meaningfully overstates the FCF to equity. Spending as a % of revenue is increasing rapidly and should not abate. Easy pass.

English

Mr Blonde retweetledi

@leevalueroach Take a look at $wulf instead, high teens unlevered returns on deals backed by Google. They’re the real operators. Granted also still in build out phase but they actually have a shot of delivering unlike $iren 3% roic deal with $msft

English

@CasinoCapital No they’re both buys, rea will also come back for rmv

English

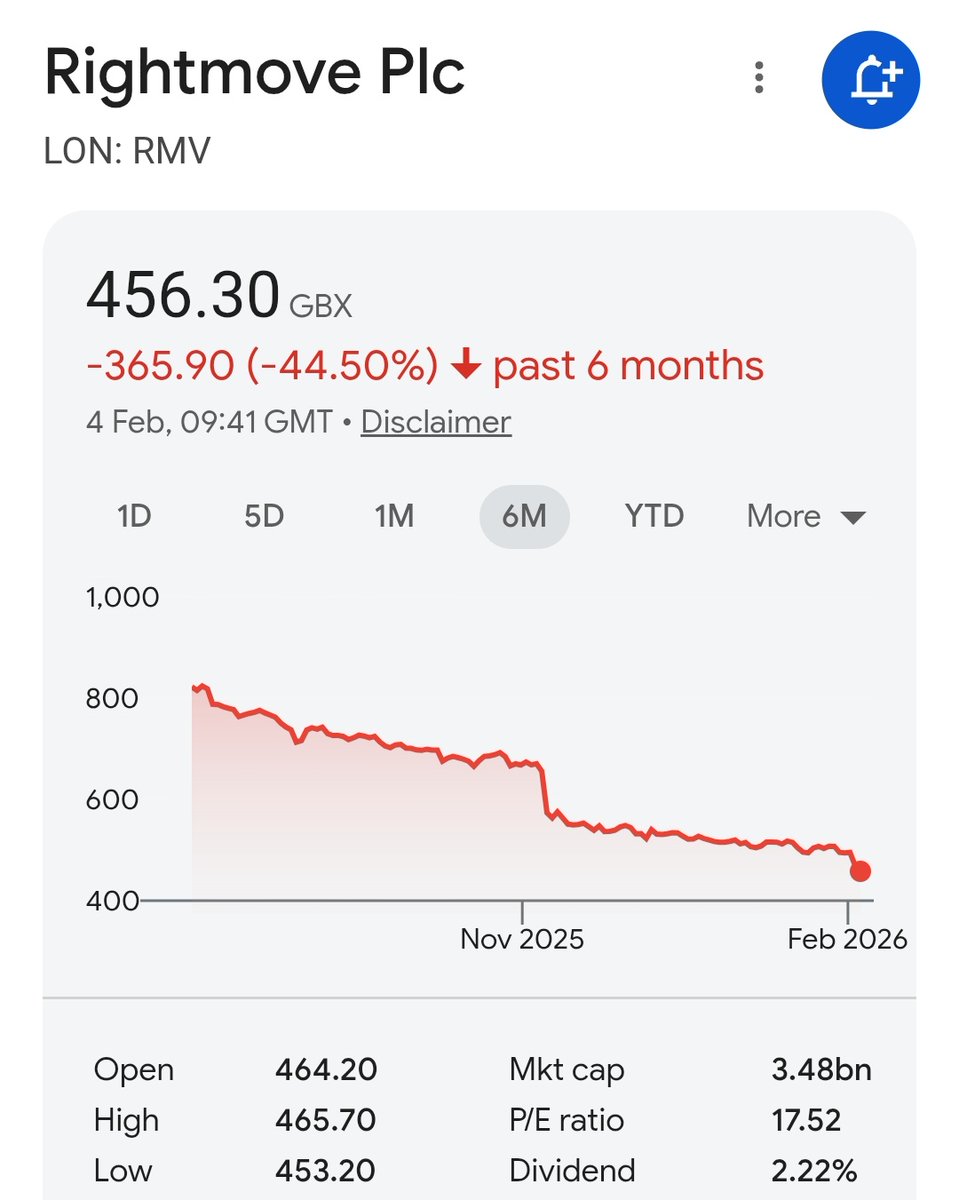

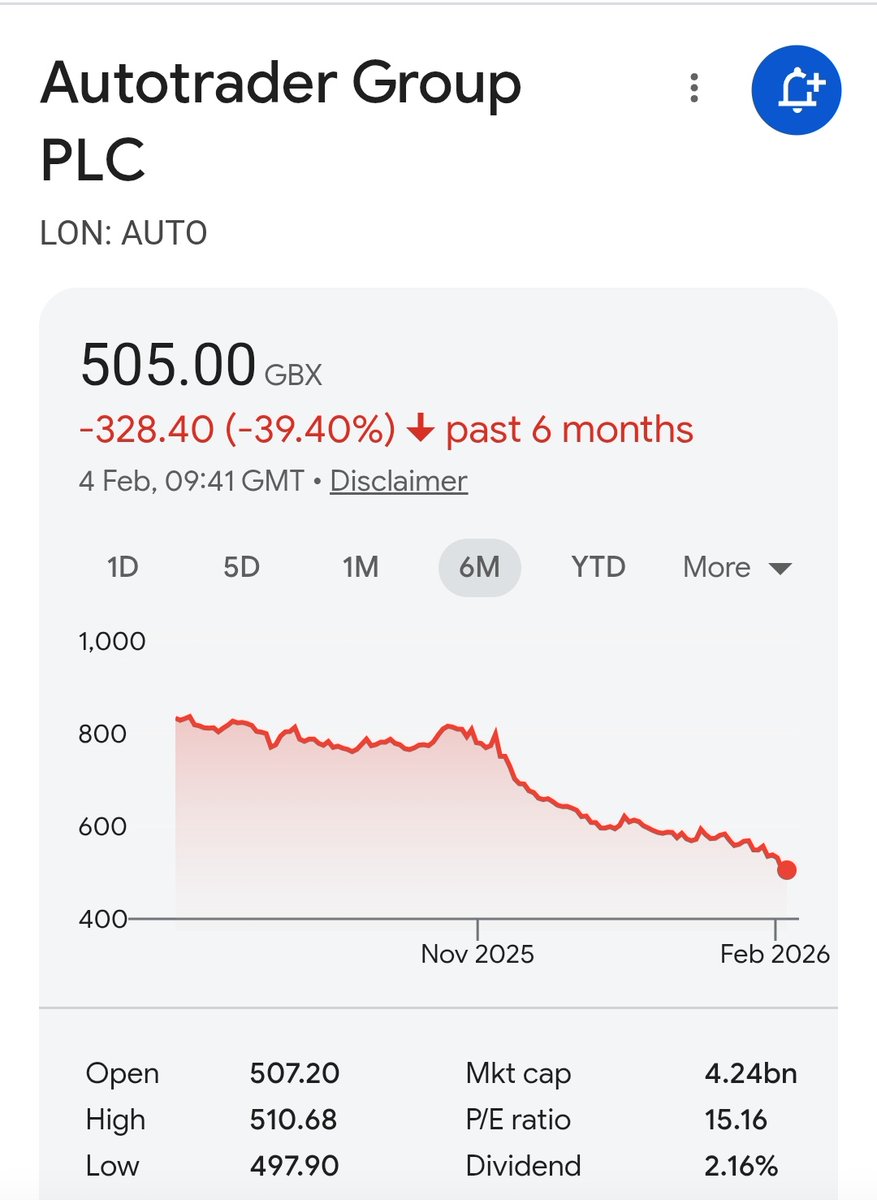

Rough six months for everyone's favourite property and car portals

Rightmove -45%

Autotrader -40%

Is AI really going to displace them?

English

@Uzocapital They’re both buys with any lt horizon, $rmv.l has a big chance of $rea coming back for it too

English

Rightmove $RMV.L & Autotrader $AUTO.L trading on 13x GAAP PE 2027….growing UK monopolies with pricing power, 50% free cashflow margins. Struggle to see why a dominant 2 sided network + destination website gets disrupted by ai vs layering ai tools themselves? What am i missng?

English

@TomSmith839 Fast casual vs qsr different skillset lets see how the roll out goes and if toast is successful.

