Concerned_American

10.5K posts

Concerned_American retweetou

$CLOV

The Trillion Dollar Question

People always ask me what comes next. I told you the story of Andrew Toy. I told you about BlackBerry. I told you about how the people kill the incumbent, not the competitor. Today I'm going to show you the math. And when you see it, you're going to understand why this is not a million dollar question, not a billion dollar question, but potentially a trillion dollar question.

Let me set the table.

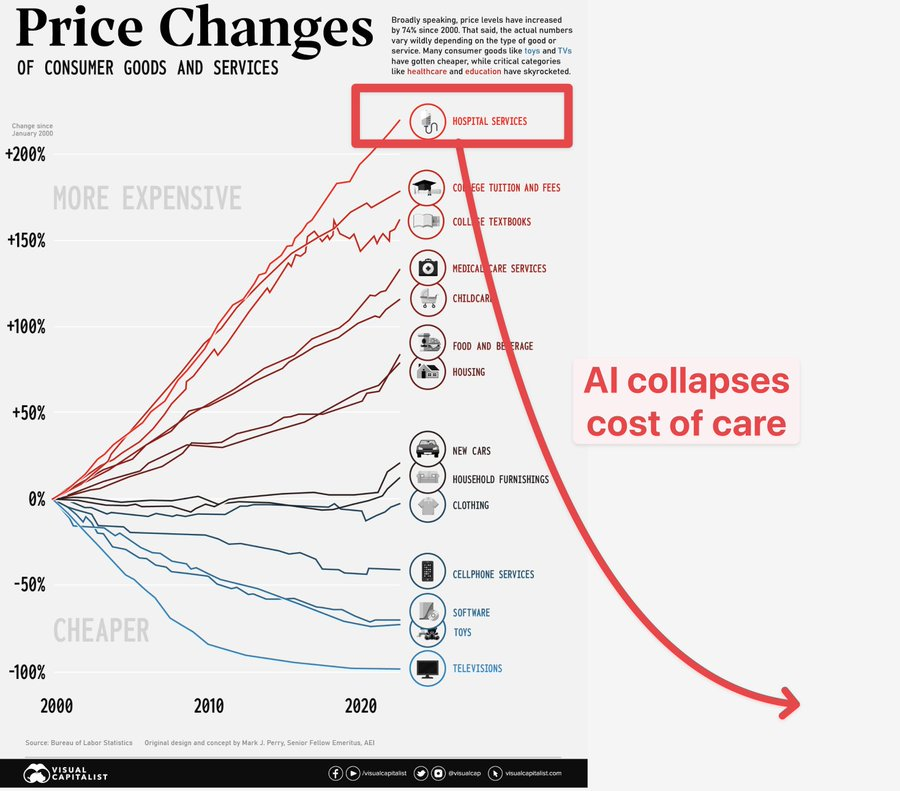

The Chart That Should Terrify Every American

There is a chart that has been circulating for years showing the price changes of consumer goods and services since the year 2000. On the bottom of that chart, you see the things that technology touched. Televisions dropped over 100%. Software collapsed in price. Cell phone services fell by more than 50%. These are the industries where innovation was allowed to do its job, where competition drove prices down and quality up. The consumer won.

Now look at the top of the chart. Hospital services have increased by over 200% since the year 2000. Medical care services are up over 100%. These are the industries where the system was designed not to get better but to get more expensive. The question every American should be asking is simple. Why did technology make everything else in my life cheaper except the one thing that can bankrupt me?

The Numbers Are Staggering

The United States spent $5.3 trillion on healthcare in 2024. That is not a typo. $5.3 trillion. That works out to roughly $15,474 per person in America, and it now accounts for 18% of the entire gross domestic product of the country. To put that in perspective, the United States spends more on healthcare than the entire GDP of every country on the planet except China. CMS projects that healthcare spending will reach $5.6 trillion in 2025 and is on pace to hit $8.6 trillion by 2033. The health share of the economy is expected to climb to over 20% of GDP within the next decade.

Federal spending on healthcare programs alone hit $1.8 trillion in 2025. Medicare cost the federal government $988 billion. Medicaid and CHIP cost another $691 billion. And CBO projects that Medicare spending will nearly double to $2 trillion by 2036. These are numbers so large that they almost lose their meaning, so let me bring it down to earth.

