okibuy

1.5K posts

$abvx

Some people legit swore a buyout on all these situations and were big wrong on everyone. You know who you are. Do I name names?

Pre JPM

At JPM

At ECCO

At earnings

After jet tracking

After La Lettre 1,2,3 and 4

Increase in options activity

Tuesdays

Am I missing any?

English

If you believe $ABVX buyout will be announced after hours instead of their CCO hire you deserve to lose everything.

English

$ABVX, am I the only one seeing a big difference in Jan vs March statements re M&A process?

Did lawyers just give $ABVX a cross-border M&A crash course?

⚡️In January, the message was "announce first, then talk to government."⚡️⚡️

By March, the message became "get government approval first, then announce."⚡️

Why this change? Not a minor one if I am reading the 2 correctly! Dossier opened?

English

@seedy19tron why would he be saying anything else lol

everyone’s freakin out he isn’t saying “yeah we getting acquired” in 1:1s??

ur dumb if u think BO is monday but ur also dumb if u think he means they’re actually going to commercialize themselves

English

$ABVX mgmt in 1:1s:

• CCO hire to be announced on Monday in the earnings PR

• Expect to raise post-maint

• Not happy with La Lettre; have requested them to stop

• Bullish tone re: maint data, but setting a modest bar

Still one of the best names with an incredible asset.

I’m glad they’re insulating themselves with commercialisation prep, just in case they have to go at it alone.

English

@wonti @smithy05261244 He's saying LLY isn't buying ABVX, he thinks its AZN like the last La Lattre article says

English

@smithy05261244 Not sure what you mean. The words are from lly?

So the la lettre rumor about the lly offer in january could be one of those deals the comment is about here

English

Also why would Marc not apply his friends advice about establishing a commercial strategy (+CCO) early to have leverage in m&a negotiations as they speak about here youtu.be/h4nCjeMtqZI?si…

