AlphaQuantStrategist

608 posts

AlphaQuantStrategist

@QuantStrategist

Trust Data and Not Clowns | Think Critical | Searching for good Risk-Return-Profiles | No Investment Advice | Only Personal Views

Entrou em Mart 2023

847 Seguindo94 Seguidores

In the past year, I made two bad stock calls: $NOW and $CLBT. I’ve exited both.

Over the past week, I’ve reflected on what I can learn from these mistakes to improve my investment process. The main takeaway is that the pace and magnitude of change driven by Claude were far beyond my understanding.

Second, let price be your guide-I should have exited before.

And third, don’t bet on dinosaurs when humans are emerging.

Can these stocks rebound? Absolutely. But I chose to cut my losses this past week.

Z@ZeeContrarian1

$NOW - I’ve been listening to ServiceNow CEO Bill McDermott across multiple interviews and conferences lately, and one thing stands out: the guy is everywhere, and he’s speaking with a level of clarity and confidence that you don’t usually see unless a CEO truly believes in what’s coming. A logical, charismatic CEO understands something very simple: if you go across every media outlet talking about the future, talking about AI, talking about growth - and then the company misses the next earnings or guides down , you lose credibility instantly. The market remembers. Investors remember. So when someone with decades of experience is putting himself out there repeatedly with a consistent message, you have to assume he understands that risk. Credibility for a CEO is everything, and once it’s damaged it’s extremely hard to rebuild. Add to that the fact that Jensen Huang mentioned ServiceNow in the context of the AI ecosystem. Nvidia sits at the center of the AI infrastructure layer, so when the CEO highlights a company in that stack, it’s not random. Portfolio allocation: 10% via stock & options.

English

AlphaQuantStrategist retweetou

@micha_bloss @pebelsberger Wahrheit, dass die Technologie jahrelang doppelt bezuschusst wurde. Einspeisung und keine Netzentgelte auf Strom von PV-Anlage. Hör auf zu jammen und sei dankbar, dass du jahrelang subventioniert wurdest. Volkswirtschaftlich Blödsinn, da Kleinanlagen unwirtschaftlich sind.

Deutsch

@pebelsberger Ohne Einspeisevergütung, mit der Pflicht zur Direktvermarktung und niemand macht das, ist das ein faktisches Verhindern… So ist das leider.

Deutsch

#Breaking Katherina Reiche plant den kompletten Stopp für Solaranlagen auf Privathäusern.

100.000 Menschen arbeiten in der Branche, diese Jobs sind alle gefährdet.

Die Gaslobbyistin Reiche macht Politik gegen alle, die einfach nur eine Solaranlage auf dem Dach haben wollen.

Deutsch

@MinotaurStocks 1/3 of the market cap gone and I have no idea why.

