Jonathan Barbero retweetou

Jonathan Barbero

594 posts

@mmpoli @fedesturze @BancoNacion Contáctate con el BNA por teléfono para que revisen el caso, la migración es simple

bna.com.ar/Home/Contacten…

Español

@fedesturze @BancoNacion Lamentablemente el @BancoNacion está cambiando la app y el Home banking ahora sí o si se necesita celular. Y además la app nueva da error al registrarse.

Español

Jonathan Barbero retweetou

FINALMENTE PODREMOS AHORRAR EN EL SECTOR FINANCIERO. Los argentinos nunca tuvimos manera de ahorrar en un banco con una renta mensual al tiempo que protegíamos nuestro capital. Bueno, eso se acabó hoy. Acabo de hacer un plazo fijo en el @BancoNacion que resuelve ambos problemas. Primero y principal porque está en UVA, así que mi dinero queda protegido en poder adquisitivo. Segundo, porque tiene un interés interesante del 4,5% anual. Tercero, y esto es lo clave: me paga el interés todos los meses. Es decir que me da una renta mensual que se ajusta por inflación y cuando termina recupero mi plata intacta en valor real. Cuarto, porque me permite invertir por plazos más largos que lo que es normal en el sistema. El que constituí hoy fue por 900 días.

Históricamente los plazos fijos en el sector financiero en Argentina rindieron en promedio -5% anual. Es decir que no eran una alternativa de ahorro. Por ello muchos argentinos ahorran comprando dólares, pero eso rinde cero y además hay inflación en EEUU, así que es como poner la plata en una lata y quemar un poco todos los años. Además, si el dólar cae en valor real encima pierde poder adquisitivo acá. Los que pueden ahorran con propiedades que alquilan. La plata está medianamente protegida en valor, a prueba de expropiaciones, y da un retorno de entre 3 y 5% anual (habrá los que dan más y los que dan menos, por supuesto). Pero recordemos que un departamento tiene un montón de costos, la propiedad se deteriora, paga impuestos y la renta también paga impuestos.

Este plazo fijo que ofrece el @BancoNacion es como tener un pedacito de un departamento: me ofrece una renta actualizada por inflación, excepto que sin costos de gestión ni de mantenimiento, sin riesgos para el capital, y exento de impuestos. Y democratiza la opción, porque cualquiera pueda hacerlo, no sólo aquellos que tienen los suficiente para un depto completo.

Hagamos una comparación. Un buen departamento de 250.000 dólares, si rinde el 5%, es un alquiler de 1,45 millones mensuales. Pero a esto hay que restarle impuestos, ABL, gastos de mantenimiento y gestión. Y esto, sin tener en cuenta que el alquiler típicamente no se actualiza todos los meses. 250.000 dólares invertido en este plazo fijo me da una renta de 1,3 millones mensuales. Lo puedo hacer por el monto y plazo que quiera. El capital está asegurado. La renta se me indexa todos los meses. No tengo impuestos para mantener la propiedad ni impuestos a pagar sobre la renta. Bingo!

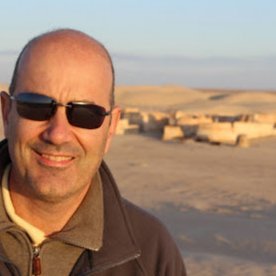

Mi impresión es que es la primera vez que tenemos un producto de ahorro en el sector financiero argentino. Para hacerlo buscar la opción Plazo Fijo UVA Pago Subperiodos (ver imagen).

Importantísimo para el sistema. El banco capta al 4,5% y presta ese dinero en un prendario o un hipotecario al 8, 10 or 15%. Como ahorrista feliz, pero al mismo tiempo le doy la oportunidad a otra persona a acceder a un crédito. Win-win como son las transacciones económicas en libertad que nos pide estimular el presidente @JMilei. Y solo si el sistema financiero ofrece alternativas atractivas de ahorro podrá crecer.

Felicitaciones a Darío Wasserman de @BancoNacion por esta innovación que espero sea un primer paso para el banco y para muchos argentinos. VLLC!

