Tweet fixado

From the Roman Denarius to the American Dollar: Fractal Anatomy of an Imperial Monetary Cycle

It’s a common misconception that banking and financial crises are a modern phenomenon; the communist tradition, by now internalized within the discourse of liberal, libertarian, and nationalist right-wing circles for over a century, describes credit crises as a phenomenon ultimately caused by “capitalism.” The bank-centric propaganda of the late British Empire, and later the Soviet and American propaganda during the Cold War, place their origin somewhere around the First Industrial Revolution.

In reality, this is false. Credit crises and the banking nature of the economy, where third parties, more or less close to sovereign power, can in fact inflate, mint, un-mint, and lend at interest the ledger-entry currency used to measure value and transfer utility between individuals and across time, are as ancient as the first Mesopotamian temples. Those temples invented formal writing to record credits and debts, began practicing fractional reserve banking, and accumulated and distributed capital, giving rise to speculative crises.

Well then, today I’ll tell you about one of them, which took place 2,000 years ago here in Rome where I live, when, after the centuries of the republican era based on sound money that had spread as a reserve currency from India to North Africa to Britain, the first dynasty at the head of the young Roman Empire, the Julio-Claudian one, fell into a spiral of corruption and collusion of interests in the hands of financial power. The “financial crisis of 33 AD” was an episode of patrimonial and real estate concentration in the hands of the senatorial elite and the state treasury, marking the beginning of the economic polarization of the Empire. The parallels with today’s globalized world under American hegemony are endless.

[Sources: Tacitus, "Annals"; Suetonius, "The Lives of the Caesars"; Cassius Dio, "Roman History"; Thornton, M.K., "The Financial Crisis of A.D. 33: A Keynesian Depression?"; Taylor, B., "Tiberius Used Quantitative Easing to Solve the Financial Crisis of 33 AD"; Bartlett, C., Harvard University; "The Financial Crisis, Then and Now: Ancient Rome and 2008 CE".]

The Origin of the Crisis:

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered." - T. Jefferson, 1809.

Julius Caesar had passed a law in 49 BCE which regulated usury, requiring lenders to possess a certain quantity of farmland in Italy. The law had been passed as a wartime measure to prevent capital flight from Italy, which was running increasing trade deficits, but it had been largely ignored.During the early reign of Augustus, the Roman government, in order to consolidate imperial power and increase influence over the senate and aristocratic class, significantly expanded the money supply through cash handouts, extensive public works projects, and the acquisition of Italian agricultural land for veterans to settle (these being partly funded by Egypt’s treasury). As a result, interest rates fell significantly, from around 12 to 4 percent per annum.This exacerbated the trade deficit of the Italian peninsula; ever more abundant gold and silver coins flowed out from the Roman Empire to pay for imports of luxury goods, especially from India. Meanwhile, large owners of farmland began accumulating credit from banking institutions to buy increasing amounts of land in Egypt, Gaul, Greece, and across Italy, using their existing capital and creditworthiness to benefit from the inflating supply of credit provided by large banking institutions such as the argentarii, who reduced their metal reserves relative to the payment promises issued—betting on continuous monetary expansion and on the assumption that creditors would not all demand redemption of their gold and silver at the same time: fractional reserve banking.

The Leveraged Collapse of the Roman Banking System:

“The death of Lincoln was a disaster for Christendom. There was no man in the United States great enough to wear his boots and the bankers went anew to grab the riches. I fear that foreign bankers with their craftiness and tortuous tricks will entirely control the exuberant riches of America and use it to systematically corrupt civilization.” Otto von Bismark, German Chancellor, 1865.

As with many financial panics, this one began when unexpected events in one part of the Roman world spread to the rest of the Empire. The important firm of Seuthes and Son, of Alexandria, was facing difficulties due to the loss of three richly laden ships in a Red Sea storm, followed by a fall in the value of ostrich feathers and ivory. Around the same time, the great house of Malchus and Co. of Tyre, with branches in Antioch and Ephesus, suddenly went bankrupt as a result of a strike among their Phoenician workmen and the embezzlement committed by a freedman manager.

These failures affected a major Roman banking house, Quintus Maximus and Lucius Vibo. A run commenced on their bank and spread to other banking houses said to be involved, particularly Brothers Pittius. The banks did not have the promised money nor sufficient land to back their issued payment promises. The Via Sacra was the Wall Street of Rome, and this thoroughfare teemed with excited merchants. These two firms sought aid from other bankers, as is done today. Unfortunately, rebellion had erupted among the peoples of Northern Gaul, where a great deal of Roman capital had been invested, and a moratorium had been declared by the local governments due to the disturbed conditions.