English

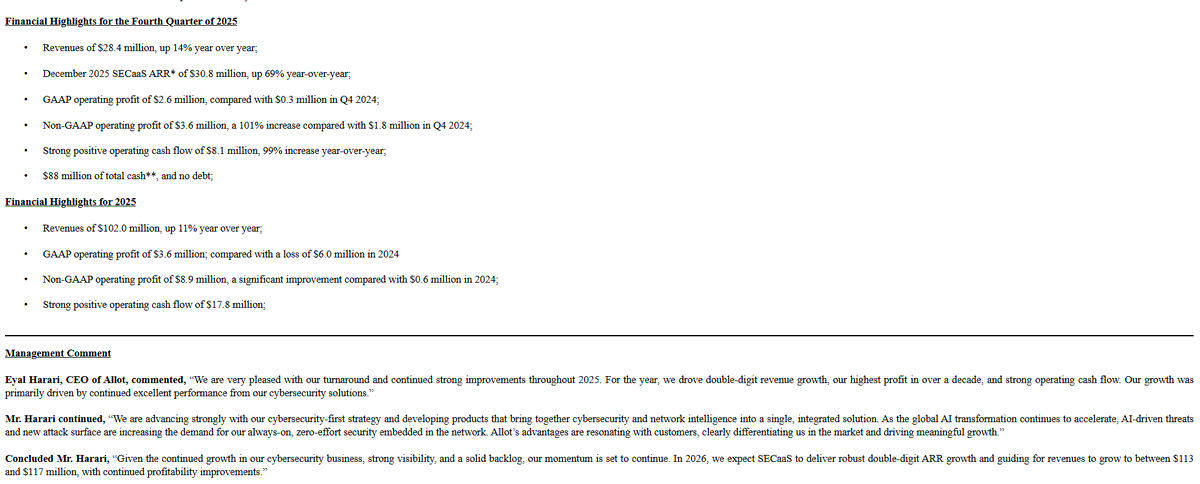

$ALLT today likely a victim of higher buyside expectations for the 2026 guide and the risk-off environment around cybersecurity and SaaS stocks in general. However, the conference call was unequivocally positive. Book to bill in Smart "way above one," and new high single digit millions win underscores the conservatism in '26 outlook. SECaaS incremental ARR is expected to stay constant with Q4 levels despite no major new customer launches (and it sounds like acceleration is possible), implying 43% SECaaS growth for '26 when run rating Q4's +$3.3m. Profitability will improve with no major degradation in GMs even despite DRAM cost pressures.

Most of all, however, we think $ALLT nailed the messaging around how and why its capabilities are purpose built for today's AI threat landscape. $ALLT excels in managing, optimizing and securing vast amounts of network traffic at scale, a core competency that has never been more needed than today. $ALLT has expanded its product array masterfully to offer OffNet, firewall, identity and DDOS capabilities alongside its core network security engine and is set to reap the benefits of a surge in SMB and consumer cyber threat awareness. Ironically, the market is pummeling a company likely to be one of the biggest beneficiaries of the AI trend in cybersecurity.

In fairness, we wish management had guided a little more aggressively for 2026 just to more appropriately signal the strength of the underlying business. Growing backlog by $50m+ but guiding to an implied 0 - $5m in SMART growth is a little ridic. Conversely, if $ALLT had an authorization in place with its $88m net cash balance sheet, then sandbag all you want and buy stock on the correction.

One thing is for sure: Based on today's numbers and earnings call, the $ALLT business and investment thesis has never been stronger. Over time, it will be reflected in the share price.

English

@MinotaurStocks Why ist the stock down 20 %? Numbers looks great. Did they say anything bad in the earnings call?

English

$ALLT just reported Q4: ARR growth of 69% came in well ahead of 60% guidance, with operating cash flow of $8.8m for Q4 alone. The combined operating leverage + growth story at $ALLT is a unique one in public markets. We believe AI will be a strong tailwind for $ALLT in 2026.

English

@QuantStrategist @CapexAndChill Lmao whatever narrative gives you comfort.

English

The market is actually on crack. $V $MA $AXP are supposed to benefit from digitalization 🤣

amit@amitisinvesting

didnt know we were vibe coding the global financial system now

English

@QuantStrategist Still nonsense to me corporate.visa.com/en/solutions/c…

English

@KairosPraxis @AndrewTakes This become fucking ridiculous ....

English

@AndrewTakes 1. Market treating CLBT like a saas name

2. DHS funding issues (DHS one of CLBT's main customers)

3. Big regulatory approval still pending, due this quarter (FEDRAMP)

English

@JohnHuber72 @ikaroscapital LOL, bc their ratings in 2008 were so right ....

English

True, but charging in excess of what something is worth is not usually sustainable. “Your margin is my opportunity” comes to mind. If AI can eventually replicate much of this for free or a fraction of the cost, I think there will be pricing pressure as new competitors create tools at a fraction of the cost. The funds will switch if the competitive product isn’t just cheaper, but also more advanced. And eventually, I think AI will be just as accurate. Of course, these companies are using AI as well to defend against this risk. We’ll see how it shakes out, but it’s a plausible risk imo.

