Cipher Cap ретвитнул

Goldman's David Solomon providing some much needed rational thought around private credit:

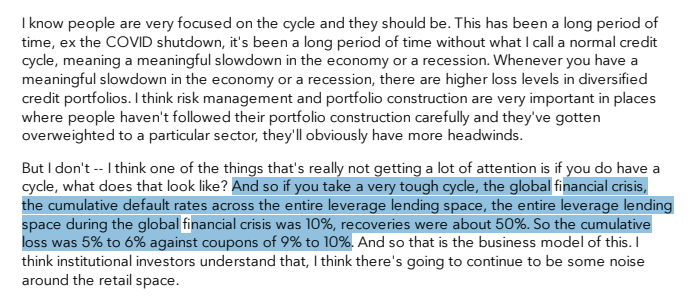

- GFC saw defaults peak at 10%

- recoveries were 50%

- trough cumulative loss of 5%-6% vs coupons of 9%-10%

For context, listed BDCs are currently pricing in defaults of more than 20%

English