English

@TomSmith839 Managing an enterprise scale rollout eg BK is very very different to catering for a local coffee shop. $toast has shown zero ability to have pmf at the enterprise level

English

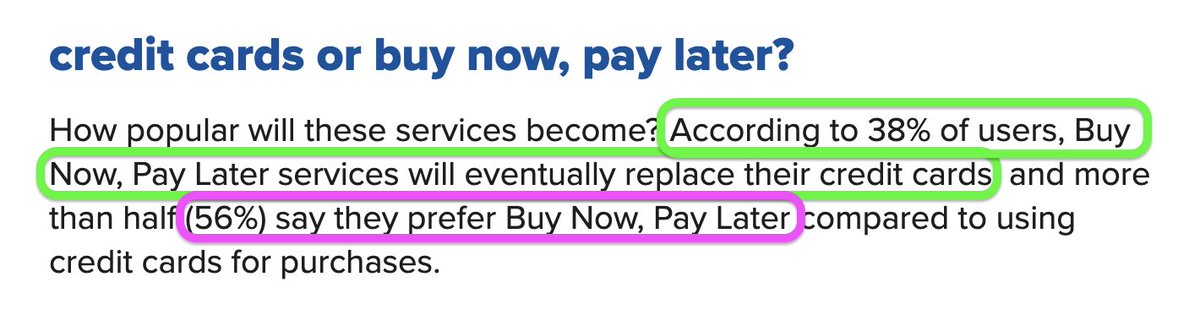

@bobspaysubstack Makes sense re $afrm I guess something like $zip.ax may be more protected as it’s a pure bnpl model, no traditional instalment products in the US, similar to $xyz with Afterpay.

English

You could look at it that way, and they would definitely get a boost, but if there’s increased scrutiny on APRs on credit products then that could eventually be trained on $AFRM and other BNPL providers. >70% of $AFRM’s GMV in the most recent quarter was interest bearing, with some APRs quite high.