The gross national debt broke through $39 trillion in March of 2026. The federal government is currently running a projected deficit of $1.9 trillion for fiscal year 2026 alone. Interest payments on the national debt reached $270.3 billion in just the first three months of fiscal year 2026, which now exceeds what we spend on national defense. The Bipartisan Policy Center and the Congressional Budget Office have both stated plainly that under current law, the debt trajectory will rise from 100% of GDP today to 156% of GDP by 2055. And the largest driver of that trajectory is healthcare spending.

This is the debt spiral. And healthcare is the engine powering it.

## The M2 Money Supply and Why Costs Will Not Fix Themselves

Here is where the economic conversation needs to happen because most people do not connect these dots. The M2 money supply, which includes cash, checking deposits, savings accounts, and other liquid assets, hit a record $22.4 trillion as of January 2026. That represents a 4.5 to 4.8% year over year increase, and it is climbing after a brief period of contraction following the pandemic era explosion. Between 2020 and 2022, the Federal Reserve injected an unprecedented amount of liquidity into the economy. M2 went from roughly $15 trillion to over $21 trillion in less than two years.

Here is what this means for healthcare. When you expand the money supply, you do not magically create more doctors, more hospital beds, or more MRI machines. You create more dollars chasing the same constrained supply of medical resources. This is textbook monetary inflation applied to a sector that already has structural pricing problems. Healthcare costs were rising before the money printing. The liquidity injection poured gasoline on a fire that was already burning. And the government is addicted to this cycle. Spend more, print more, borrow more, repeat. They cannot stop because the political incentives are designed to keep the spending going. The M2 money supply tells you that the era of easy money is not over. It paused. Now it is expanding again. And every dollar that gets created dilutes the purchasing power of the dollars you already have, which means the $5.3 trillion we spent on healthcare last year will be $5.6 trillion this year, and $6 trillion the year after that, and $8.6 trillion by 2033. The trajectory does not bend on its own. It requires something external to break the cycle.

The Insurance Model Is Broken and the People Know It

Let me ask you something. If you are paying $560 to $610 a month in premiums for an individual ACA plan before subsidies, and your deductible is $7,476 on a Bronze plan or $5,304 on a Silver plan, at what point are you actually insured? You are paying nearly $7,000 a year in premiums and then you are told that you need to spend another $5,000 to $7,500 out of pocket before your insurance even starts helping you. That means for a healthy individual, you could be spending $12,000 to $14,000 a year before your insurance company pays a single dollar toward your actual medical care.

For employer sponsored plans, the average deductible in 2025 was $1,886 for a single employee, with small companies averaging $2,631. And if you are on a high deductible health plan, the average annual premiums are $8,620 for single coverage and $25,379 for a family. The maximum out of pocket for 2026 is $10,600 for an individual and $21,200 for a family. For 2027, those numbers jump to $12,000 and $24,000. CMS has even proposed allowing catastrophic plans to go as high as $15,600 for an individual and $31,200 for a family.

At some point, a reasonable person has to ask: what am I paying for? Many Americans are now doing the math and realizing that for routine care, preventive visits, and even some procedures, it can be cheaper to pay out of pocket than to use their insurance. You are paying for the privilege of having a card in your wallet that does not start working until you have already spent thousands of dollars. Medical debt has become one of the leading causes of bankruptcy in the United States. People with insurance are going bankrupt from medical bills. That is not a functioning system. That is a system designed to extract money from consumers at every possible point of contact.

And here is the part that should make your blood boil. Traditional insurance companies have zero structural incentive to lower costs. They operate on what is essentially a percentage of total medical spending. When costs go up, they raise premiums. Their revenue goes up. Their administrative cut gets bigger. They profit directly from the inflation of the very system they claim to manage. Why would they ever want costs to come down? The answer is they would not. And they have not. For decades.

CMS Is Cracking Down and the Incumbents Are Bleeding

But something has changed. The Centers for Medicare and Medicaid Services has started applying serious pressure. And the results are showing up in the stock prices of the largest health insurers in America.