Español

Jonathan Barbero retweetou

Pocos entienden el "game changer" de este plazo fijo uva +4.5% con pagos mensuales.

Imaginate que tenes 80k usd y decis bueno, compro un dpto y lo pongo en alquiler, inmovilizas tu capital, es muy jodido de recuperar liquidez y ganas prácticamente lo mismo que con este Plazo Fijo que tenes liquidez al vencimiento inmediata.

Poca gente lo va a entender, poca gente lo va a considerar valioso.

Ahora bien van a venir los sommeliers de inversiones medidas en USD, está bien, el inmueble se actualizaría en USD y como tenemos este país pendular, mientras exista riesgo kuka, el dólar le puede ganar a cualquier tasa.

Pero en términos reales vas a ser ganador, que es algo muy importante!

Español

Jonathan Barbero retweetou

Hi @bcherny! Claude Code is amazing, but permission prompts are a bit too narrow ("Yes" / "Yes, and don’t ask again for: ls:*" / "No"). Would love a 4th option to manually define the scope (e.g., "allow * in this path") so I don't get prompted again for a cat on those files.

English

Jonathan Barbero retweetou

📍"EXPOAGRO 2026": RÉCORD DEL BANCO NACIÓN EN SOLICITUDES DE CRÉDITO

En el primer día de trabajo en “Expoagro 2026”, la entidad registró 8.000 solicitudes de crédito, cuadruplicando el volumen alcanzado en la jornada inaugural de la edición anterior, en la que se habían contabilizado alrededor de 2.000.

Este fuerte incremento refleja el alto interés del sector productivo por las líneas crediticias y las tasas más competitivas del mercado en pesos y dólares que presentó el Banco Nación.

Español

Jonathan Barbero retweetou

📍EXPOAGRO 2026: BANCO NACIÓN LIDERA EL FINANCIAMIENTO PARA MAQUINARIA AGROINDUSTRIAL CON TASAS DE 0% EN DÓLARES Y DEL 19% EN PESOS

En la 20° edición aniversario de @Expoagrocom 2026, la entidad presentó una propuesta crediticia integral para impulsar la inversión en el campo, con las tasas más competitivas del mercado y condiciones especialmente diseñadas para productores y empresas.

Entre las principales líneas se destacan, para maquinaria agroindustrial nueva:

✅ 0% de tasa en dólares.

✅ Y 19% de tasa en pesos.

La oferta incluye además financiamiento para maquinaria usada, camiones, utilitarios, insumos estratégicos y capital de trabajo, junto con herramientas digitales a través de BNA+ Empresas, AgroNación y PymeNación.

El lanzamiento de la propuesta se realizó en el stand institucional de la entidad, encabezado por el presidente del Banco, Darío Wasserman, junto al Directorio y el gerente general, Gastón Álvarez.

Más información: prensa.bna.com.ar/Expoagro2026

Español

Jonathan Barbero retweetou

An important, and perenially underrated, aspect of "trustlessness", "passing the walkaway test" and "self-sovereignty" is protocol simplicity.

Even if a protocol is super decentralized with hundreds of thousands of nodes, and it has 49% byzantine fault tolerance, and nodes fully verify everything with quantum-safe peerdas and starks, if the protocol is an unwieldy mess of hundreds of thousands of lines of code and five forms of PhD-level cryptography, ultimately that protocol fails all three tests:

* It's not trustless because you have to trust a small class of high priests who tell you what properties the protocol has

* It doesn't pass the walkaway test because if existing client teams go away, it's extremely hard for new teams to get up to the same level of quality

* It's not self-sovereign because if even the most technical people can't inspect and understand the thing, it's not fully yours

It's also less secure, because each part of the protocol, especially if it can interact with other parts in complicated ways, carries a risk of the protocol breaking.

One of my fears with Ethereum protocol development is that we can be too eager to add new features to meet highly specific needs, even if those features bloat the protocol or add entire new types of interacting components or complicated cryptography as critical dependencies. This can be nice for short-term functionality gains, but it is highly destructive to preserving long-term self-sovereignty, and creating a hundred-year decentralized hyperstructure that transcends the rise and fall of empires and ideologies.

