Sabitlenmiş Tweet

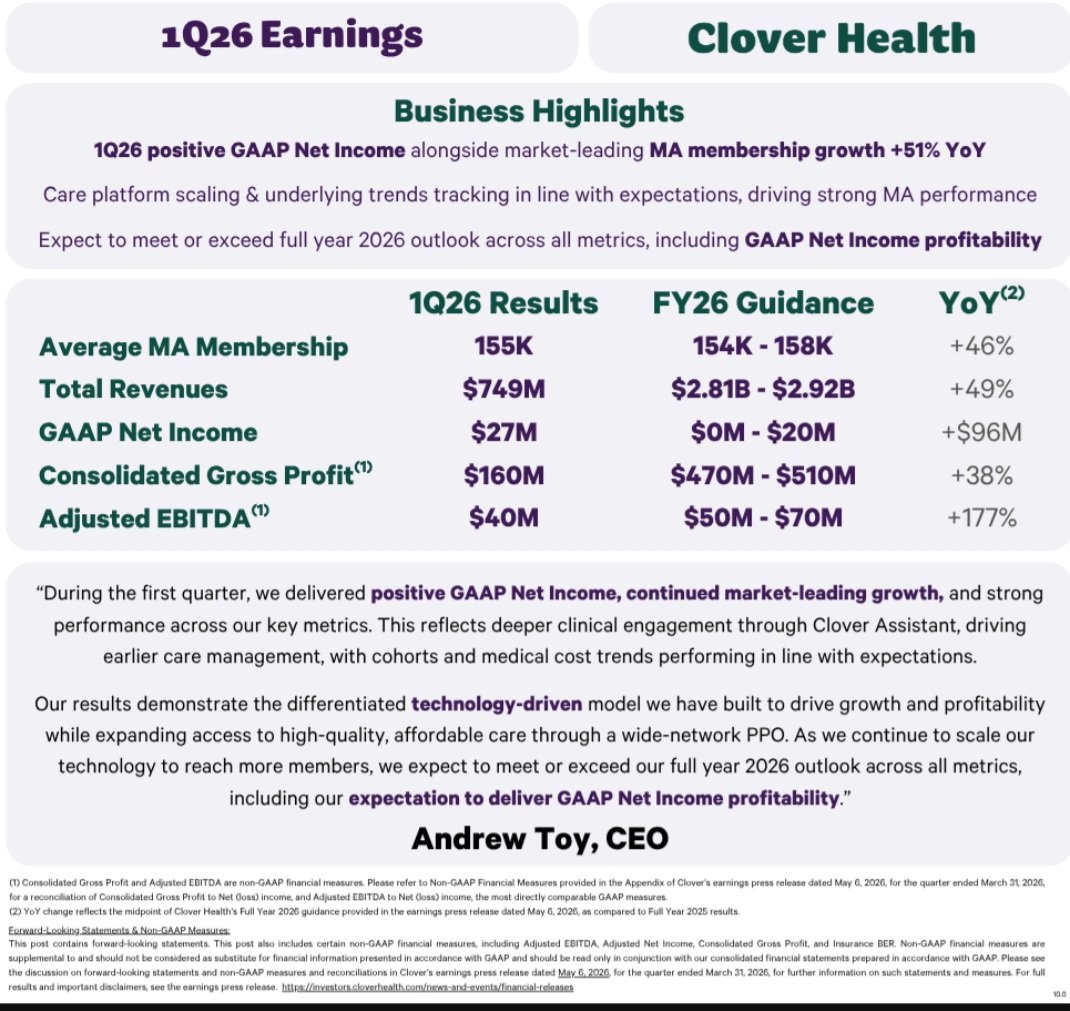

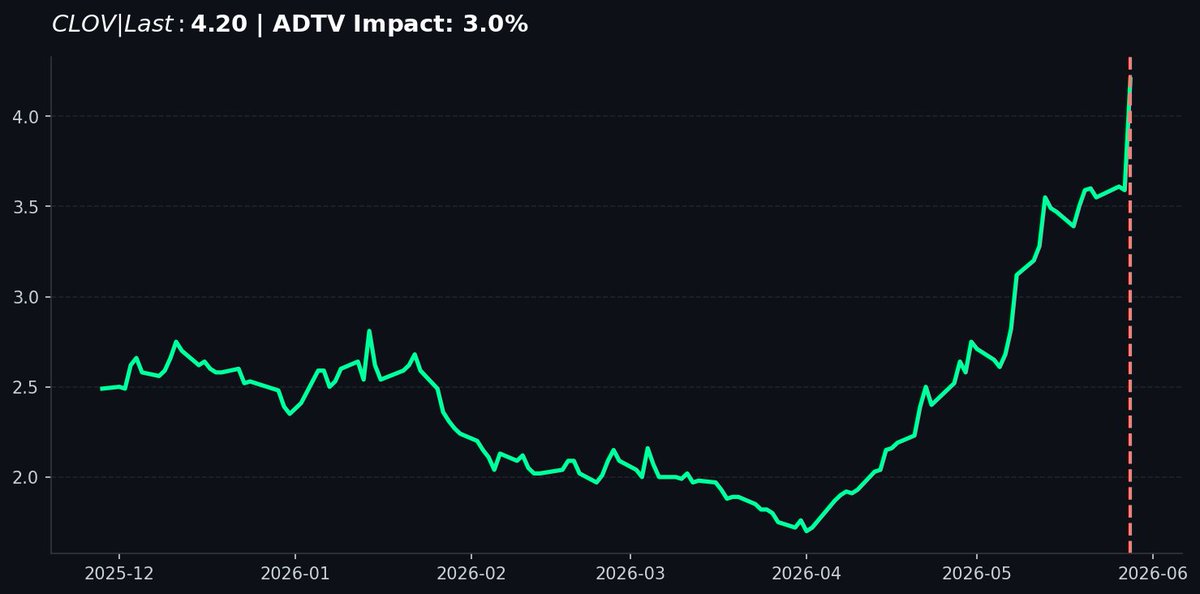

Here's my longterm investment view on $clov... if the company can turn profitable and stave off bankruptcy, I believe it can grow to $50 a share. Buying 10k shares at $3 is a max loss of $30k and a long term target gain of $470k. Risk reward is there for me, personally.

English