UnitedHealth Group, which for over a decade was considered one of the most reliable growth stocks on Wall Street, has lost roughly 54% of its value from its 52 week high of $606 to around $277 as of recent trading. The company's medical care ratio exploded from a stable 82% where it had sat for years to 88.9% in 2025, with some quarters hitting 89.9%. That is a 600 basis point increase eating directly into profits. Their adjusted EPS collapsed 40.9% year over year. Their operating margin fell from 5.2% in 2024 to 2.7% in 2025. Optum Health, their services arm, swung from $7.77 billion in operating income to a $278 million operating loss. The company is now projecting its first annual revenue decline in more than three decades, guiding to just over $439 billion for 2026, a 2% drop from last year and well below analyst expectations.

The structural headwinds are real. CMS is eliminating diagnosis based reimbursement upcoding starting in 2027. The V28 coding transition represents a $6 billion headwind in 2026 alone. The proposed 2027 Medicare Advantage rate increase is essentially flat. UnitedHealth has the highest MA exposure in the industry at 30% of national enrollment, and they are planning to shed roughly 1 million members in 2026 to right size their book of business. They are getting smaller to try to survive.

Humana is in even more trouble. Their star ratings on their largest contract dropped from 4.5 stars to 3.5 stars, and the percentage of members enrolled in plans with four or more stars plummeted from 94% to just 25%. That translates to a $3.5 billion net revenue headwind. Their 2026 earnings guidance came in at "at least $9.00" per share, which is a 47% decline from 2025 and well below analyst expectations of $12.00. For 2026, Humana has stated that individual Medicare Advantage margins are expected to be slightly below breakeven. The second largest MA insurer in the country is telling you they expect to make essentially nothing on their core product.

This is not a temporary blip. This is a structural reset of the entire Medicare Advantage business model. The government is deliberately squeezing margins. CMS is demanding higher quality, better outcomes, and lower costs. They are removing the coding tricks that allowed insurers to inflate their reimbursements. They are raising the bar on star ratings. And the incumbents cannot handle it because their entire model was built on the assumption that costs would keep going up and they would keep getting paid more.

AI Collapses the Cost of Care

Now go back to that chart. Look at the bottom half. What do all of those industries that got cheaper have in common? Technology entered the equation and fundamentally changed the cost structure. Software made cell phone services cheaper. Automation made electronics cheaper. The internet made information free.

Healthcare has been waiting for its technology moment. And the hypothesis on that chart is exactly right. AI collapses the cost of care.

But let me be specific about how, because this is where most people get lost. The way AI collapses healthcare costs is not by replacing doctors. It is not some science fiction robot performing surgery. It is by giving doctors better information at the exact moment they are making clinical decisions. It is about catching a chronic condition in year one instead of year five. It is about diagnosing COPD when it is manageable with a $50 monthly prescription instead of when it requires a $200,000 hospitalization. It is about making thousands of better clinical decisions every day, at the point of care, across millions of patients.

This is the difference between reactive medicine and proactive medicine. The current system waits until you are sick, then spends enormous amounts of money trying to make you less sick. A proactive system identifies the trajectory of your health early and intervenes when it is cheap, effective, and humane.

Who Captures the Alpha

So here is the trillion dollar question. If healthcare AI can decrease the cost of care, who collects the alpha? Who wins?

Ultimately, the American taxpayer wins. If you can bend the cost curve on a $5.3 trillion annual expenditure, even by a few percentage points, you are talking about hundreds of billions of dollars in savings. For a country in a debt spiral where healthcare spending is the single largest driver of federal deficits, the ability to reduce costs is not just valuable, it is existential. The government literally cannot afford the current trajectory. The numbers do not work. Something has to give.

But here is the critical insight. These costs are not going to decrease by magic. The government cannot simply legislate costs lower without destroying access to care. You cannot tell hospitals to charge less without hospitals closing. You cannot tell doctors to accept less without doctors leaving the profession. The money printing will continue. The M2 money supply will keep expanding. The government will keep spending because it is structurally incapable of doing otherwise.