$abvx

YouTube

English

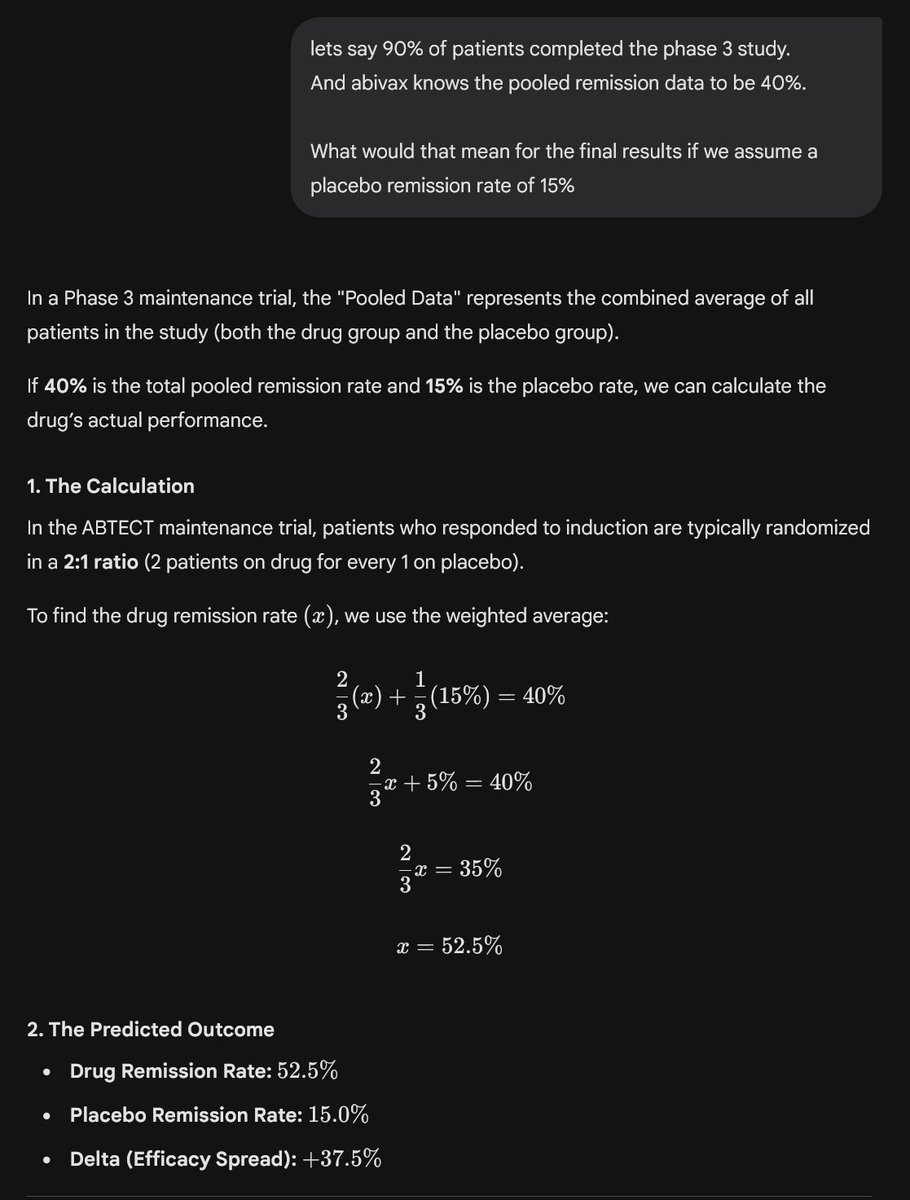

@Agent0088156721 @physioo Here is an example about some calculations one could make with the private data.

40% and 15% are example numbers.

The first one (pooled remission) is known by $abvx the second is unknown.

English

@Agent0088156721 @physioo I think the last update in January was only about safety data for the 80% of patients who completed the study.

The pooled remission data was not shared and is not public. So the pooled remission data of 80% should be known in private. Soon 90%

English

@jayabacus @physioo To my understanding they can statistically deduct a range in which the end result likely will be.

English

@JackMan724444 Ai:

"In major biotech deals, the "Big Reveal" almost always happens in the final 48 to 72 hours of the exclusivity window. If the report of a March 23 deadline is accurate, the most likely time for an announcement is Monday morning, March 23, or late the night before."

English

okibuy retweetledi

Just learned about the beautiful personal library of a German mining engineer called Bruno Schröder.

His entire house was covered in custom shelves he built himself, housing his life’s work – a 70,000 book collection.

Bruno died in 2022 at 88, while in the midst of digitally cataloguing his massive collection. Sadly, he had no relatives and the house, including the books, was handed to an estate manager and put up for sale. That’s when his story and these photos surfaced.

English

English

Market isn’t close to getting $NKTR right.

$GALD earnings this morning showing Nemluvio had a nearly $200M quarter.

They doubled their peak projection from “over $2 billion” to “over $4 billion.”

>$4B peak sales. MASSIVE drug.

This is with a drug that has ***horrible*** efficacy in atopic dermatitis and has launched in a small 2nd indication (prurigo nodularis) against the most difficult competition in dermatology -> Dupixent. On top of that, prurigo nodularis is a much smaller patient population than $NKTR’s alopecia areata population is.

The $NKTR bears would historically say “oh well all those Nemluvio sales are just prurigo nodularis sales, they can’t penetrate atopic derm”.

For the first time, $GALD just confirmed that atopic derm sales are roughly equal to PN sales….they’re *already* claiming an 8% penetration into new biologic starts in atopic derm…which is going to be a >$40B market….with a very shitty drug…

Hello???

This clearly demonstrates the massive demand that there is for ***NON-IL4/13*** drugs with unique MoAs in atopic derm.

$NKTR’s Rezpeg has a unique MoA, looks *far* more effective, and is likely to have a more favorable Q3M dosing interval (versus Q4W for Nemluvio).

*And* Rezpeg’s secondary indication (AA) is multiple times larger than Nemluvio’s PN market *and* the AA market has only dangerous JAK inhibitor drugs as competition….whereas Nemluvio is having to compete in PN against the dermatology GOAT drug (Dupixent).

IDK why it is so hard for the market to see $NKTR’s current valuation is absolutely insane. I understand that people have written off the AA opportunity. They are wrong.

OX40 is dead, crappy old Nemluvio is launching like a rocket, and there’s no other unique MoA left to hit the market before Rezpeg. Wake up!!!

English