The core problem is that if protocol changes are judged from the perspective of "how big are they as changes to the existing protocol", then the desire to preserve backwards compatibility means that additions happen much more often than subtractions, and the protocol inevitably bloats over time. To counteract this, the Ethereum development process needs an explicit "simplification" / "garbage collection" function.

"Simplification" has three metrics:

* Minimizing total lines of code in the protocol. An ideal protocol fits onto a single page - or at least a few pages

* Avoiding unnecessary dependencies on fundamentally complex technical components. For example, a protocol whose security solely depends on hashes (even better: on exactly one hash function) is better than one that depends on hashes and lattices. Throwing in isogenies is worst of all, because (sorry to the truly brilliant hardworking nerds who figured that stuff out) nobody understands isogenies.

* Adding more _invariants_: core properties that the protocol can rely on, for example EIP-6780 (selfdestruct removal) added the property that at most N storage slots can be changedakem per slot, significantly simplifying client development, and EIP-7825 (per-tx gas cap) added a maximum on the cost of processing one transaction, which greatly helps ZK-EVMs and parallel execution.

Garbage collection can be piecemeal, or it can be large-scale. The piecemeal approach tries to take existing features, and streamline them so that they are simpler and make more sense. One example is the gas cost reforms in Glamsterdam, which make many gas costs that were previously arbitrary, instead depend on a small number of parameters that are clearly tied to resource consumption.

One large-scale garbage collection was replacing PoW with PoS. Another is likely to happen as part of Lean consensus, opening the room to fix a large number of mistakes at the same time ( youtube.com/watch?v=10Ym34… ).

Another approach is "Rosetta-style backwards compatibility", where features that are complex but little-used remain usable but are "demoted" from being part of the mandatory protocol and instead become smart contract code, so new client developers do not need to bother with them. Examples:

* After we upgrade to full native account abstraction, all old tx types can be retired, and EOAs can be converted into smart contract wallets whose code can process all of those transaction types

* We can replace existing precompiles (except those that are _really_ needed) with EVM or later RISC-V code

* We can eventually change the VM from EVM to RISC-V (or other simpler VM); EVM could be turned into a smart contract in the new VM.

Finally, we want to move away from client developers feeling the need to handle all older versions of the Ethereum protocol. That can be left to older client versions running in docker containers.

In the long term, I hope that the rate of change to Ethereum can be slower. I think for various reasons that ultimately that _must_ happen. These first fifteen years should in part be viewed as an adolescence stage where we explored a lot of ideas and saw what works and what is useful and what is not. We should strive to avoid the parts that are not useful being a permanent drag on the Ethereum protocol.

Basically, we want to improve Ethereum in a way that looks like this:

YouTube

English

Español

just finished reading "The scaling era: An oral History of AI" by @dwarkesh_sp from @stripepress

tl;dr: it was meh. the podcast >> the book

the book is a compilation/mashup of Dwarkesh's interviews with AI industry experts. but the format is not working for it IMO

specifically, in the first few chapters about Scaling, Evals and Internals it was not easy for me to understand how one segment of an expert conversation follows the next. seemed very unrelated, discrete hops

the excerpts are a lot more cohesive towards the end (Impact, Explosion, Timelines) but that part also has the most speculation

one great thing was using AI (@ChatGPTapp or @GeminiApp) to explain things in detail. the book does have side notes, but you do want to use AI to understand it more (I don't think I understood it fully)

wouldn't recommend it

English

Jonathan Barbero retweetou

Happy to announce that @yerbamateina zero sugar cold brew Yerba Mate (canned in BPA free cans) is now in @WholeFoods nationwide.