What has to happen is that a company needs to build the technology that makes it possible to deliver better care at lower cost. Not cheaper care. Better care that happens to cost less because it is proactive rather than reactive. The company that solves this problem does not just win a contract. That company becomes a critical piece of the national infrastructure. It becomes the technology layer that sits between the government, the providers, and the patients, and it earns a premium for every dollar of cost it removes from the system.

On a $5.3 trillion annual spend that is heading toward $8.6 trillion, even capturing a fraction of the value created by bending that curve is a massive, generational business opportunity.

Counterpart Health and the Case for Clover

Counterpart Health, a subsidiary of Clover Health, is building exactly this. And the data is not theoretical. It is real, published, and compounding.

In 2025, Counterpart Health released results showing that returning Clover Health members whose primary care physicians use Counterpart Assistant demonstrated an approximate 1,500 basis point MCR differential compared to those whose doctors do not use the platform. Let me say that again. 1,500 basis points. In an industry where UnitedHealth is in crisis because their MCR moved 600 basis points in the wrong direction, Clover's technology is demonstrating a 1,500 basis point advantage.

Counterpart Assistant is not a back office analytics tool. It operates inside the clinical encounter, at the moment the doctor is making decisions with the patient. It provides real time, clinically intuitive insights about the patient's full medical history, chronic conditions, gaps in care, and recommended interventions. In 2025, new capabilities were added including integrated ambient scribing, natural language chat within a PHI safe environment, and proactive visit summaries. This is not a static product. It is evolving into a full clinical operating system for value based care.

The outcomes speak for themselves. New members were 75% more likely to be diagnosed with COPD in their first year under a Counterpart Assistant physician. Outpatient pulmonology utilization increased 18%, meaning patients were being treated in lower cost settings instead of emergency rooms. All cause hospitalizations dropped 18% for congestive heart failure and 15% for COPD. Thirty day readmissions fell 25% for CHF and 18% for COPD. In high need, underserved neighborhoods measured by Area Deprivation Index, diagnosis rates were 70 to 89% higher across four major chronic diseases when Counterpart Assistant was in use.

Clover Health's PPO Medicare Advantage plan achieved the number one HEDIS score nationwide for the second consecutive year. Not among small plans. Not among technology companies. Nationwide, across every PPO MA plan in the country. And they did this with a wide network of non employed physicians, without capitation, meaning the technology itself is driving the quality, not a closed system of owned doctor groups.

From a financial perspective, Clover Health reported $1.924 billion in total revenues for 2025, a 40% increase year over year. Medicare Advantage membership grew 38% to 113,803. The company achieved adjusted EBITDA profitability of $21.7 million. For 2026, Clover is guiding to 154,000 to 158,000 average MA members, total revenues of $2.81 to $2.92 billion, consolidated gross profit of $470 to $510 million, adjusted EBITDA of $50 to $70 million, and is targeting its first ever full year GAAP net income profitability in a range of $0 to $20 million. Membership grew 53% for the 2026 plan year, with over 95% retention during the annual enrollment period and over 97% of members in their flagship PPO product.

Counterpart Health is also scaling its third party business. Live third party customer clinicians grew over 450% year over year. The company has stated that it believes Counterpart can help external providers and payers improve their MCR by over 1,000 basis points, with a 700 basis point reduction by the second year and an additional 800 basis points by the third year. For context, if Humana, which has roughly 7 million Medicare Advantage members, could achieve even a fraction of this improvement, it would translate into billions of dollars in annual savings.

The Defense of This Argument

Let me address the counterarguments directly because I said I would build this case with no holes.

"Clover's MCR data is self reported." The HEDIS score is not. HEDIS is an industry standard quality measurement maintained by the National Committee for Quality Assurance. Clover's PPO plan being ranked number one nationally is independently verified. The hospitalization reductions and readmission data are drawn from retrospective analyses of real patient encounters. And the company's overall financial MCR, while different from the differential metric, is reflected in their actual insurance results and CMS filings.

"The incumbents could build this technology themselves." UnitedHealth has spent billions on Optum. Optum Health just swung to a $278 million operating loss. Humana's cost management strategy has resulted in a star rating collapse and near breakeven margins on their core product. The incumbents have had decades and tens of billions of dollars to solve this problem. They have not. Because their business model was never designed to lower costs. It was designed to process claims.