English

The debate on whether the SPGI/MCO ratings regulatory moat is immune to AI should not the main concern here (imo). If only a minority of your revenue (20-30%) comes from a segment that can be easily replicated with AI, it could have a major impact on your business. The ratings moat can be fully intact, but maybe the $20k CapIQ product (which has massive margins) is way overpriced.

I’m not suggesting this is my view, but that is what I would be thinking about as a much greater likelihood than upsetting the ratings moat.

My hunch is these companies will adapt and remain good businesses long term, but I don’t think it’s an irrational market reaction to discount some chance of a piece of their business seeing pricing pressure, given what we know AI can do in this space. Because it happened all at once makes it feel irrational, and often times these moves are, but maybe these stocks were a bit overpriced before. I’m not sure either way, but I just think the debate on ratings moat might not be the right debate

Century Egg Credit@yummyCenturyEgg

Where do you think $MCO and $SPGI get their regulatory moat from? Is that Gospel? "everyone can do credit rating" is so true, but not everyone can do credit rating across all of credit on every single credit. AI will devalue analytical work. Once that's gone, it is very easy to see regulatory moat gone. The regulatory infrastructure doesn't even have to actually change before $MCO and $SPGI lose half of their value.

English

English

@RihardJarc For me is crazy that search grows 17 %. How can this be in a time where many people mainly use mainly chatbots?

English

I've been holding almost 30% cash for 10 months. Today, starting to deploy half of it

English

@na_option LOL, but TESLA is already priced as they were the only producer of autonomous EVs and robots. Stock is overpriced by at least 50 %. Furthermore Elon's political actions lead to catastrophic EV sales numbers in Europe ....

English

There’s always a negative way to spin a story, it defines your character.

If you had sold when Burry posted in Jan 2023, you would have missed out on 71% gain in $SPY

$TSLA will never be the only company to produce EVs, Autonomous EVs or robots but they will be a major player that takes most of the share.

When you think smart phone you imagine an iPhone. When you think EVs you imagine a Tesla.

Soon when you think autonomy you will imagine a Cybercab. When you think humanoid robot you will imagine @Tesla_Optimus.

Competition will be crumbs.

Cassandra Unchained@michaeljburry

Say what you want, but I'm right. CNN: Tesla scraps Model S and Model X to build robots "Tesla (TSLA) CEO Elon Musk, who turned an upstart electric vehicle maker into an industry-changing powerhouse, is pulling the plug on the two models that helped get him there, as he struggles with another quarter of declining profits and car sales. He announced the end of production of two models – the Model S and Model X, among the company’s most expensive models, on a Wednesday earnings call. Instead, the company will use that factory space to build humanoid robots instead." Foundations: The Tragic Algebra of Stock-Based Compensation open.substack.com/pub/michaeljbu…

English

@fintegrate Good quarter, but sky high valuation ....

English

@RihardJarc The problem is that Meta and others are interested in promoting the benefits of AI. Independent research often says the opposite, that AI has so far led to hardly any productivity gains.

English

People still don't truly comprehend the ramifications of this. $META CFO:

»Since the beginning of 2025, we've seen a 30% increase in output per engineer with the majority of that growth coming from the adoption of agenetic coding, which saw a big jump in Q4. We're seeing even stronger gains with power users of AI coding tools, whose output has increased 80% year-over-year. We expect this growth to accelerate through the next half.«

English

@ThomasVierhaus @Lars_Feld @EuckenInstitut Ich wäre duraus für einen Kompromiss bereit, aber Abfindungen lehne ich definitiv ab. Du hast auch Recht, dass Kündigungsschutz eine Regel zur Begrenzung von Machtasymmetrien ist, die allerdings aus meiner Sicht heute im. Vgl. zu damals nicht mehr gegeben sind.