Other bankers, fearing contagion and further suspensions, refused to assist the first two houses, which further worsened the crisis. When Publius Spencer, a wealthy nobleman, requested 30 million sesterces from his banker Balbus Ollius, the firm was unable to fulfill the withdrawal and was forced to close its doors. Over the following days, prominent banks in Corinth, Carthage, Lyons, and Byzantium announced they had to “rearrange their accounts,” i.e., they had failed.

This sparked a full-scale banking panic and the closure of several institutions along the Via Sacra in Rome. The confluence of these seemingly unrelated events triggered a cascading financial collapse. To protect themselves, banks began calling in loans. When debtors could not meet their creditors’ demands, they were forced to liquidate homes and possessions, leading to a dramatic fall in real estate and asset prices as buyers vanished.

A full-scale panic ensued, not only in Rome but throughout the Empire. Over the course of a few weeks, one collapse precipitated another, and the financial crisis spread across Egypt, Greece, Gaul, and every corner of the Empire.

The 33 CE Financial Crisis:

“Independently of its misdeeds, the merepower, the bare existence of such a power is a thing irreconcilable with the nature and spirit of our institutions.” - Nicolas Trist, secretary to President Andrew Jackson, about the Second Bank of the US, 1832

“I am afraid the ordinary citizen will not like to be told that the banks can and do create money. And they who control the credit of the nation direct the policy of Governments and hold in the hollow of their hand the destiny of the people.” Reginald McKenna, as Chairman of the Midland Bank, 1924

As a consequence, in 33 CE, under the rule of Tiberius, a flood of cases was brought against prominent individuals accused of widespread violation of the land-owning requirement established by Julius Caesar’s law a century earlier. Tacitus tells us that every one of the 600 senators was personally in violation of this law, and they sought Tiberius’s indulgence. He instituted a grace period of eighteen months during which all personal finances were to be brought into compliance with the law. What followed was a severe credit crisis.

The Senate passed a resolution requiring creditors to invest two-thirds of their capital in Italian land and debtors to repay the same proportion of their loans. In practice, however, creditors demanded full repayment, and debtors were morally compelled to pay in full.This triggered the worst phase of the crisis. Debtors tried to sell their lands to raise funds for repayment, but the flood of properties onto the market depressed prices. Those unable to raise sufficient funds, or unable to sell at all, turned to money lenders who charged exorbitant interest rates. This recourse failed in many cases, leading to widespread defaults and numerous debtors being brought to court. When judgments went against them, many were dispossessed of their lands.

The senatorial decree, intended to prop up land values, only worsened the situation. Because it forced many to sell their properties, prices plummeted. Creditors who were required to invest in land instead held onto the cash from the loans they had managed to call in, waiting for prices to fall further before buying, thus deepening the collapse in land values and the shortage of credit that drove interest rates skyward.

At this point, Tiberius intervened to cover the losses of the banking system and the aristocratic families, who were also the main financiers of the State, by implementing what can be described as Quantitative Easing. He distributed 100 million sesterces, equivalent to billions in modern dollars, to specially chartered banks, essentially a proto–public central bank, to provide three year interest free loans. Each loan was secured by land worth twice its value. Tacitus reports that this restored credit and encouraged the gradual return of private lenders.

Though a few banks never recovered from the panic, most resumed normal business, and the financial turmoil ended as quickly as it began. This was the “whatever it takes” of Bernanke and Draghi two millennia earlier: injecting liquidity into a bankrupt banking system to cover losses and save a central state dependent upon it.

The Consequences of the Crisis:

“I am a most unhappy man. I have unwittingly ruined my country. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated Governments in the civilized world; no longer a Government by free opinion, no longer a Government by conviction and the vote of the majority, but a Government by the opinion and duress of a small group of dominant men.” - Woodrow Wilson, some years after signing the Federal Reserve act in 1913.

"The real truth of the matter is, as you and I know, that a financial element in the large centers has owned the government ever since the days of Andrew Jackson" -F. D. Roosevelt (in a letter to Colonel House, dated 1933)

The major liquid creditors, namely a handful of senators, patrician families, and above all the aristocracy close to the imperial treasury, acquired vast tracts of land at fire sale prices. Small and medium landowners, as well as urban entrepreneurs, who lacked access to the credit of the central bank, were wiped out.

Huge feuds were created or expanded, often managed by slaves or imperial freedmen, and directly tied to the senatorial aristocracy or the fiscus. In essence, those with access to imperial credit accumulated capital; those dependent on private credit lost their property. The number of large landowners decreased, but their relative wealth increased. Real estate and financial capital increasingly fell into the hands of those connected to the State and the imperial court.

In the medium term, this crisis consolidated the economic foundation of imperial power, as the fiscus and senatorial families merged into an integrated patrimonial system. The emperors succeeding Tiberius continued to use this mechanism, doubling down on the credit system initiated by Augustus, to appease the populace even as it lost everything to the aristocratic class, financing wars and public works: what the satirical poet Juvenal, seventy years after the 33 CE crisis, would call panem et circenses, bread and circuses, to distract the masses.