"Clover is still a small company." Correct. With $1.9 billion in revenue growing at 40% year over year, approaching first time GAAP profitability, and a technology platform that is demonstrating clinical and financial results that the largest companies in the industry cannot match. Every company that eventually became a dominant platform was small once. The question is whether the technology works. The data says it does.

"Medicare Advantage is under regulatory pressure." It is. And that pressure is exactly why this technology matters. CMS is demanding lower costs and better outcomes. The companies that cannot deliver are being crushed. The company that can deliver those outcomes through technology is not threatened by this pressure. It is the solution to it. When the government says it wants lower MCRs, better star ratings, and proactive care, they are describing what Counterpart Assistant already does.

The Conclusion

The United States spends $5.3 trillion a year on healthcare. That number is heading toward $8.6 trillion. The national debt is at $39 trillion. Interest payments alone now exceed defense spending. The M2 money supply is at a record $22.4 trillion and climbing. The system cannot sustain itself. Everyone from CBO to the Bipartisan Policy Center to the Federal Reserve has said so.

The government is not going to stop spending. But it is going to start demanding that the money it spends produces better results. CMS is already doing this. The upcoding crackdowns, the flat rate proposals, the star rating pressure. This is the government telling the insurance industry: figure out how to do more with less, or we will take away your bonus payments and compress your margins until you either adapt or die.

The incumbents are dying. UnitedHealth has lost half its market value. Humana is guiding to breakeven on its core product. The old model is collapsing in real time.

Somewhere in the middle of this trillion dollar problem is a company that has built an AI platform that demonstrably reduces hospitalizations, catches chronic diseases earlier, produces the highest quality scores in the country, and creates a 1,500 basis point MCR advantage for the physicians who use it. That company is now licensing this technology to external providers and payers, growing its third party clinician base by over 450% year over year, and approaching its first full year of GAAP profitability.

The chart says AI collapses the cost of care. The data says Counterpart Health is already doing it.

Nobody is going to carry two phones forever. Nobody is going to accept going bankrupt for healthcare forever. The only question is who is already building for what comes next.

Andrew Toy has done this before.

English

@ALSTOCKTRADES Oh maybe the posts about voting? Vivek and Toy?

English

I RAISE MY PRICE TARGET FOR CLOVER HEALTH $CLOV TO $7.25

English

Concerned_American retweetou

Concerned_American retweetou

Melania is 'BREAKING WITH TRUMP BECAUSE SHE KNOWS THE SHIP’S SINKING" — Alex Jones responds to Trump’s post

"This reminds me of Melinda Gates, Melinda French, when SHE started turning against Bill, ALSO OVER EPSTEIN"

English

Concerned_American retweetou

I asked Grok that with these hires sounds like saas partnerships. This is what he said.

Yes, you're spot on — the wave of Provider Success Manager (and related senior roles like Senior Manager, Provider Success or Senior Provider Success Partner) hires by Counterpart Health across multiple markets strongly signals active SaaS partnership and customer success expansion.

What Counterpart Health Actually Is

Counterpart Health is a subsidiary of Clover Health (NASDAQ: CLOV). It spun out/rebranded Clover's internal AI-powered clinical decision support tool (originally Clover Assistant, now Counterpart Assistant or CA) into a standalone SaaS + tech-enabled services platform.

The tool delivers real-time, patient-specific AI insights directly into clinicians' workflows (integrated with major EHRs) to support earlier diagnosis/management of chronic conditions (diabetes, CKD, CHF, COPD, etc.), better documentation/coding, HEDIS quality improvement, and value-based care (VBC) success. It uses a hybrid revenue model: pure SaaS licensing + shared-savings arrangements (and even full capitation options in some deals).8a40eb

It launched externally in mid-2024 to serve not just Clover's own Medicare Advantage plans, but other Medicare Advantage payors, ACOs, provider groups, and VBC enablers nationwide. Early traction includes live users in diverse settings (large systems to small independent practices), published studies showing clinical/financial impact, a Google Cloud partnership for better data access, and specific multi-year deals (e.g., with Southern Illinois Healthcare).644bf3

Why the Provider Success Manager Hiring Wave Matters

These roles are not generic sales or support hires. Job descriptions emphasize:

Building and managing provider partnerships and relationships.

