Mike@MikeLongTerm

$GRAB-Fin is going to be 30%+ of overall Revenue

Long-Term. Initially I only had it projected to be 10-15%

Southeast Asia has ~700+ million people, with estimates showing 60–85% of adults either unbanked (no account) or underbanked (limited services beyond basic accounts). This translates to roughly 300 million+ people who are smartphone-savvy, often run small businesses or drive for platforms like Grab, but are shut out of traditional credit, insurance, savings, or efficient payments due to no credit history, paperwork barriers, or lack of physical bank branches.

I will write a thread on Cash Loan potential later.

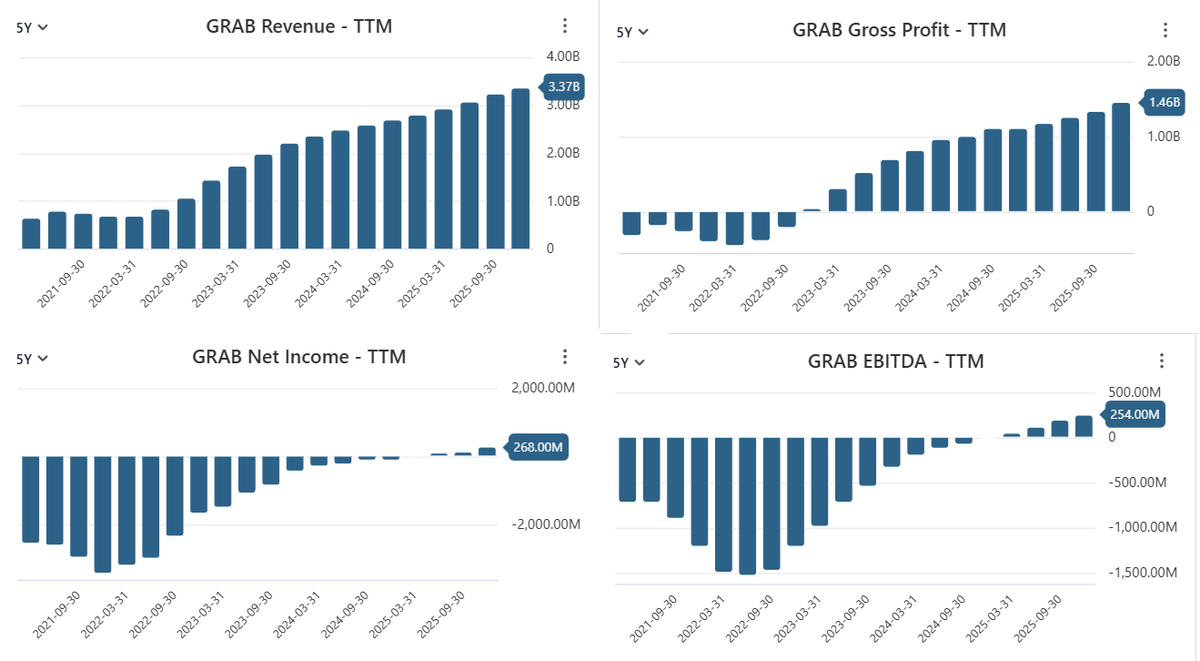

Management guided for above $2B Loan book by end of 2026 and H2 2026 to be profitable.

I believe, guidance is conservative, and loan book may hit $2.5-$3B by year end, and yes it is pretty aggressive, as margin is much higher from various financial services. AKA nonstop Margin expansion !

Currently Revenue as % of Loan book is ~8-9%. As $GRAB-Fin scales, it will improve to 12-15% over time. This is per quarter speaking.

So we are looking at $2.5B Loan book to generate ~$300m by Q1 2027, or $1.4-$1.7B revenue FY2027(just GrabFin)

Longer term 5-10 years out, we could be talking about $40-$50B Loan book, mostly will be financed by merchants/drivers/users deposits, banks owned by $GRAB, and partnerships. It will rely less on Internal Cash. GrabFin will become more efficient long term, or getting to that 12-15% of Total Loan Book per quarter.

Or in this case, $4.8B-$7.5B per quarter revenue.

The 70%+ unbanked/underbanked stat is the core growth thesis(similar to Wechat) for Grab’s next decade and the subscription, Ads side are similar to $AMZN. By turning its super-app into the daily financial hub for the underserved (drivers getting working-capital loans, merchants getting instant credit, everyday users getting micro-savings/insurance), GrabFin converts daily transactions into sticky, profitable financial relationships. It’s not just racing, it’s using its existing SuperApp Ecosystem as a rocket ship to dominate the region’s biggest remaining digital economy gap. Recent results (record loans, deposits, and revenue acceleration) show the strategy is already delivering.

Not Financial Advice!