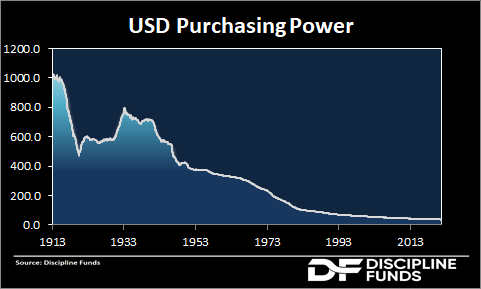

Taxes kept rising century after century, while the silver content of Roman coinage began to collapse amid successive speculative crises fueled by monetary expansion and government corruption. The repeated inflationary episodes eroded confidence in the imperial currency, which by then was regularly issued by the fiscus Caesaris acting as a de facto central bank for the credit system. The antoninianus of Caracalla lost over 95% of its silver content in less than a century, during the crisis of 235–284 CE.

Public debt kept growing, while war financing, one of the main sources of government revenue, became increasingly complex due to the extravagance of the Roman aristocracy, demographic decline, and the corruption of aristocratic generals. More and more troops were recruited from among barbarian populations in exchange for conquered lands.

In the later imperial age, the emperor’s refusal to debase the currency to redistribute wealth to the aristocracy often resulted in his assassination by the Praetorian Guard.

Conclusions:

"The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve." - Satoshi Nakamoto, 2009.

As the saying goes, history doesn’t repeat itself, but it rhymes, essentially because memory fades, people remain the same, and identical incentives produce identical results. Just as the branches of a tree, unaware of what the trunk or larger boughs have done, replicate their shapes in fractal structures because they respond to the same underlying rules.

During the Roman Imperial Age, the process known as Gresham’s Law is perfectly visible. The silver denarius of Augustus contained about 3.9 grams of fine silver; by the time of Caracalla (early 3rd century CE), the new antoninianus contained less than 2 grams, yet it was legally valued at “two denarii.” Under Gallienus (about 260 CE), it contained less than 0.05 grams, virtually copper plated bronze. The “good” money (old denarii) quickly vanished from circulation; it was hoarded or melted down to recover the silver. The “bad” money (antoniniani) remained in use but collapsed in real value. Large-scale trade shifted toward barter or payments in kind or gold (aurei), i.e., toward reserve assets external to the degraded system.

This process almost always follows the same sequence, ancient or modern (Weimar, Zimbabwe, Argentina, etc.):

-Parallel issuance of coins or notes with differing real content.

-Preferential use of the weaker money for payments, and hoarding/export of the stronger one.

-Disappearance of the strong money from circulation, reducing the effective stock of solid reserves.

-Inflationary acceleration as the weak currency becomes virtually limitless in issuance.

-Transition to a new currency or standard (gold, barter, foreign currency, Bitcoin, etc.).

We are witnessing the same pattern today across the globalized world under the US financial empire. The political left may complain that housing prices are too high, but fails to realize that even a 10% drop in home values would produce the same systemic effects as 2008. The government would be forced to bail out the banking system to save itself, effectively taxing existing currency holders (the poor) by issuing more money. The best outcome it can offer: panem et circenses, a few populist bonuses paid with newly printed currency, and nothing more.

Meanwhile, the political right may lament high taxes, immigration, or the degree of “free market” in the economy, while wealth concentration explodes, laws are written under lobbying pressure, and corrupt officials enrich their families through insider trading, while major banks hold a gun to the State’s head. There is nothing “free” in a State sold to the institutions that create its credit, something well understood by the Founding Fathers of the young American Republic, who drew their warnings from centuries of European history.

After the fall of the Roman Empire, Europe merely repeated these same dynamics over and over again, as power passed into the hands of the next issuing empire with the strongest currency: the gold florin, the Portuguese real, the Spanish real, the Dutch guilder, the French livre, and the English pound. Each time, inequality and central corruption rose, purchasing power fell, Gresham’s Law took hold, capital and purchasing power fled toward stronger currencies, and inefficiencies caused by corruption and distorted price signals triggered a spiral that destroyed the currency and the underlying economy, until a new, stronger one emerged elsewhere, creating positive feedback loops for the rising empire.

The only reason the US dollar hasn’t yet fully collapsed is that since the Bretton Woods agreements, it has faced no real competition. Today, 93% of global liquid credit is managed by the Fed, the ECB, and the Bank of England, whose systems are now fully welded together through a private interbank network recycling the equivalent of the entire global GDP every week, over 7 trillion dollars in daily transactions.

Every other monetary domain, from the Yuan to the Peso, is even worse.

A resurgence of hard money by Gresham's Law is only a matter of time. Capital will increasingly flow toward scarce assets, especially easily transferable assets, and those who own the most will dominate the next cycle of history.

English