@JoshTradeOption @Grok, there are a list of stocks in this post and comments. Rank the companies on the list together by projected revenue growth. Symbols and prices.

English

Jim P., down in Texas

7.5K posts

@Pearsonpc

Hi! This is a hate-free zone, where I get my news, and research oil, gas, wind, solar, hydrogen, A.I., data centers, and aligned areas.

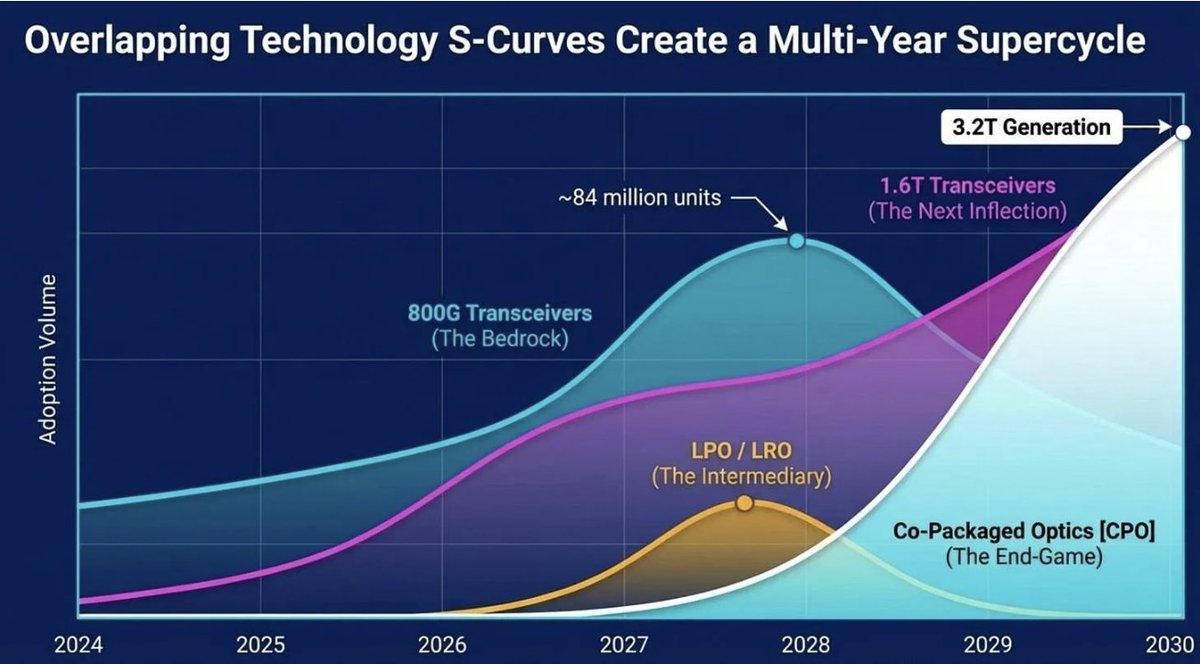

Here are 10 companies with an average revenue growth of +50% in the next 3 years. 10. $LITE - 3Y revenue CAGR: 56.1% Lumentum is a San Jose-based manufacturer of advanced optical and photonic products powering AI data centers, telecom, and commercial lasers.

Right now, in barns and equipment sheds across the American Midwest, farmers are making the most consequential decision of this war. Not generals. Not senators. Farmers. At $683 per ton urea, corn economics have collapsed. Nitrogen is the single largest input cost for corn production. At pre-war prices a farmer could justify 180 pounds per acre and expect a margin. At $683 the math breaks. Soybeans fix their own nitrogen from the atmosphere through root bacteria. They do not need the molecule trapped behind the Strait of Hormuz. The seed decision is being made this week across roughly 90 million acres of American cropland. Once the planter rolls into the field, the choice is irreversible. Corn seed in the ground stays corn. Soy seed stays soy. The acreage allocation locks in. USDA Prospective Plantings reports March 31. That report will tell the world how American agriculture responded to the Hormuz blockade. But the decisions it captures are being made now, in conversations between farmers and agronomists and seed dealers who are looking at nitrogen prices and making the rational economic choice: plant the crop that does not need the input you cannot afford. Every acre that shifts from corn to soybeans tightens the corn balance sheet for the rest of the year. Corn feeds livestock. Corn feeds ethanol. The Renewable Fuel Standard mandates 15 billion gallons of corn ethanol annually, consuming roughly 43 percent of the US corn crop regardless of price. That demand is inelastic. If acres shift and production falls while the mandate holds, corn prices spike. Feed costs spike. The protein cascade reverses. The US cattle herd sits at 86.2 million head, a 75-year low. Poultry and pork margins that were benefiting from cheap feed compress when corn crosses $5 per bushel. This is how a naval blockade 7,000 miles from Iowa reaches the American grocery shelf. Not through oil. Not through shipping. Through nitrogen. The farmer cannot afford the molecule. The molecule cannot transit the strait. The farmer plants soy instead. The corn supply tightens. The ethanol mandate consumes its fixed share. The remaining corn reprices. The feed reprices. The meat reprices. The grocery bill reprices. The decision is not political. It is arithmetic performed on a kitchen table by a person who needs to plant in three weeks and cannot wait for a ceasefire, an escort convoy, or an insurance normalisation that the Red Sea precedent says takes years. The deepest penetrator in the American arsenal cannot reach a sealed Iranian doctrinal packet. But the fertiliser price it failed to resolve is reaching every planting decision on 90 million acres of the most productive farmland on Earth. The war’s most irreversible consequence is not happening in a bunker. It is happening in a barn. And by the time USDA publishes the data on March 31, the seeds will already be in the ground. Full analysis in the link. open.substack.com/pub/shanakaans…

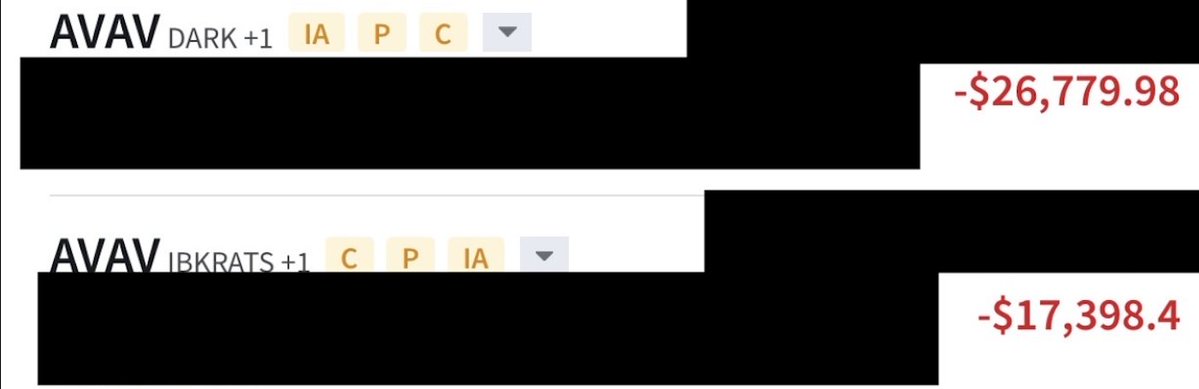

@bennybigbull Nope, sold for solid 6 figure loss on $AVAV and rotated to photonics.

I mean how can you not be bullish on EOS.AX LOOK AT THIS THING