English

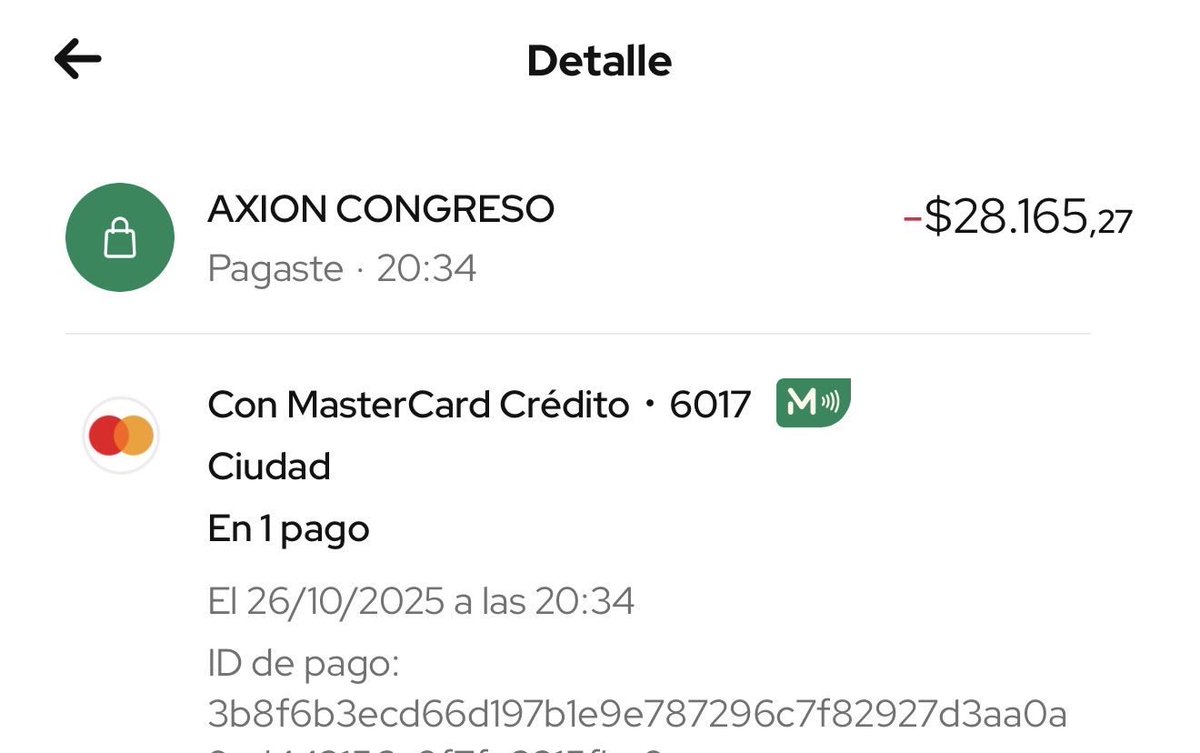

⛽️ Axion + cupón ON + buepp crédito

✔️12% descuento cupón de la app ON

✔️10% extra buepp + MODO + crédito

Posibilidad de ahorrar un domingo con buepp crédito ( la obtenes gratis desde la app buepp )

Español

Al fin @elonmusk pudo domar a los bots? ni uno me apareció hoy

Español

Jonathan Barbero retweetou

Introducing the Uniswap Cup ⚽️

A single-day fútbol tournament in Buenos Aires, featuring 32 of your favorite teams in crypto

Kicking off November 16th (just in time for @EFDevcon)

And the best part is you’re invited to come play 👀

English

Jonathan Barbero retweetou

Dato random copado:

¿Cuándo el costo de transporte del humano prehistórico se volvía inviable? 🏃♂️

Desde los 300km, la mitad de la carga se absorbía por el costo de alimentarse. 🌮.

A los 600km, el costo de alimentarse era equivalente a la carga. 📦

Español

0 en Galicia. 0 en Macro. 0 en Santander. 0 en BBVA. 0 en Patagonia. 0 en ICBC. 40% en @uala_arg. ❤️

Español

Jonathan Barbero retweetou

Jonathan Barbero retweetou

Jonathan Barbero retweetou

Jonathan Barbero retweetou

AGI is definitely achievable in the near term if we redefine it appropriately.

English