English

Regulatory firestorm for the credit card industry $V and $MA

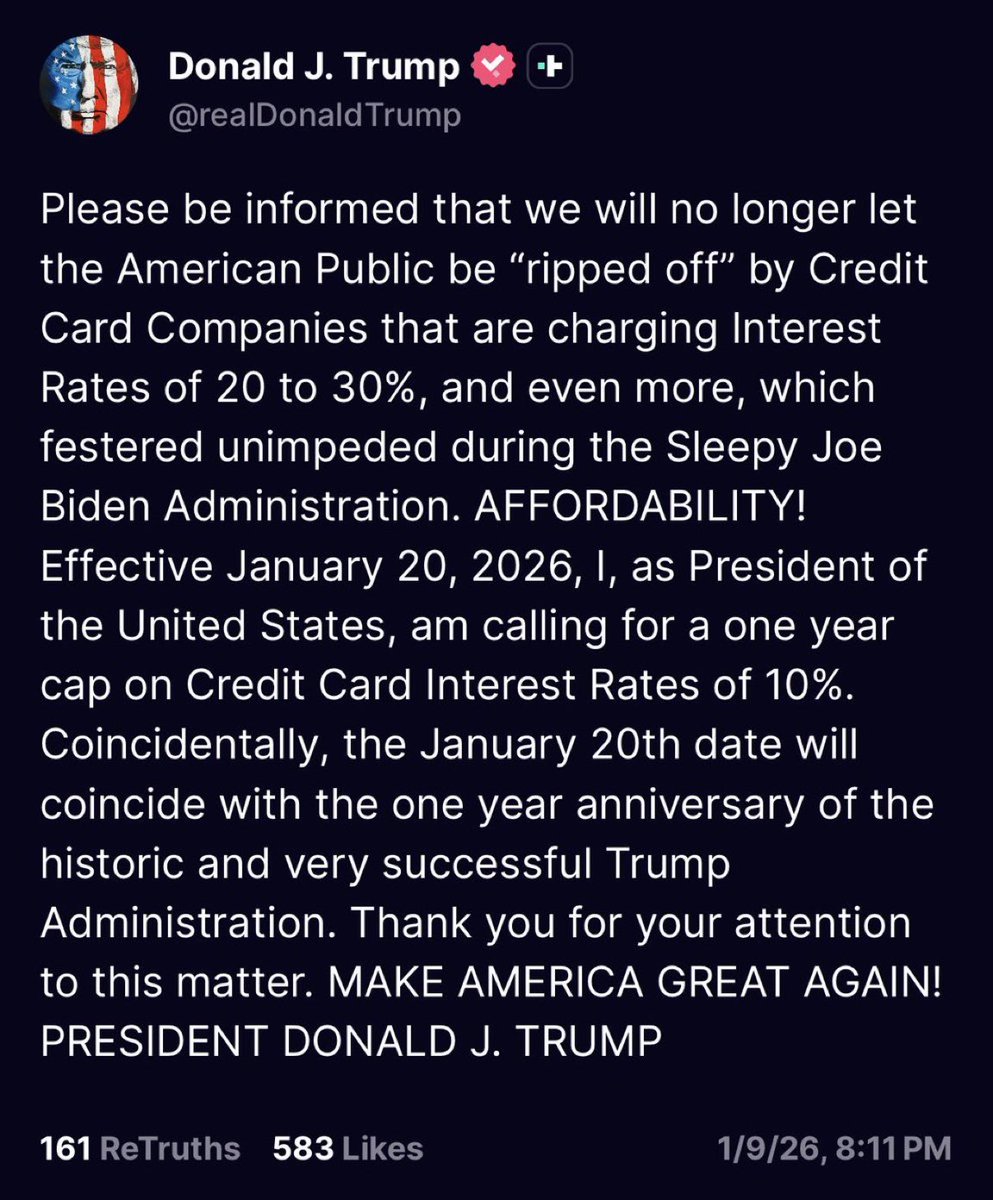

Okay, so my posts have been a bit meandering today, but here’s a recap:

President Trump has thrown his full weight behind the credit card competition act, which also had the support of his vice president in the past. I have no way of handicapping whether this will pass or not, but the odds are certainly higher after today and a vote almost certainly will happen in the Senate. The purpose of the bill is to drive down the cost of credit interchange by allowing merchants the option of processing a credit transaction over two unaffiliated networks. The technical implementation of such a thing would likely be complex and lengthy.

Lower credit interchange would have far reaching consequences. Significantly pared back or eliminated rewards programs is the most obvious. On the other hand, it would be a big boost for PSPs $PYPL $XYZ $TOST $SHOP that charge a gross fee to the merchant and interchange is a cost of goods sold, driving up the transaction margin.

Also sitting out there is the threatened 10% cap on credit card interest rates. Still think that is unlikely to go anywhere but $JPM certainly painted a dire picture of what the industry would look like if it happened (hint, a significant reduction in access to credit for a large portion of the population).

Right now, it looks like the ire of the Trump administration is squarely focused on the credit card industry. If you’re a bull you’re relying on President Trump’s preferred style of negotiation which is to make big threats to extract some (small) movement and claim victory. I still think that’s the more likely outcome.

Needless to say, if both of these measures passed or were implemented the industry would cease to exist anywhere near its current form.

English

Good luck getting a credit card approved if your FICO is 750 or below.

Perhaps 780 or below.

In housing, we create demand where there isn’t enough supply.

Here, we are going to cut supply where there is tons of demand for low income credit.

English

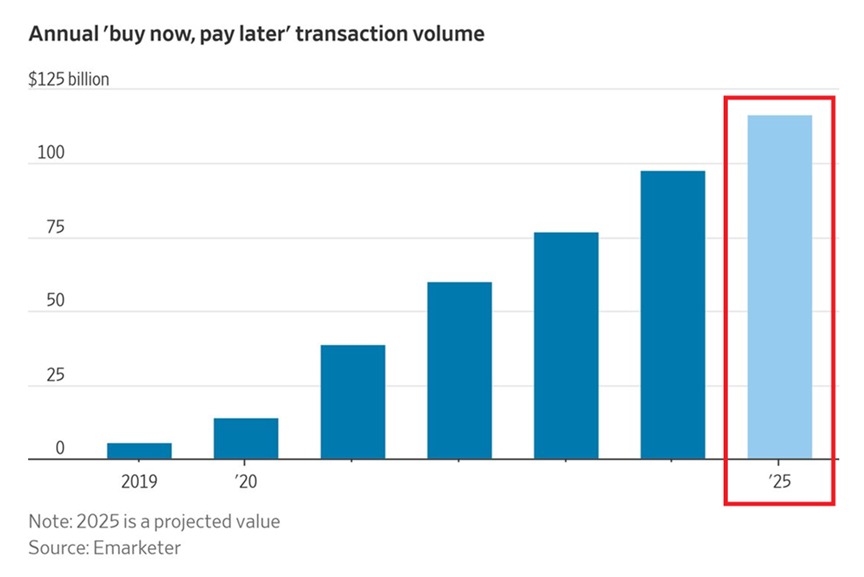

I was laying in bed last night thinking about the news regarding a 10% cap on credit card interest rates.

And there's a huge winner.

(but it’s not shorting $V or $MA like everyone’s screaming about)

It's the BNPL trade.

