Aaryan

1.3K posts

Aaryan

@BscDetector

💭 Turning ideas into reality | 🚀 Exploring the intersection of tech, creativity, and life | ✨ Curiosity is my superpower Elite Goat @ Iotex

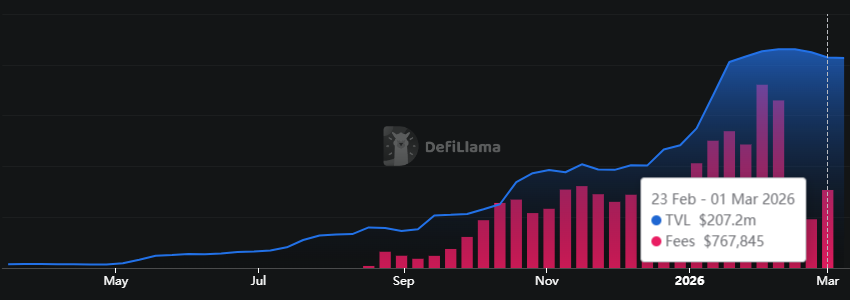

A lot of people ask which Perp DEXs I’m interacting with and where I actually rank. Here’s a transparent breakdown, categorized by effort level 👇 🔥 Top Effort Play (Serious Focus) 1. @variational_io , I Ranked #1 with 46K+ points. This is where most of my energy goes. ⚡ Medium Effort Plays (Exploring the Tech & Positioning Early) 2. @Backpack - 211K+ points in Season 4. Shoutout to @MadVincent666 3. @tread_fi - Ranked #19 with 9K+ points. 4. @pacifica_fi - 209K+ points. 5. @extendedapp - Ranked #85 with 63K+ points. 🧪 Early Positioning / Registered @01Exchange @nadoHQ @paradex Still monitoring these closely. 🎯 My Strategy Is Simple: I primarily trade $BTC, while rotating into key alts like $ETH, $SOL, $HYPE, and $LIT when the opportunity makes sense. Focused execution. Controlled aggression. Volume with intent. Which Perp DEX are you grinding right now and why? 👇

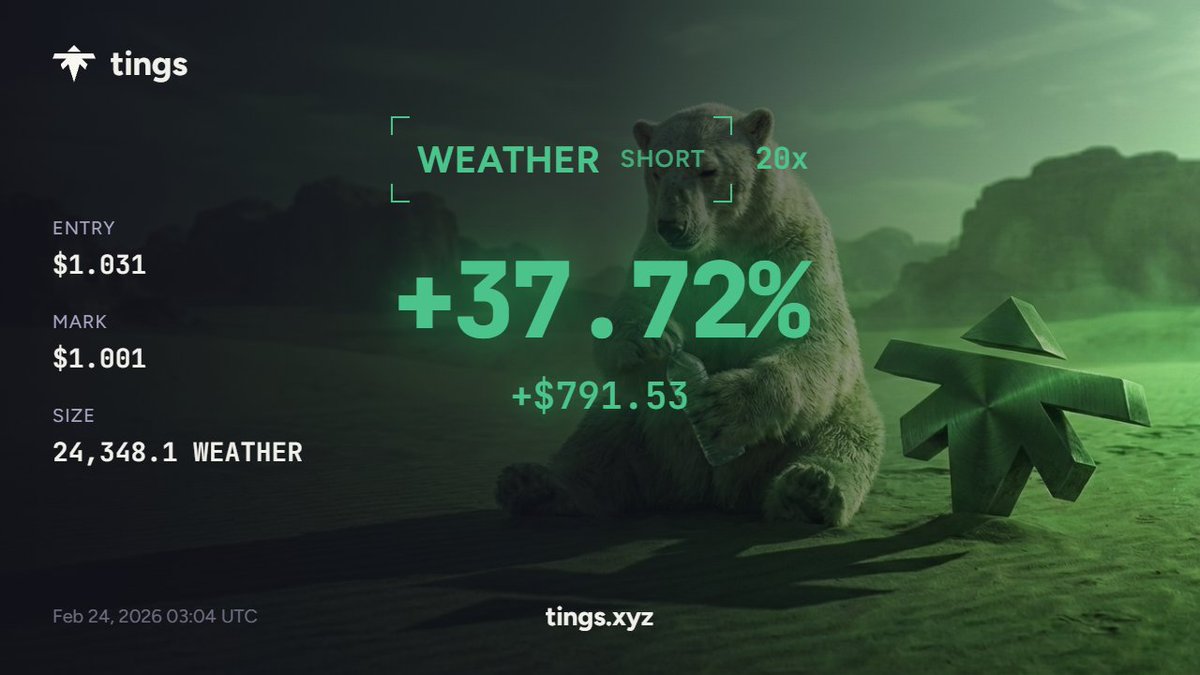

You asked for more than pair trading, so we built it Create and trade fully customizable baskets with up to 20 assets, powered by @HyperliquidX Now live at: trade.hyperswap.exchange