Driving adoption, implementation, training, and expansion of Counterpart Assistant in practices.

Helping providers optimize workflows, achieve measurable success in value-based care (e.g., better outcomes, quality scores, risk adjustment), and maximize ROI from the platform.

Acting as a consultative "product SME" with data analysis and in-office support (often requiring significant travel to practices).

Openings or recent postings include locations like:

Seattle/Tacoma, WA

Nashville/Jackson/Memphis, TN

Jackson, MS

Dallas-Fort Worth, TX

Montgomery/Mobile/Lee counties, AL (Senior Provider Success Partner)

And others in the Gulf region and beyond.

This is a classic customer success / post-sales expansion play in B2B SaaS, especially healthcare tech. Companies hire dedicated success managers when they have (or expect) paying customers who need hands-on help to implement, adopt, and scale usage — which directly ties to retention, upsell, and revenue growth. Hiring regionally shows they're embedding support where provider networks and partnerships are landing or ramping up.8a26d5

Recent leadership hires (e.g., VP of Enterprise Growth & Partnerships from Aledade experience, President of Market Operations for the Gulf Region) further point to scaling external deals with risk-bearing entities and providers.3702a7

SaaS Partnership Momentum

This aligns directly with Counterpart's strategy:

Opening the proven "HEDIS excellence flywheel" (which powered Clover's top-ranked Medicare PPO quality) to third-party payors and providers.

Flexible models for payors (equip their network clinicians), ACOs, practices, and VBC enablers.

Early external wins and hundreds of third-party clinicians already live on the platform as of early 2026 updates.

Healthcare moves slowly (implementation, contracting, EHR integration, regulatory alignment all take time), so the ~2-year gap since the 2024 announcement to visible scaling is normal. The hiring velocity in success roles suggests the pipeline is converting into active deployments and regional expansion — exactly what you'd expect in a growing SaaS business with enterprise healthcare partnerships.

English

Concerned_American retweetou

Hmmm... Provider Success Managers now being hired by @counterparthlth across Texas... started with the Gulf, then PNW two weeks ago, now Texas...

I wonder what they're up to 🤔

$CLOV

English

Concerned_American retweetou

Friendly reminder that I tried to warn everyone about the anti-Trump losers that were trying to hijack MAGA and sabotage us from within.

And I received A LOT of flak for it…

Now POTUS just confirmed that’s exactly what happened.

Fuck everybody who spoke ill on my name.

English

Concerned_American retweetou

Meet Tom, the horse who plays dead whenever someone wants to ride him! 😂

English

Concerned_American retweetou

Failing at everything, Starmer is, as always, trying to deflect responsibility for his failed energy policies. Not a Churchill.

Politics UK@PolitlcsUK

🚨 NEW: Keir Starmer says he is "fed up" with Donald Trump and Putin "I'm fed up with the fact that families across the country see their bills go up and down on energy businesses bills go up and down on energy because of the actions of Putin or Trump across the world"

English

@TokenAtheist1 @ZelenskyyUa No burrow (digging trenches) = No borrow

Get it?

English

I met with representatives of the Hungarian community of Zakarpattia, including military personnel. We spoke and discussed many important issues – above all, preparations for the next winter, business relocation, the role of local self-government in filling the budget, the return of Ukrainians from abroad, and the rehabilitation of warriors and veterans.

Thank you for this meeting. Thank you for your resilience throughout this difficult winter and for supporting the front, and to the military – for all your efforts to defend Ukraine, our skies, and our critical and civilian infrastructure from Russian attacks. I presented the warriors with awards. Thank you for your service.

English

@TokenAtheist1 @ZelenskyyUa Yeah!

Three things to remember, son.

1 - end the war

2 - then security guarantees

3 - in that order

I love simple. ❤️

English

@TokenAtheist1 @ZelenskyyUa Kinda refreshing to hear all you need to know in just one sentence, no?

No fix = No loan

English

@TokenAtheist1 @ZelenskyyUa Mad? For what, telling you the facts? lol

English

Concerned_American retweetou