Why? If credit card issuers get forced into a 10% cap, they’re going to pull back on risky borrowers...really fast, which instantly removes access to credit for millions of people.

But (obviously) those consumers can't just stop spending, so they just migrate to using something else.

...and the only place for them to migrate is *buy now, pay later*.

Trump's announcement becomes a *structural* tailwind for BNPL adoption.

Without access to credit, people get pushed to alternative "credit" rails.

We literally just saw record numbers of BNPL activity over the holiday season. Demand is there.

So you have tightening credit, record demand, and a political catalyst that steers millions of consumers into BNPL by default?

aka an entire sector is on the verge of re-pricing...

I'm watching a few BNPL names:

One. $AFRM...cleanest pure BNPL exposure in the usa with a huge merchant network, and a direct volume lift coming

Two. $KLAR...largest BNPL platform in the world, recent IPO, eating market share in the US quickly

Three. $PYPL...massive distribution, "PayPal Pay Later" is already everywhere at checkout

Four. $SQ (owns cashapp + afterpay)...exposure to BNPL + consumer lending rails...secondary winner

But my top focus is $AFRM.

> more direct exposure & sensitivity to the U.S. credit tightening catalyst

> affirm is overwhelmingly us-centric

> stronger U.S. merchant penetration

> direct $amzn integration

> exclusive partnership with $shop

I like $KLAR too, but if this 10% cap only applies to the USA, then $AFRM is the most direct, immediate beneficiary.

This theme is about to really heat up.

$AFRM is currently $81.80.

The Kobeissi Letter@KobeissiLetter

BREAKING: President Trump calls for a 10% cap on credit card interest rates for one year, effective January 20th.

English

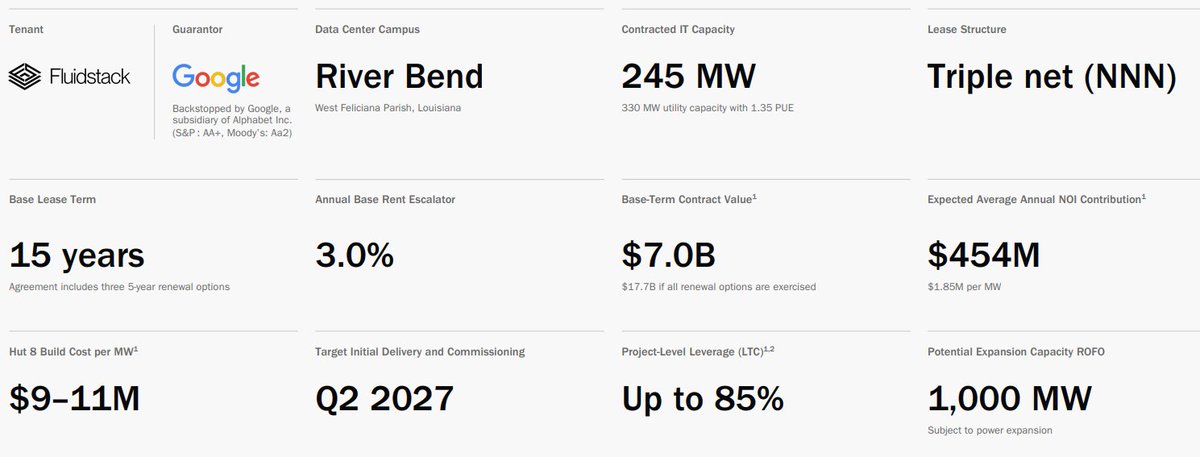

@656hjhfgvt The biggest risk to all of these miner to hpc plays is execution, $hut hasn’t done this before. But outside of $corz (due to capex being funded) this deal is the best in the space by a mile. We’re also long

English

9/9 $HUT

HUT 8 climbs to a top 10 holding in my portfolio. I’m planning adds to push it higher.

Am I missing anything? Dissenting voices are encouraged to add their take…

English

1/9 $HUT

Overlooked, some investors are still looking at the wrong metrics, treating the stock like a BTC miner. It’s not. $HUT isn’t just pivoting to AI, it is turning into an AI infrastructure operator with long term revenue tied to big tech. Breaking $60 today, feels legit 🚀

English

The btc miner to HPC transition sees a lot of grift and promotion. Some good deals in the space, $wulf with fluidstack, $cifr with AWS+ FS, and some less good deals, $iren with $msft, $corz delivery issues with $crwv. The recent $hut deal stands out at River Bend, Louisiana

English