Deutsch

Wir haben unterschiedliche ordnungspolitische Grundannahmen, das ist erkennbar. Für mich ist Kündigungsschutz keine Frage der aktuellen Arbeitsmarktlage oder individueller Arbeitgeberkosten, sondern eine institutionelle Regel zur Begrenzung von Machtasymmetrien und zur Stabilisierung von Erwartungen. Die Kritik an starren Verfahren teile ich – die Forderung nach Abschaffung nicht. Dabei belasse ich es – als Arbeitgeber.

Deutsch

@Lars_Feld, Professor für Wirtschaftspolitik an der Universität Freiburg und Direktor des dort ansässigen @EuckenInstitut, berührt mit seiner aktuellen Kritik am #Kündigungsschutz einen klassischen ordnungspolitischen Zielkonflikt – und genau dort liegt auch die Quintessenz.

Aus ordnungspolitischer Sicht ist der Kündigungsschutz weder per se innovationsfeindlich noch automatisch innovationsfördernd. Er erfüllt eine legitime Schutzfunktion in der Arbeitsmarktordnung: Er begrenzt Machtasymmetrien, schützt vor Willkür und stabilisiert Erwartungen. Diese Funktionen sind kein sozialpolitisches Beiwerk, sondern konstitutiv für eine marktwirtschaftliche Ordnung, die auf Vertrauen, Investitionen in Humankapital und langfristige Kooperationsbeziehungen angewiesen ist. In diesem Sinne kann Beschäftigungssicherheit durchaus innovationsfördernd wirken – nicht durch Zwang, sondern durch Erwartungssicherheit.

Problematisch wird der Kündigungsschutz jedoch dort, wo er faktisch zu einer Versteinerung betrieblicher Strukturen führt. Ordnungspolitisch kritisch ist nicht der Schutz vor Entlassung an sich, sondern die Kombination aus hohen rechtlichen Hürden, langen Verfahren und schwer kalkulierbaren Kosten. Sie verzerrt unternehmerische Entscheidungen ex ante: Unternehmen vermeiden Neueinstellungen, scheuen radikale Strategiewechsel und internalisieren Risiken, die eigentlich über Märkte verteilt werden sollten. Innovation wird dann nicht verhindert, aber systematisch entmutigt – insbesondere dort, wo technologische Brüche schnelle Anpassungen erfordern.

Der Kernkonflikt liegt damit nicht zwischen „Sicherheit“ und „Innovation“, sondern zwischen Bestandsschutz und Anpassungsfähigkeit. Eine ordnungspolitisch saubere Lösung kann daher nicht in einem simplen Abbau des Kündigungsschutzes bestehen, sondern in seiner funktionalen Entzerrung: klare, vorhersehbare Regeln statt prozessualer Ungewissheit; schneller Strukturwandel mit sozial abgefederten Übergängen statt juristisch blockierter Anpassung. Kurz: Schutz der Person, nicht Konservierung des Arbeitsplatzes.

Die ordnungspolitische Quintessenz lautet daher: Eine innovationsfähige Arbeitsmarktordnung braucht Sicherheit in den Regeln, nicht Starrheit in den Strukturen. Kündigungsschutz darf kein Investitionshemmnis werden – er muss Erwartungssicherheit schaffen, ohne ökonomische Erneuerung zu blockieren.

handelsblatt.com/meinung/oekono…

Deutsch

@ThomasVierhaus @Lars_Feld @EuckenInstitut Absicherung ist zudem durch Arbeitslosengeld und anschließend Bürgergeld in D mehr als gegeben.

Deutsch

@ThomasVierhaus @Lars_Feld @EuckenInstitut Ich bleibe bei der Meinung, dass der Kündigungsschutz in einem Land mit nahezu Vollbeschäftigung nicht notwendig ist. Du argumentierst nur aus AN-Sicht, die Nachteile trägt alle der AG. Wenn ich wg. KI z. B. eine Vielzahl von MA entlassen will, ist das in D ein Rießenaufwand.

Deutsch